PCI DSS

• Developedby the five major card brands, to address potential areas of vulnerability

and guide organizations in best practices to maintain the integrity of cardholder data.

• Anyone handling payment card details must adhere to.

• Failure to comply could result in:

• Significant fines from the card brands

• Inability to accept credit cards for payment

• Damage to brand/reputation

4.

PCI DSS

• ThePayment Card Industry Data Security Standard (PCI DSS) is a set of

requirements intended to ensure that all companies that process, store, or

transmit credit card information maintain a secure environment.

• The PCI DSS applies to all entities that store, process, and/or transmit

cardholder data. It covers technical and operational system components

included in or connected to cardholder data. If you are a merchant who

accepts or processes payment cards, you must comply with the PCI DSS.

• All organizations that retain, process, and transmit cardholder data, such as

merchants who are members of card issuing companies and any other service

providers should all consider compliance with PCI DSS.

5.

History

• The PaymentCard Industry Data Security

Standard (PCI DSS) is the unified global standard

for cardholder data security established by five

international payment card brands (VISA,

MasterCard, JCB, AMEX and Discover). This is the

data security standard that multilaterally

specifies requirements of security management,

policies, procedures and methods, network

configurations and software design to protect

other cardholder data.

• Each of these five international payment card

brands support compliance with PCI DSS and

strives to promote the adoption.

7

What is PCI-DSS?

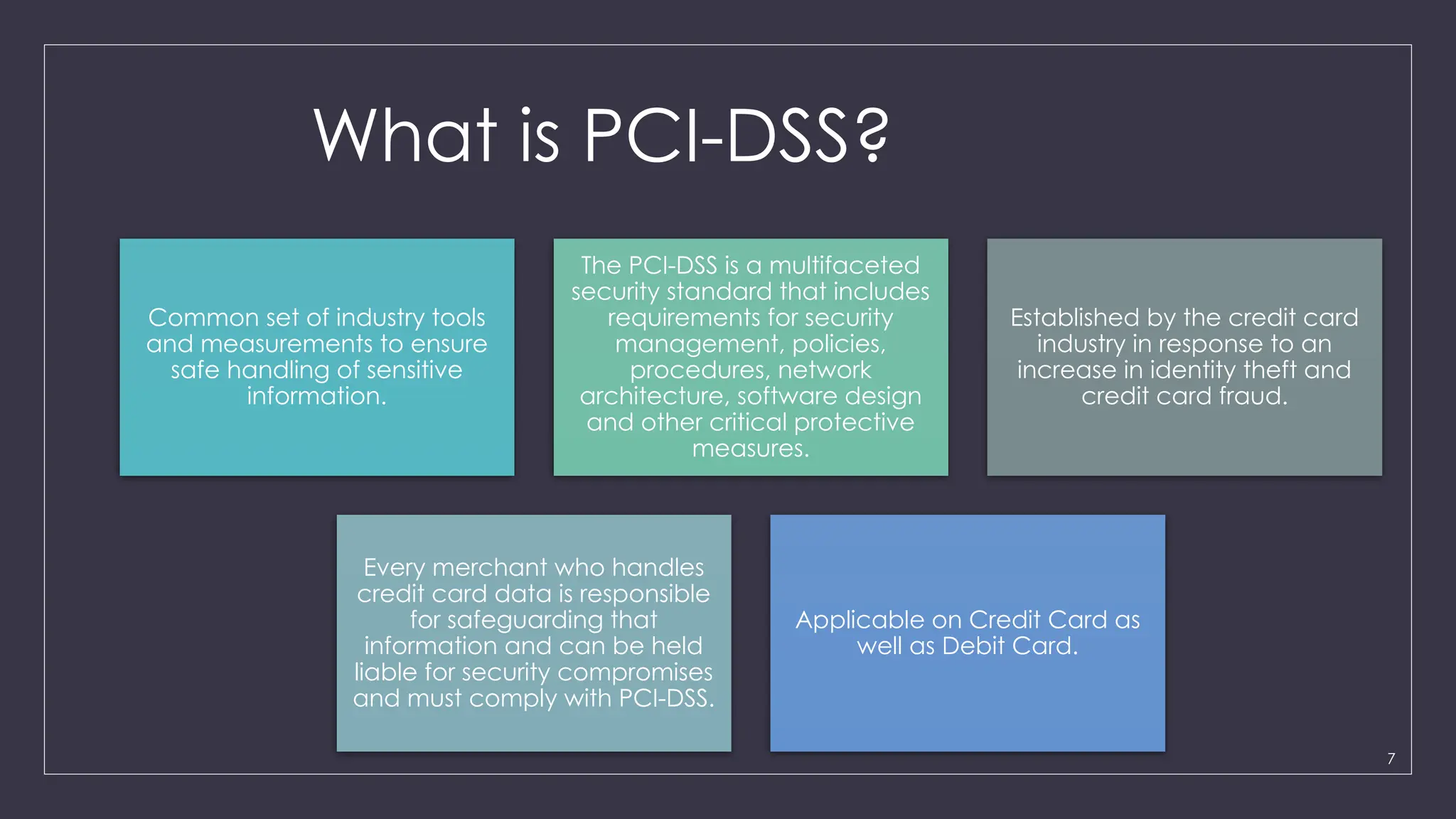

Commonset of industry tools

and measurements to ensure

safe handling of sensitive

information.

