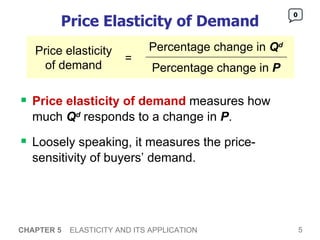

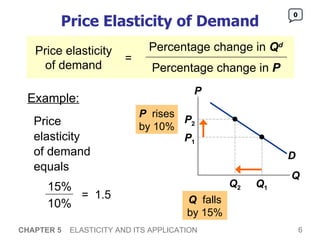

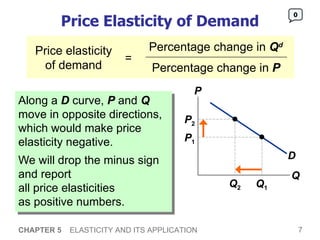

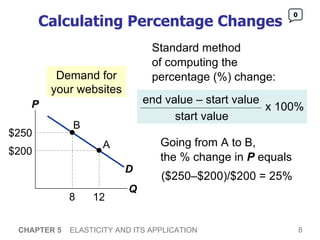

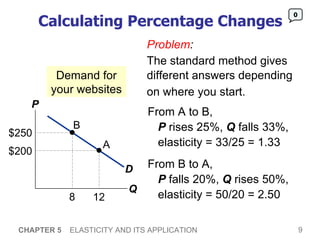

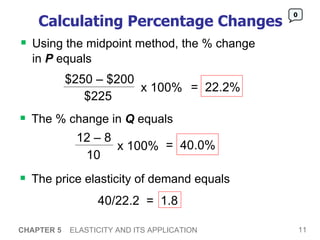

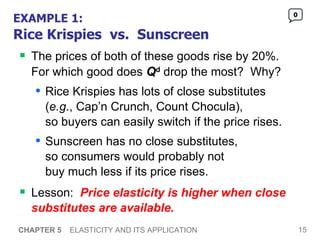

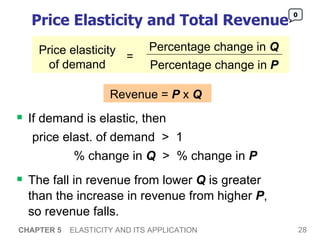

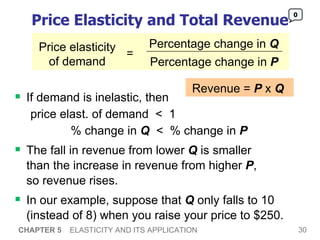

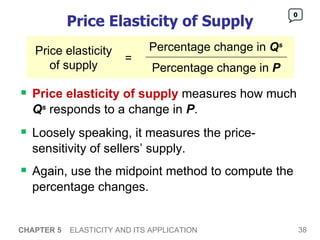

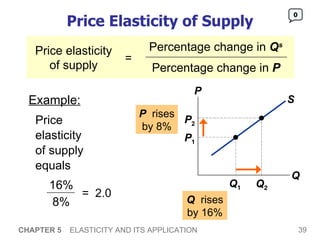

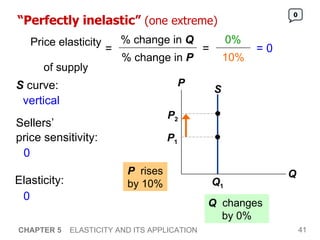

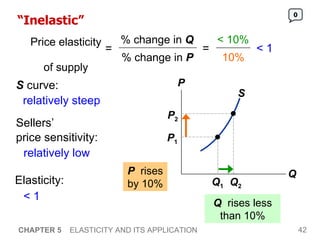

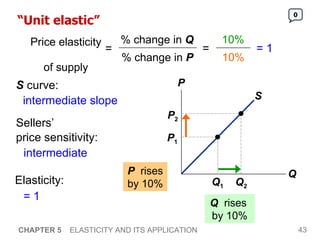

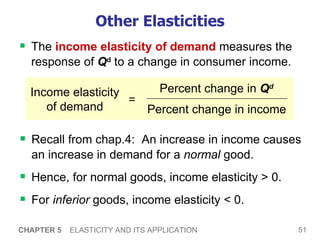

This chapter discusses elasticity, which measures how responsive one variable is to changes in another variable. It focuses on price elasticity of demand, which measures how much quantity demanded responds to changes in price. Price elasticity is calculated as the percentage change in quantity divided by the percentage change in price. Examples are used to illustrate factors that determine whether demand is elastic or inelastic, such as availability of substitutes. The elasticity also depends on whether a good is a necessity. The chapter explores how elasticity is related to the slope of the demand curve and total revenue.