Downloaded 39 times

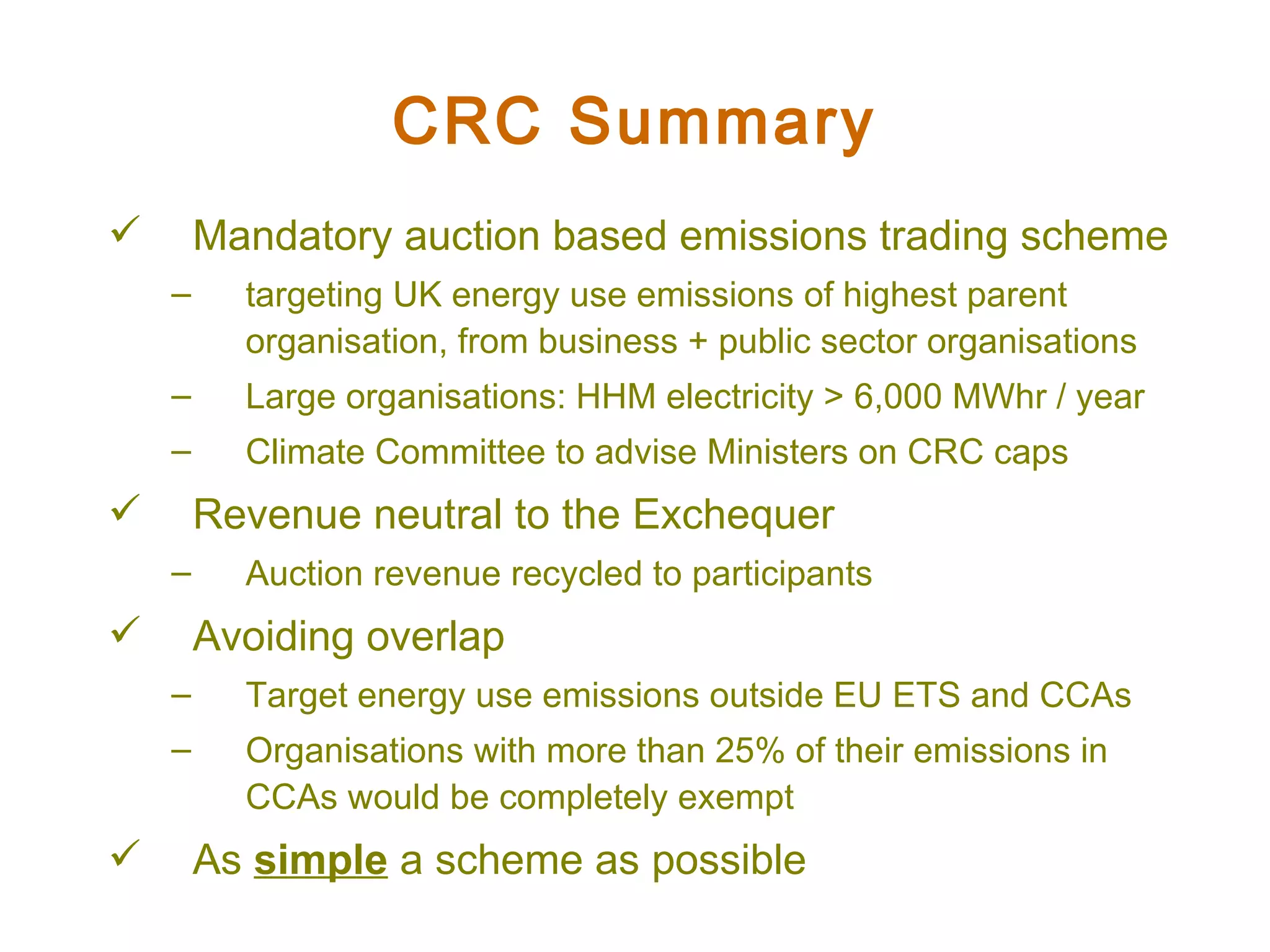

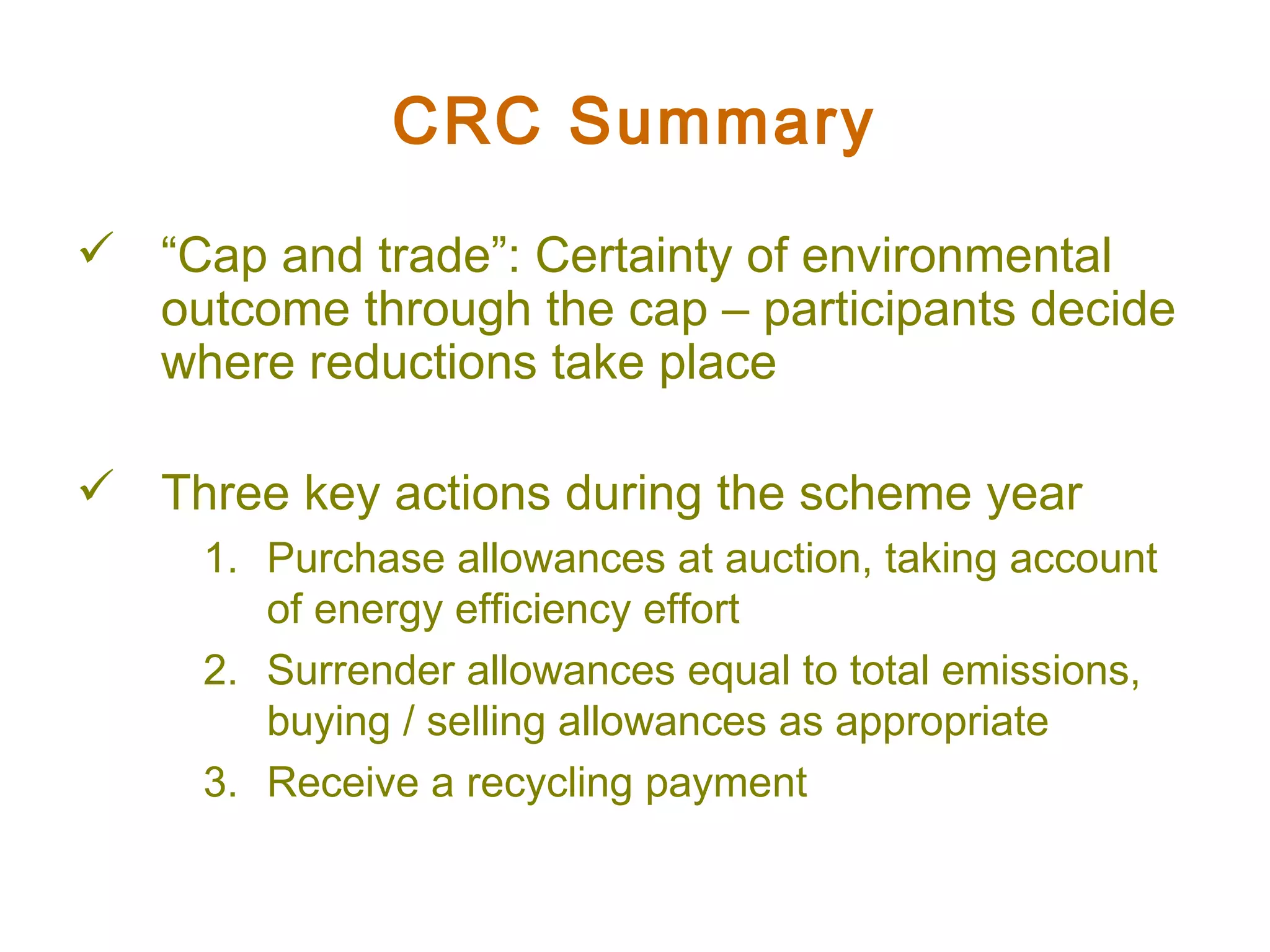

