Based on the market research, the value-based price for the motorbike would be Rs. 38,000. This price reflects the consumers' perceived value based on the key features and benefits of the product.

PRICING CONSIDERATIONS AND

PRICINGAPPROCHES

Dr. M. Umamageswari

Assistant Professor (Agricultural Economics)

JSA College of Agriculture &Technology

(Affiliated toTamil Nadu Agricultural University)

Ma. Podaiyur,TittagudiTk. ,

Cuddalore District – 606 108

2.

PRICE

Simply Defined

Theamount of money charged for a product or

service

Broadly Defined

The sum of the values that consumers exchange for

the benefits of having or using the product or

service.

3.

Price

Price hasbeen the major factor affecting

buyer choice (Historically)

Recent times – Non price factors influencing

majorly

Determine very much of a firm’s market

share and its profitability

4.

Price

Only Marketingmix element that produces

revenue

(Product - It must be developed and produced,

Place - facility and transportation costs, and

Promotion - costly anyway )

Flexible – Marketing mix rather than others

Changing too much chases away potential

customers and charging too low cuts revenue

Marketing Objectives that

AffectPricing Decisions

Marketing

Objectives

Survival

Low Prices to Cover Variable Costs and

Some Fixed Costs to Stay in Business.

Current Profit Maximization

Choose the Price that Produces the

Maximum Current Profit, Cash Flow or ROI.

Market Share Leadership

Low as Possible Prices to Become

the Market Share Leader.

Product Quality Leadership

High Prices to Cover Higher

Performance Quality

9.

Marketing Mix Variablesthat Affect

Pricing Decisions

Marketing-Mix

Strategy

Product Design

and Quality

Distribution

Promotion

Non-Price

Factors

10.

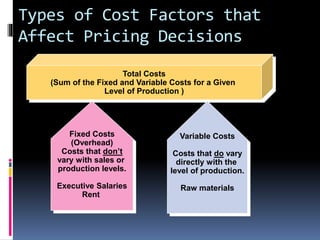

Types of CostFactors that

Affect Pricing Decisions

Total Costs

(Sum of the Fixed and Variable Costs for a Given

Level of Production )

Variable Costs

Costs that do vary

directly with the

level of production.

Raw materials

Fixed Costs

(Overhead)

Costs that don’t

vary with sales or

production levels.

Executive Salaries

Rent

11.

External Factors AffectingPricing

Decisions

Market and

Demand

Competitors’ Costs,

Prices, and Offers

Other External Factors

Economic Conditions

Reseller Needs

Government Actions

Social Concerns

12.

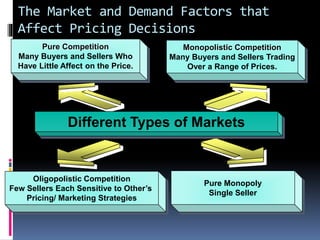

The Market andDemand Factors that

Affect Pricing Decisions

Pure Competition

Many Buyers and Sellers Who

Have Little Affect on the Price.

Monopolistic Competition

Many Buyers and Sellers Trading

Over a Range of Prices.

Oligopolistic Competition

Few Sellers Each Sensitive to Other’s

Pricing/ Marketing Strategies

Pure Monopoly

Single Seller

Different Types of Markets

13.

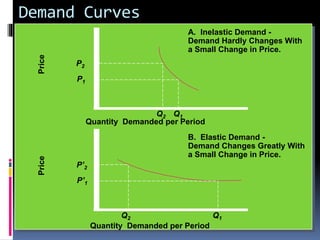

Demand Curves

Price

Quantity Demandedper Period

A. Inelastic Demand -

Demand Hardly Changes With

a Small Change in Price.

P2

P1

Q1Q2

Price

Quantity Demanded per Period

P’2

P’1

Q1Q2

B. Elastic Demand -

Demand Changes Greatly With

a Small Change in Price.

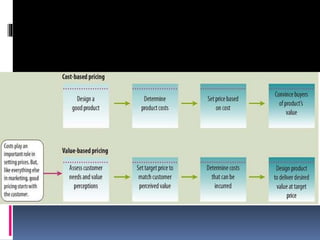

Cost based pricing

Add a markup to the cost base to determine

a prospective selling price

Usually it is only a starting point in the price

setting process

The markup is somewhat flexible, based

partially on customers and competitors

Because a markup is added, cost based

pricing is often called as cost plus pricing,

where the plus refers to markup component.