The PCI-DSS is a multifaceted

security standard that includes

requirements for security

management, policies,

procedures, network

architecture, software design

and other critical protective

measures.

Established by the credit card

industry in response to an

increase in identity theft and

credit card fraud.

Every merchant who handles

credit card data is responsible

for safeguarding that

information and can be held

liable for security compromises

and must comply with PCI-DSS.

Applicable on Credit Card as

well as Debit Card.

8.

Background

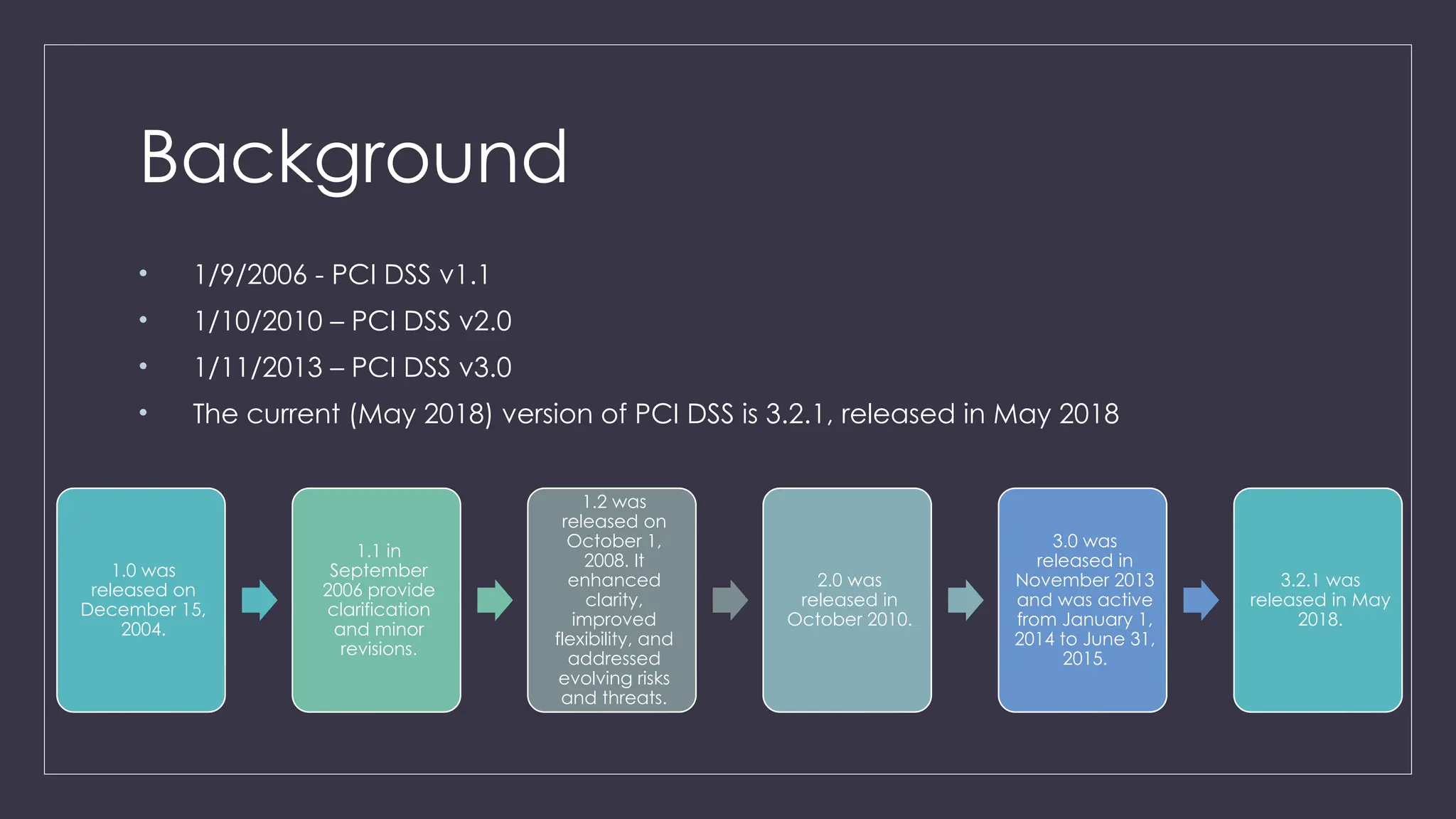

• 1/9/2006 -PCI DSS v1.1

• 1/10/2010 – PCI DSS v2.0

• 1/11/2013 – PCI DSS v3.0

• The current (May 2018) version of PCI DSS is 3.2.1, released in May 2018

1.0 was

released on

December 15,

2004.

