Downloaded 17 times

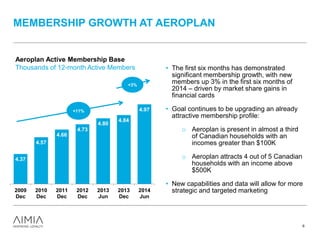

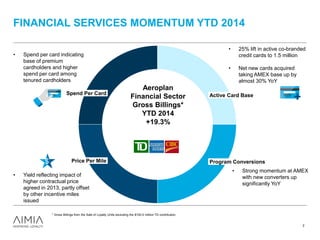

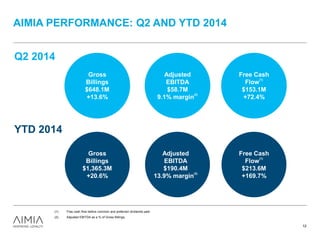

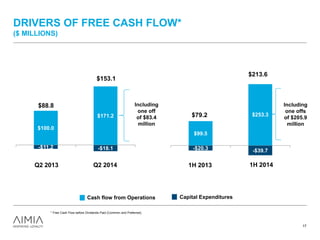

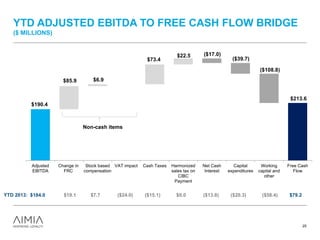

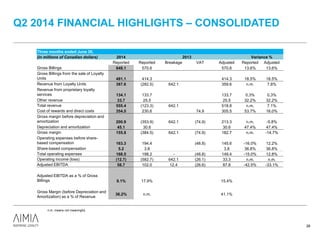

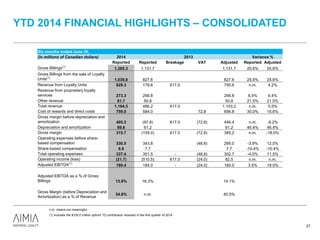

- Aimia reported strong financial results for Q2 2014, with gross billings up 13.6% and free cash flow up 72.4% - Aeroplan membership grew 4% to 5 million members since announcing its transformation, with co-branded credit cardholders reaching 1.5 million - A new long-term partnership with Fractal Analytics was announced to build on Aimia's existing analytics capabilities