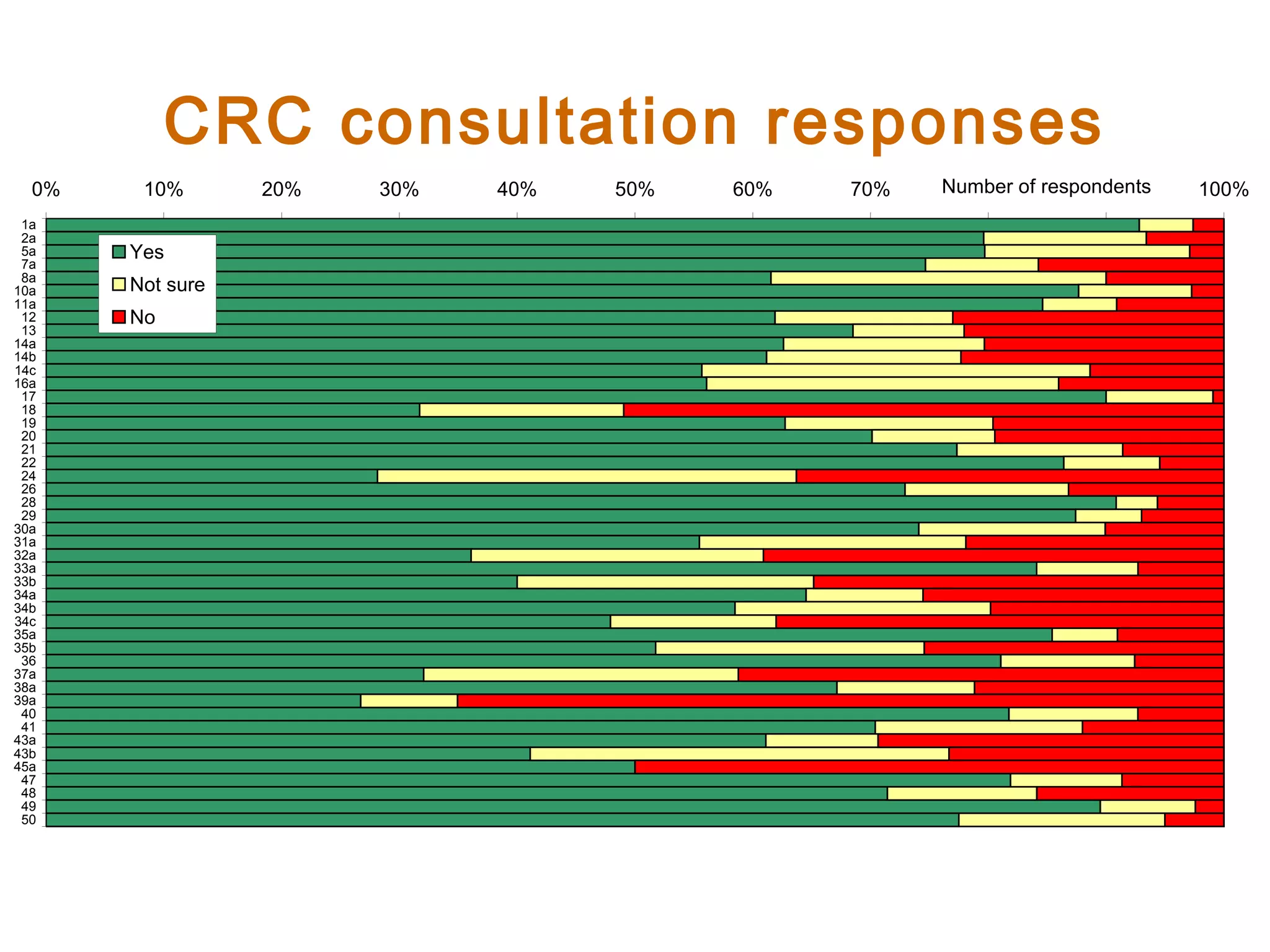

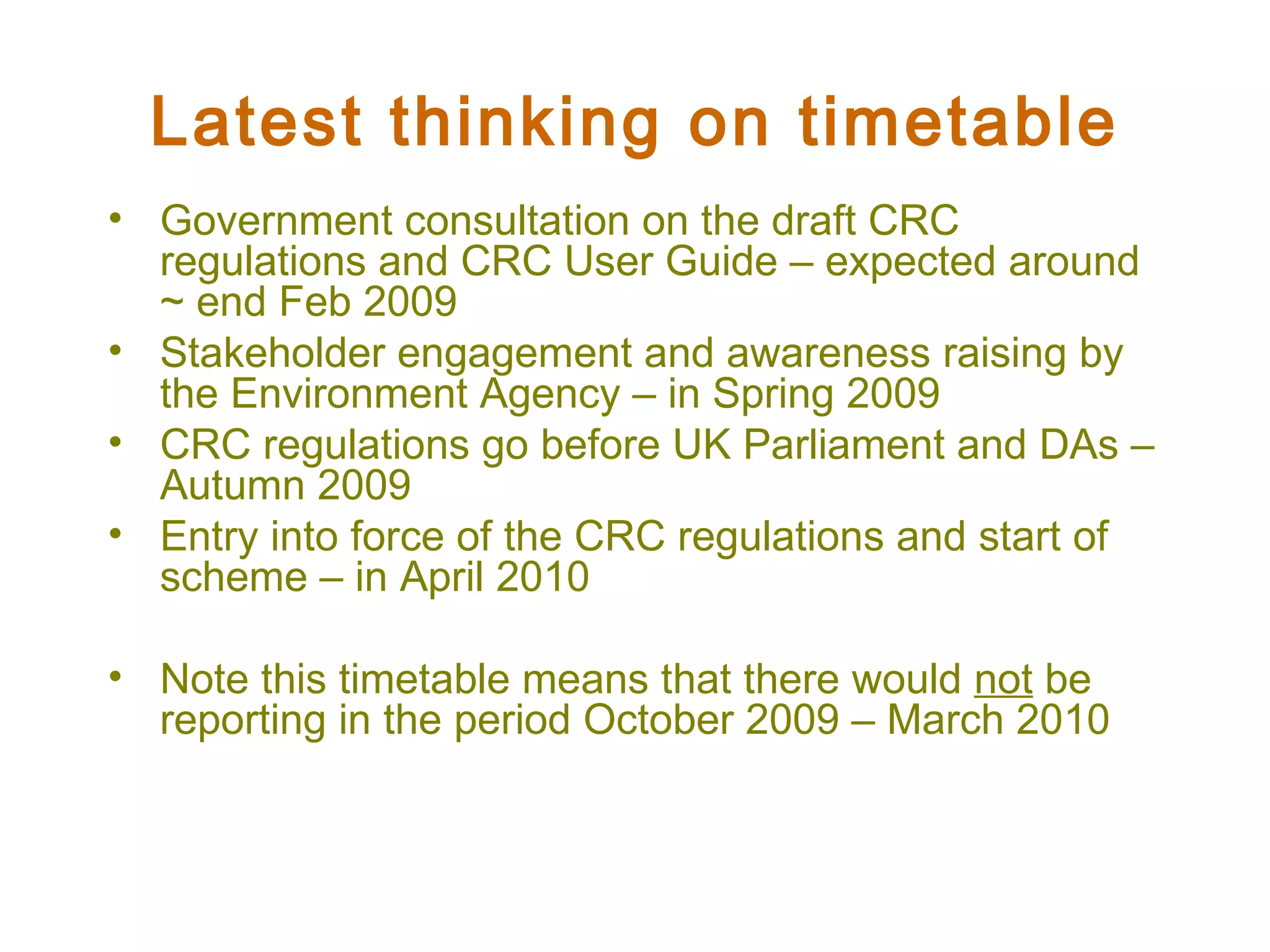

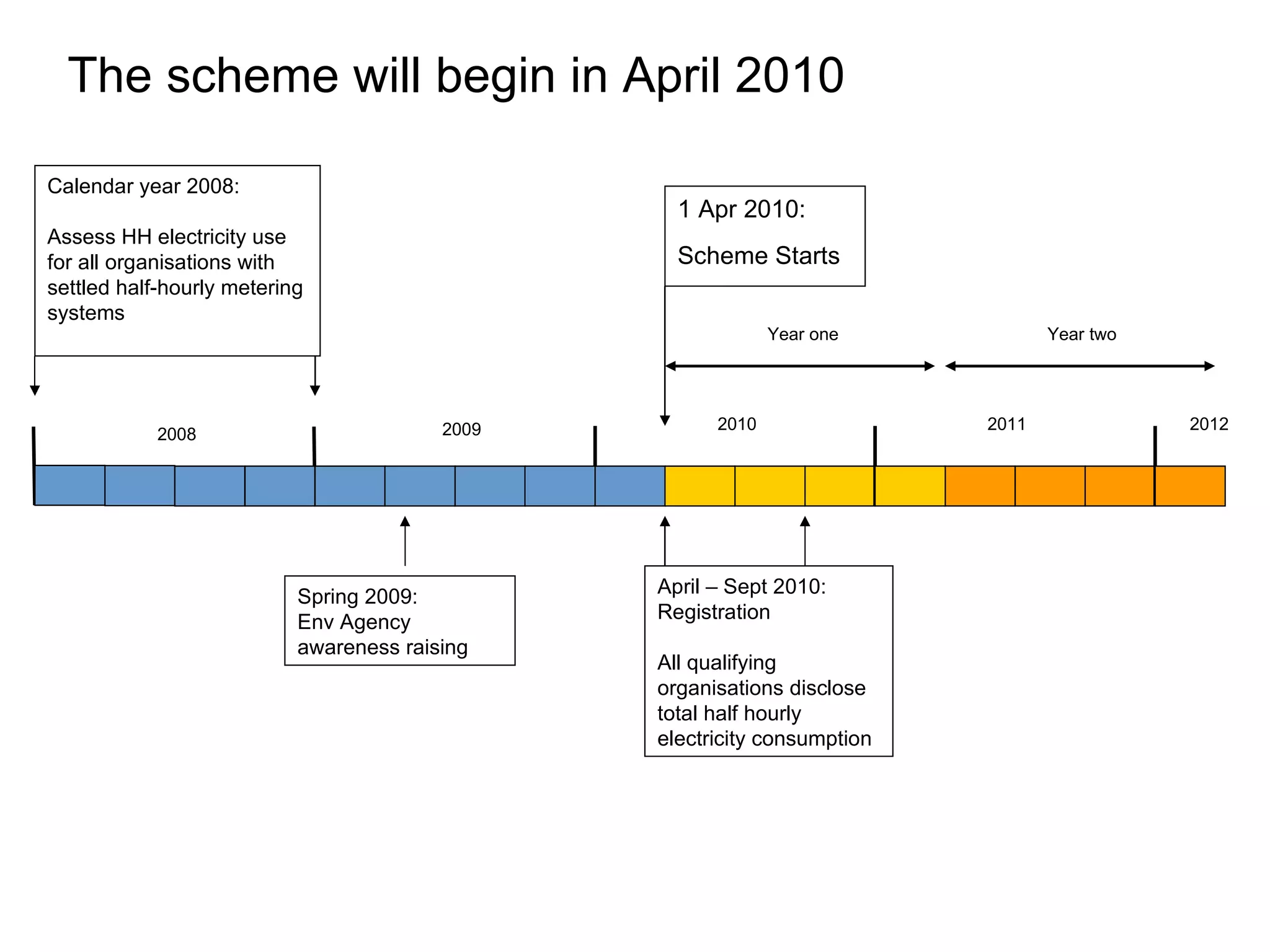

