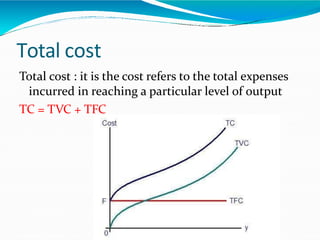

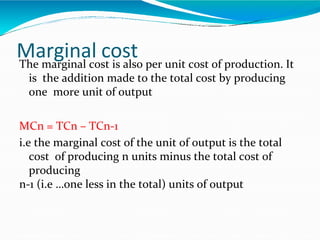

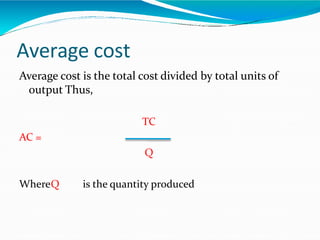

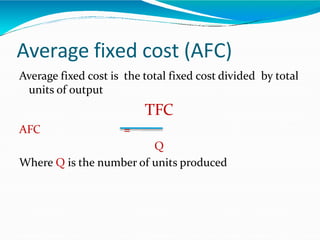

This document defines and explains the different types of costs that a business may incur. It outlines opportunity cost versus actual cost, direct versus indirect costs, fixed versus variable costs, average versus marginal costs. Specific types of costs covered include explicit and implicit costs, historical and replacement costs, real and prime costs, total costs. The document provides examples and definitions for each cost type to clarify the concepts and how they are used in managerial decision making.