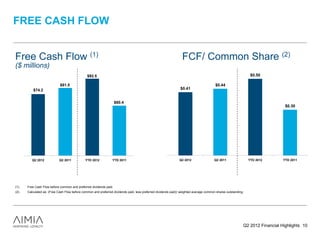

Download to read offline

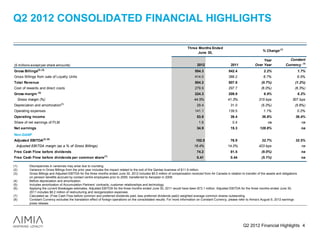

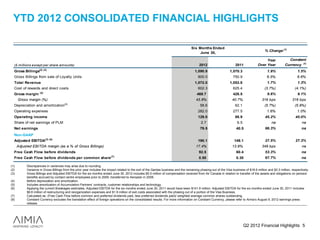

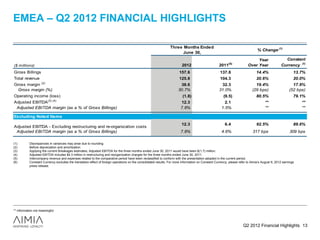

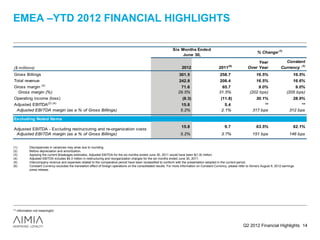

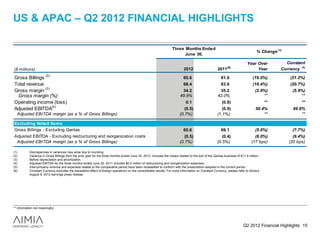

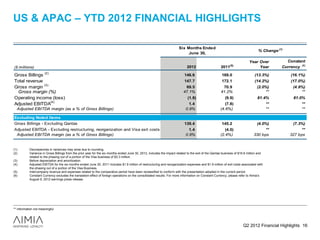

This document provides financial highlights for Q2 2012, including year-over-year comparisons. Some key figures increased significantly from 2011 to 2012, such as operating income (up 36.8%), net earnings (up 128.8%), and adjusted EBITDA (up 32.7%). However, total revenue decreased slightly (down 0.7%) from 2011 to 2012. The document also notes that results are subject to various risks and uncertainties and may differ materially from forward-looking statements.

![1 Q09 Earnings Eng Final[20090421134102809]](https://cdn.slidesharecdn.com/ss_thumbnails/1q09earningsengfinal20090421134102809-090629072608-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)