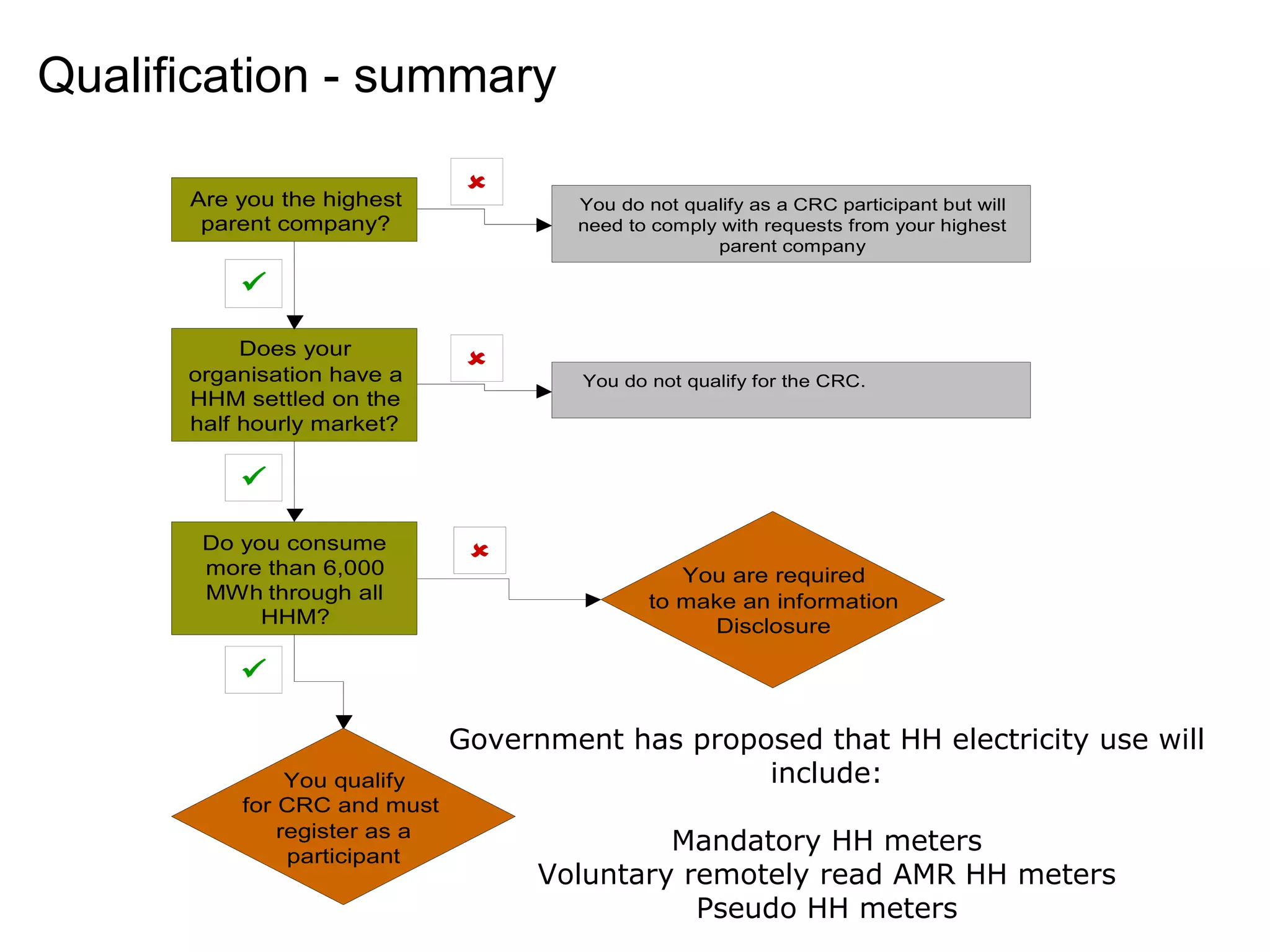

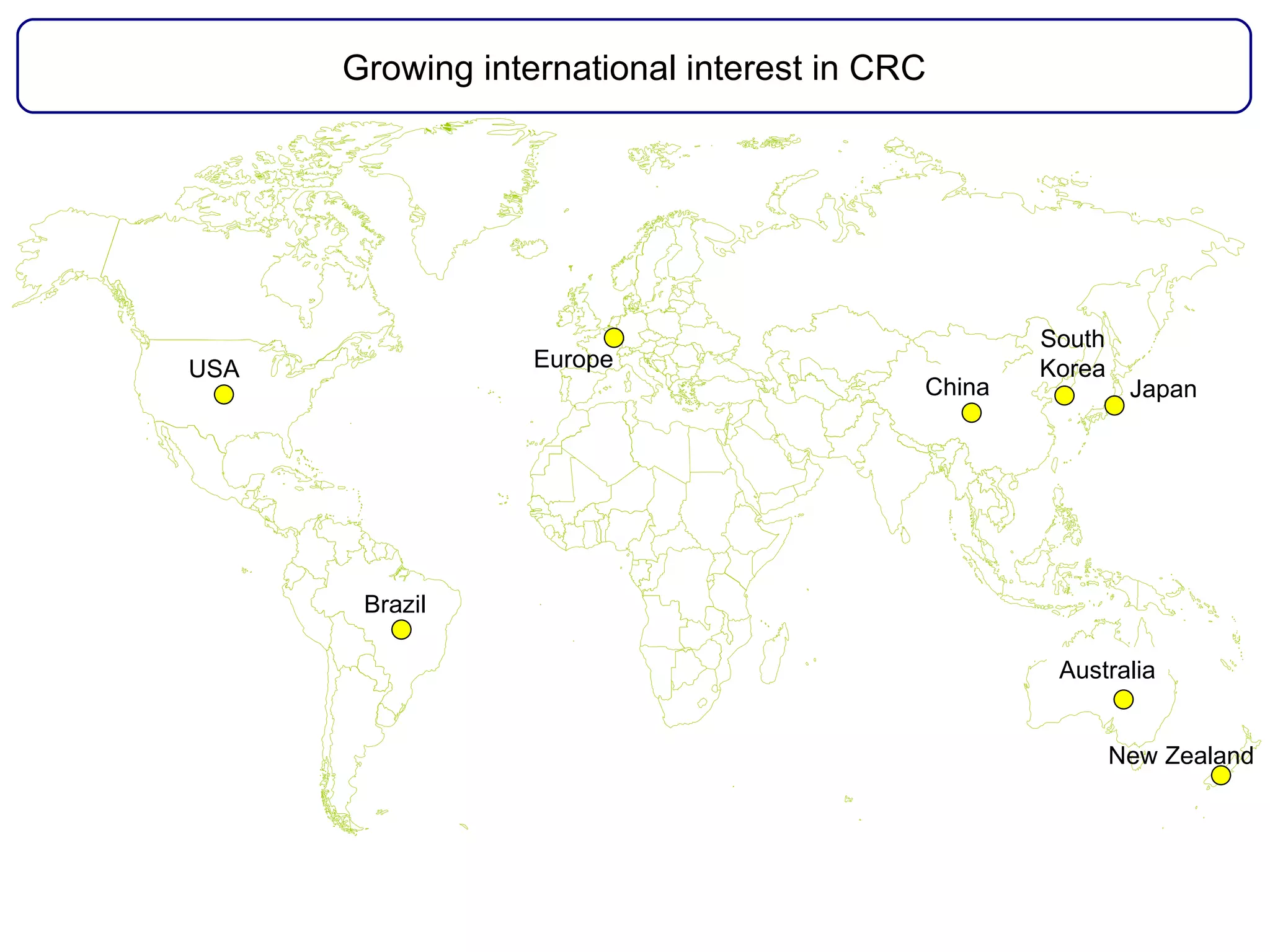

The document outlines the Carbon Reduction Commitment (CRC), a mandatory auction-based emissions trading scheme targeting energy use emissions in the UK from large organizations. Key elements include a cap-and-trade system, participant actions for purchasing and surrendering allowances, and a focus on revenue recycling to support compliance and improve energy efficiency. Additionally, it discusses the consultation process, stakeholders' concerns, and implementation timetables leading to the scheme's start in April 2010.