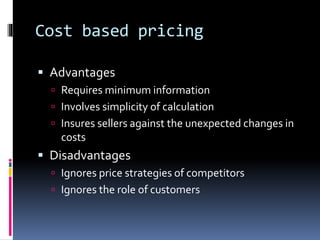

Cost based pricing

Advantages

Requires minimum information

Involves simplicity of calculation

Insures sellers against the unexpected changes in

costs

Disadvantages

Ignores price strategies of competitors

Ignores the role of customers

18.

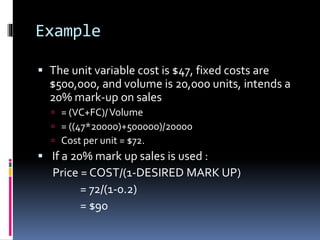

Example

The unitvariable cost is $47, fixed costs are

$500,000, and volume is 20,000 units, intends a

20% mark-up on sales

= (VC+FC)/Volume

= ((47*20000)+500000)/20000

Cost per unit = $72.

If a 20% mark up sales is used :

Price = COST/(1-DESIRED MARK UP)

= 72/(1-0.2)

= $90

19.

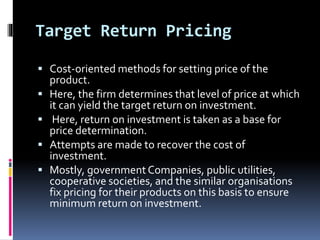

Target Return Pricing

Cost-oriented methods for setting price of the

product.

Here, the firm determines that level of price at which

it can yield the target return on investment.

Here, return on investment is taken as a base for

price determination.

Attempts are made to recover the cost of

investment.

Mostly, governmentCompanies, public utilities,

cooperative societies, and the similar organisations

fix pricing for their products on this basis to ensure

minimum return on investment.

20.

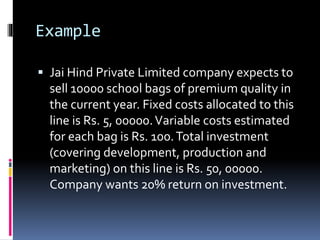

Example

Jai HindPrivate Limited company expects to

sell 10000 school bags of premium quality in

the current year. Fixed costs allocated to this

line is Rs. 5, 00000.Variable costs estimated

for each bag is Rs. 100.Total investment

(covering development, production and

marketing) on this line is Rs. 50, 00000.

Company wants 20% return on investment.

21.

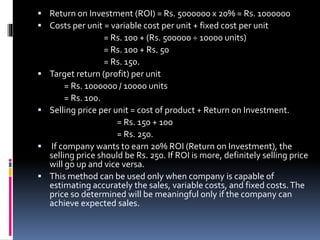

Return onInvestment (ROI) = Rs. 5000000 x 20% = Rs. 1000000

Costs per unit = variable cost per unit + fixed cost per unit

= Rs. 100 + (Rs. 500000 ÷ 10000 units)

= Rs. 100 + Rs. 50

= Rs. 150.

Target return (profit) per unit

= Rs. 1000000 / 10000 units

= Rs. 100.

Selling price per unit = cost of product + Return on Investment.

= Rs. 150 + 100

= Rs. 250.

If company wants to earn 20% ROI (Return on Investment), the

selling price should be Rs. 250. If ROI is more, definitely selling price

will go up and vice versa.

This method can be used only when company is capable of

estimating accurately the sales, variable costs, and fixed costs.The

price so determined will be meaningful only if the company can

achieve expected sales.

22.

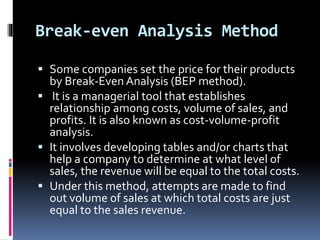

Break-even Analysis Method

Some companies set the price for their products

by Break-Even Analysis (BEP method).

It is a managerial tool that establishes

relationship among costs, volume of sales, and

profits. It is also known as cost-volume-profit

analysis.

