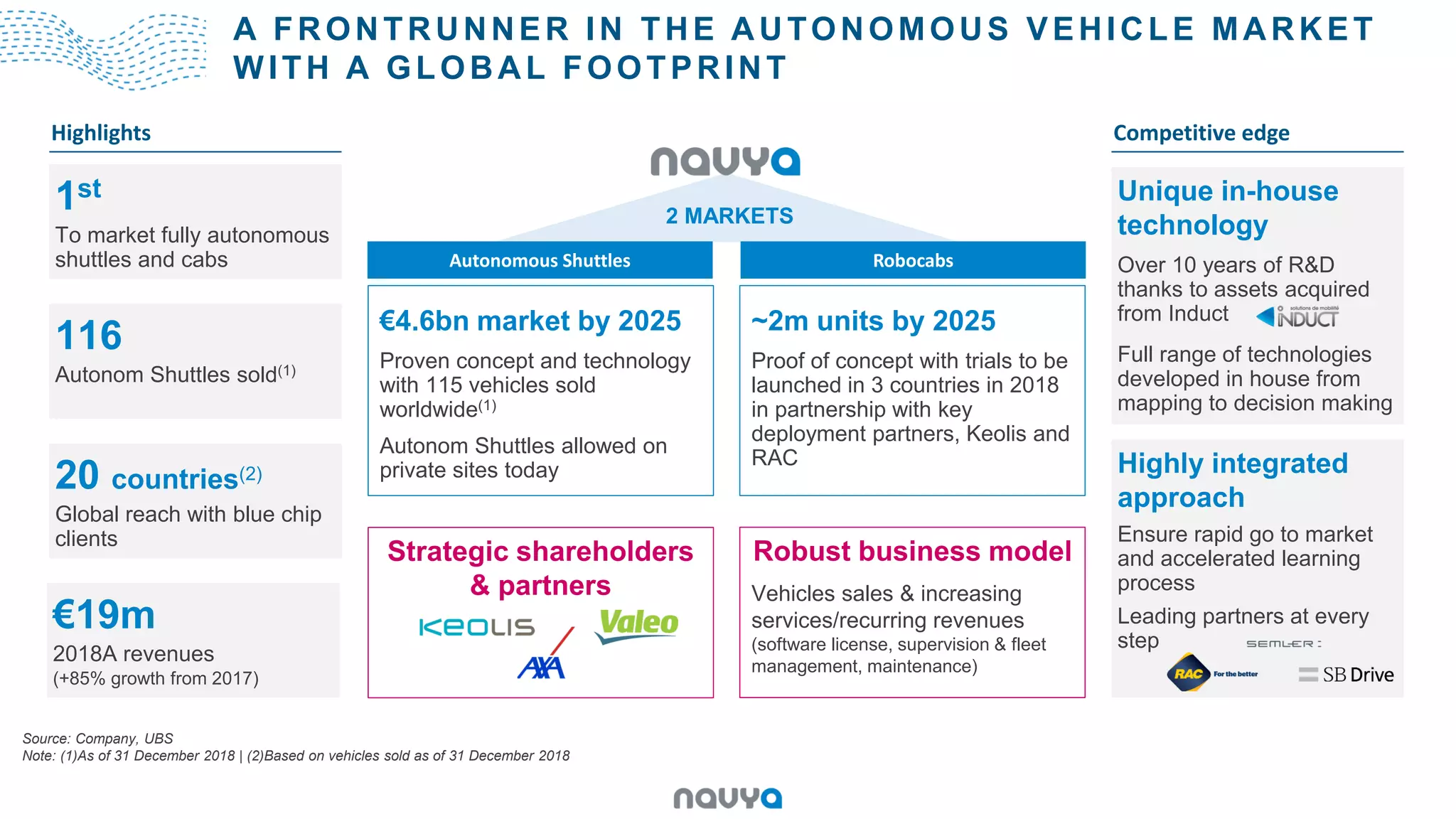

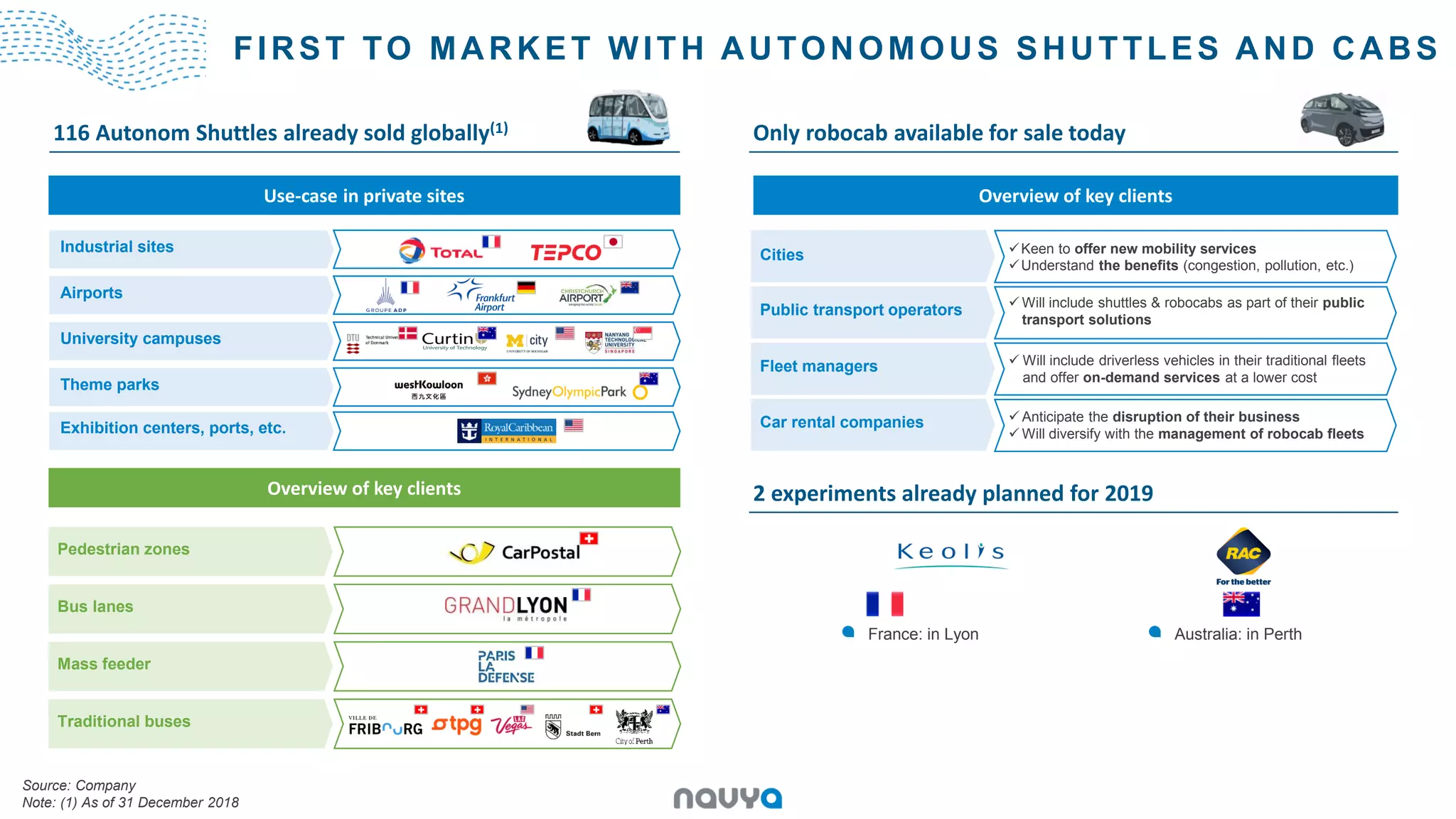

The document outlines the advancements and market presence of a leader in autonomous vehicles, specifically their shuttles and cabs, with 116 units sold across 20 countries as of December 2018. It details a robust business model supported by unique in-house technology developed over a decade, forecasting a €4.6bn market by 2025. Key features include a focus on integrated solutions, a rapid go-to-market strategy, and deployment in various settings such as airports and urban areas.

![[NOVABUILD] Livret électoral CA 2021-2024](https://cdn.slidesharecdn.com/ss_thumbnails/livretelectoralvf-210302091555-thumbnail.jpg?width=640&height=640&fit=bounds)

![[NOVABUILD] Intervention de Romain MARTEN | Présentation de la dynamique régi...](https://cdn.slidesharecdn.com/ss_thumbnails/191129-reseco-novabuild-191205133935-thumbnail.jpg?width=640&height=640&fit=bounds)

![[NOVABUILD] La Smart Building Alliance (SBA) et le cadre de référence R2S Rés...](https://cdn.slidesharecdn.com/ss_thumbnails/r2sresidentielsbadec2019-191205102956-thumbnail.jpg?width=640&height=640&fit=bounds)

![[NOVABUILD-JedisBIM] Présentation Vendée Eau 06/06/2019](https://cdn.slidesharecdn.com/ss_thumbnails/2-190607083401-thumbnail.jpg?width=640&height=640&fit=bounds)

![[NOVABUILD-JedisBIM] Présentation Atlancad 06/06/2019](https://cdn.slidesharecdn.com/ss_thumbnails/1-190607083356-thumbnail.jpg?width=640&height=640&fit=bounds)