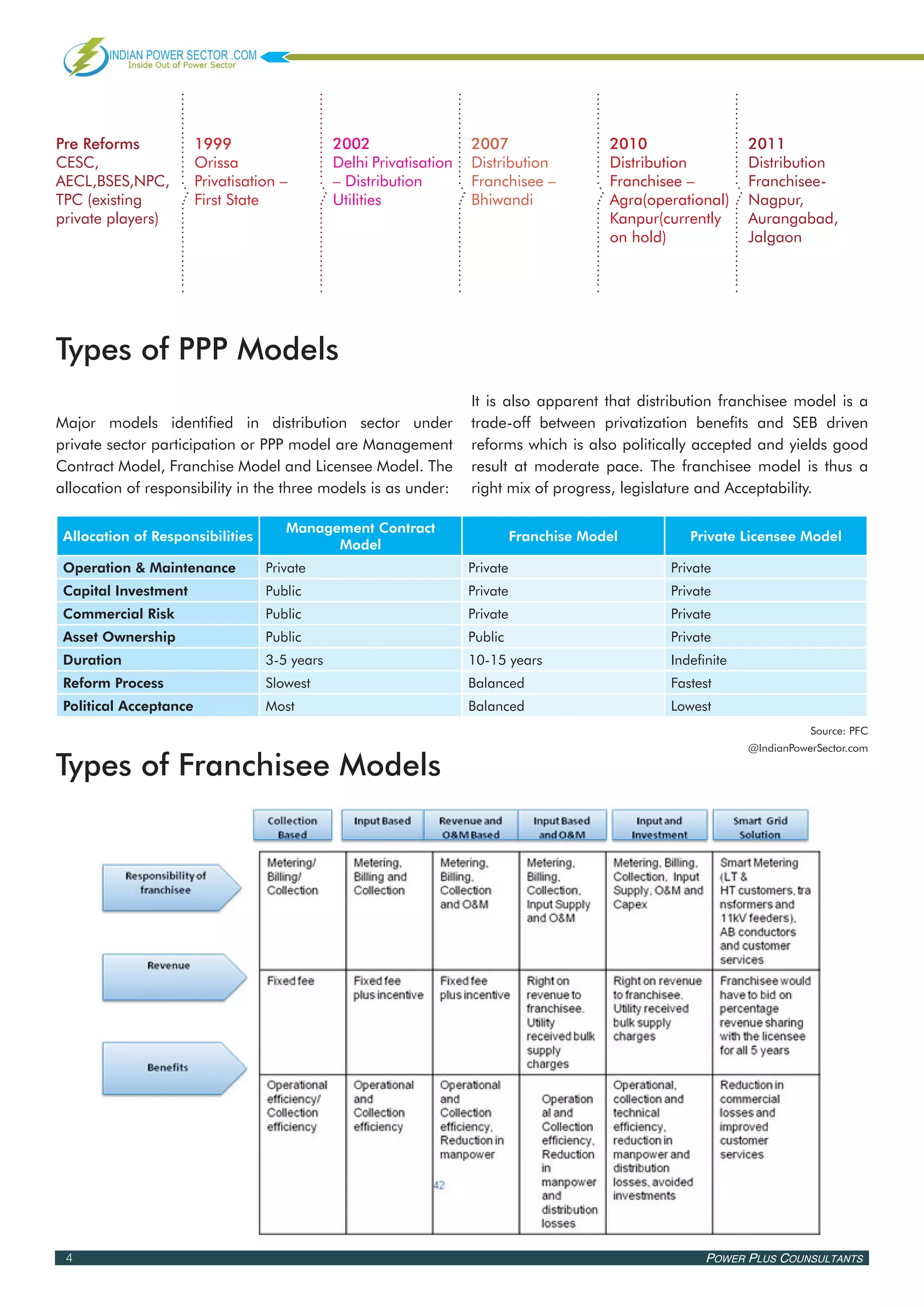

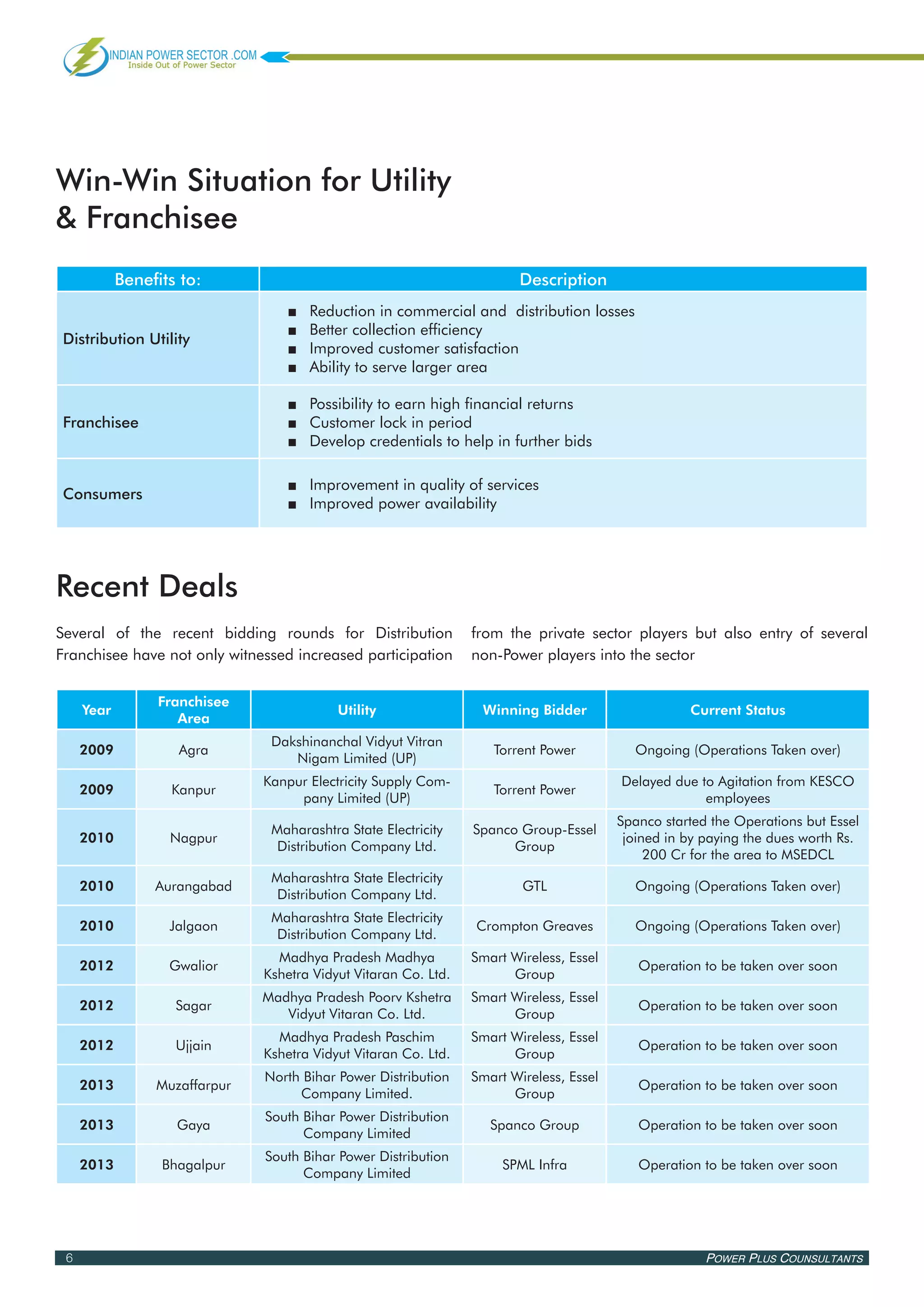

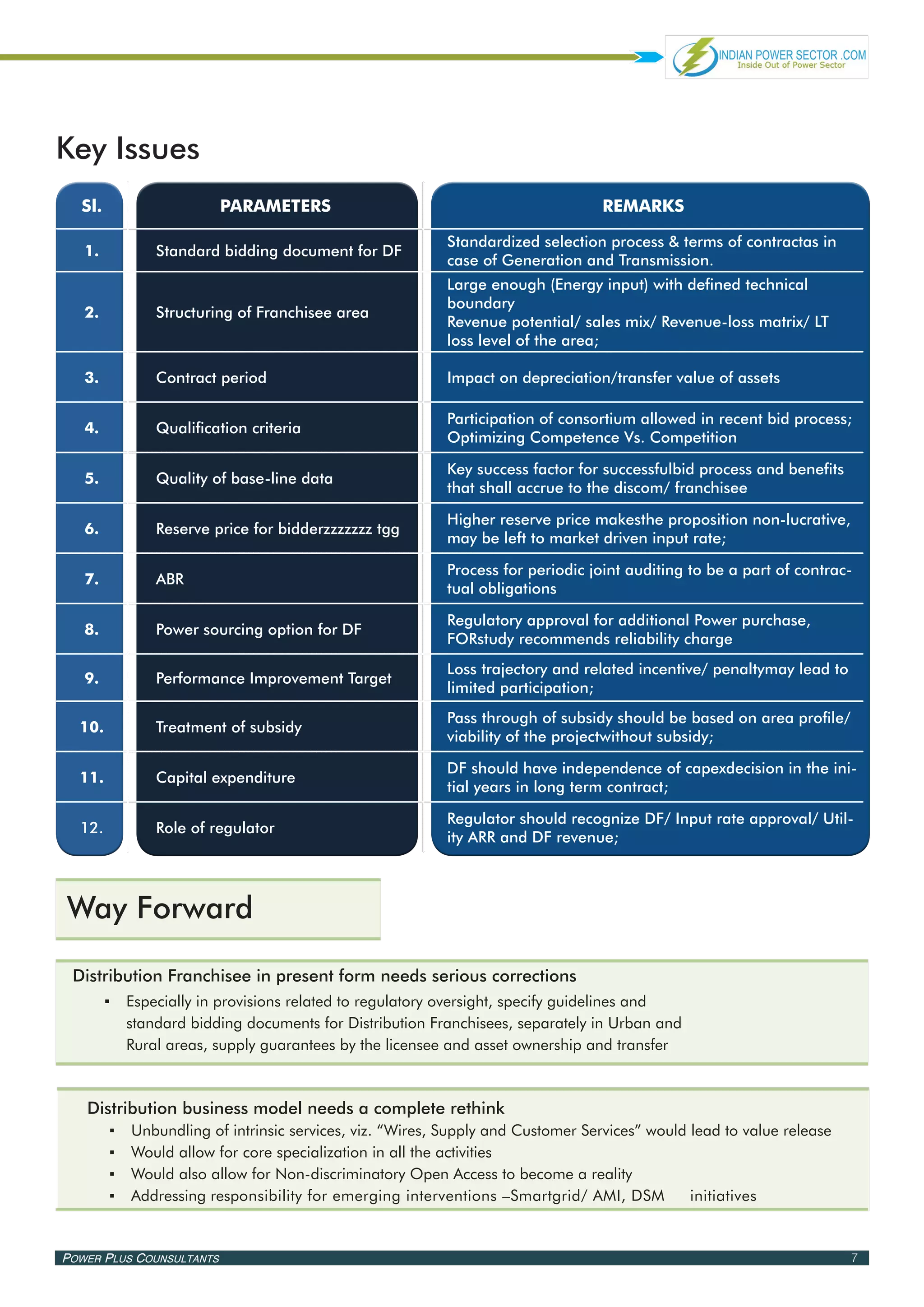

The document discusses power distribution in India, focusing on distribution franchisees. It provides an overview of the current state of power distribution, noting high AT&C losses around 27% on average. Distribution franchisees are presented as a form of public-private partnership that provides flexibility. The types of franchise models are described, including management contracts, franchise models, and private licensee models. Recent deals involving distribution franchisees are listed. Key issues related to franchisee area structuring, contract period, qualification criteria, and reserve pricing are identified. Benefits to utilities, franchisees, and consumers are outlined.

![[Smart Grid Market Research] (Part 1 of 3 Part Series): The U.S. Smart Meter ...](https://cdn.slidesharecdn.com/ss_thumbnails/theussmartmeteruprisingaugust2011zprymeresearch-110823160207-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)