It involves developing tables and/or charts that

help a company to determine at what level of

sales, the revenue will be equal to the total costs.

Under this method, attempts are made to find

out volume of sales at which total costs are just

equal to the sales revenue.

23.

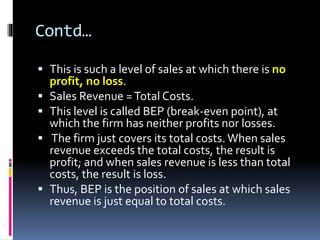

Contd…

This issuch a level of sales at which there is no

profit, no loss.

Sales Revenue =Total Costs.

This level is called BEP (break-even point), at

which the firm has neither profits nor losses.

The firm just covers its total costs. When sales

revenue exceeds the total costs, the result is

profit; and when sales revenue is less than total

costs, the result is loss.

Thus, BEP is the position of sales at which sales

revenue is just equal to total costs.

24.

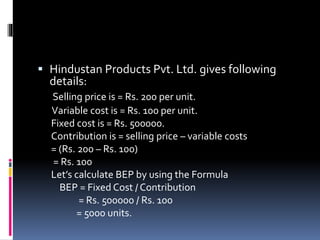

Hindustan ProductsPvt. Ltd. gives following

details:

Selling price is = Rs. 200 per unit.

Variable cost is = Rs. 100 per unit.

Fixed cost is = Rs. 500000.

Contribution is = selling price – variable costs

= (Rs. 200 – Rs. 100)

= Rs. 100

Let’s calculate BEP by using the Formula

BEP = Fixed Cost / Contribution

= Rs. 500000 / Rs. 100

= 5000 units.

25.

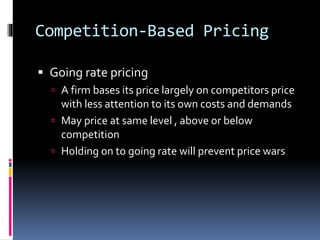

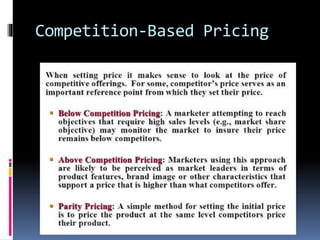

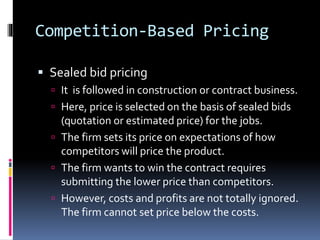

Competition-Based Pricing

Goingrate pricing

A firm bases its price largely on competitors price

with less attention to its own costs and demands

May price at same level , above or below

competition

Holding on to going rate will prevent price wars

Competition-Based Pricing

Sealedbid pricing

It is followed in construction or contract business.

Here, price is selected on the basis of sealed bids

(quotation or estimated price) for the jobs.

The firm sets its price on expectations of how

competitors will price the product.

The firm wants to win the contract requires

submitting the lower price than competitors.

However, costs and profits are not totally ignored.

The firm cannot set price below the costs.

28.

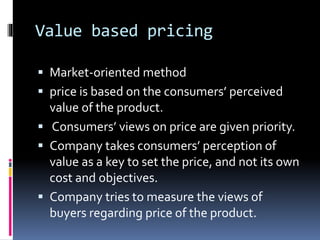

Value based pricing

Market-oriented method

price is based on the consumers’ perceived

value of the product.

Consumers’ views on price are given priority.

Company takes consumers’ perception of

value as a key to set the price, and not its own

cost and objectives.

Company tries to measure the views of

buyers regarding price of the product.

29.

Set price forthe motorbike:

Market Research;

Buyers respond as under:

Rs. 30000 if the bike is similar to competitors’ motorbikes

Rs. 2000 is the price premium for novelty, shape, new getup, and

colour.

Rs. 3000 is price premium for the highest mileage per litre petrol.

Rs. 2000 is price premium for replacement guarantee and two

extra free services.

Rs. 2000 is price premium for durability and reliability.

Rs. 1000 is price premium for special safety measures.

Rs. 40000 is the normal price as per consumers’ perception.

Rs. 2000 discount is for DIWALI special offer.

Rs. 38000 is final ex-showroom price as per consumers’ views (or

perception).