Download to read offline

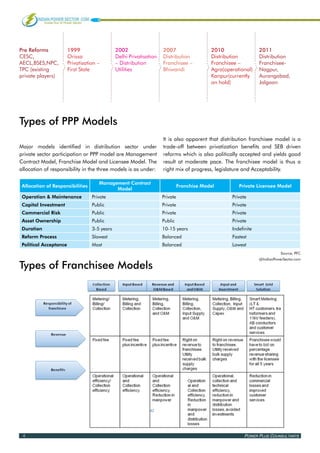

The document discusses power distribution in India, focusing on distribution franchisees. It provides an overview of the current state of power distribution, including high AT&C losses around 27% on average. Distribution utilities have been losing money, with aggregate losses increasing from 2008-2009 to 2009-2010 before decreasing in 2010-2011. The document discusses steps taken to privatize distribution, including different models of private sector participation like management contracts, franchise models, and private licensees. It provides examples of recent distribution franchise deals across several states. Key benefits to utilities and franchisees from franchise models are outlined. Issues around standardizing bidding documents for franchisees are also mentioned.