1.1 in

September

2006 provide

clarification

and minor

revisions.

1.2 was

released on

October 1,

2008. It

enhanced

clarity,

improved

flexibility, and

addressed

evolving risks

and threats.

2.0 was

released in

October 2010.

3.0 was

released in

November 2013

and was active

from January 1,

2014 to June 31,

2015.

3.2.1 was

released in May

2018.

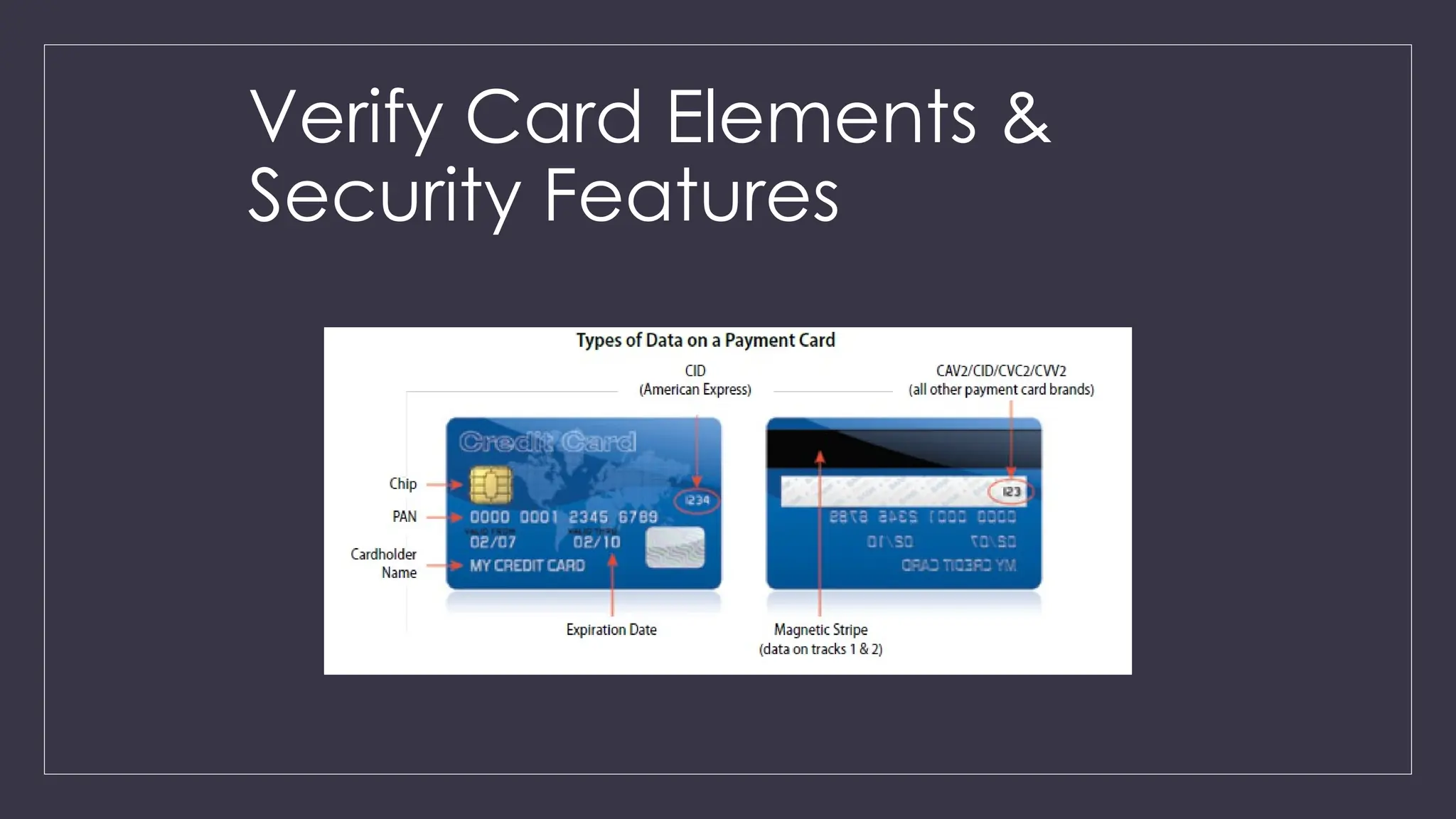

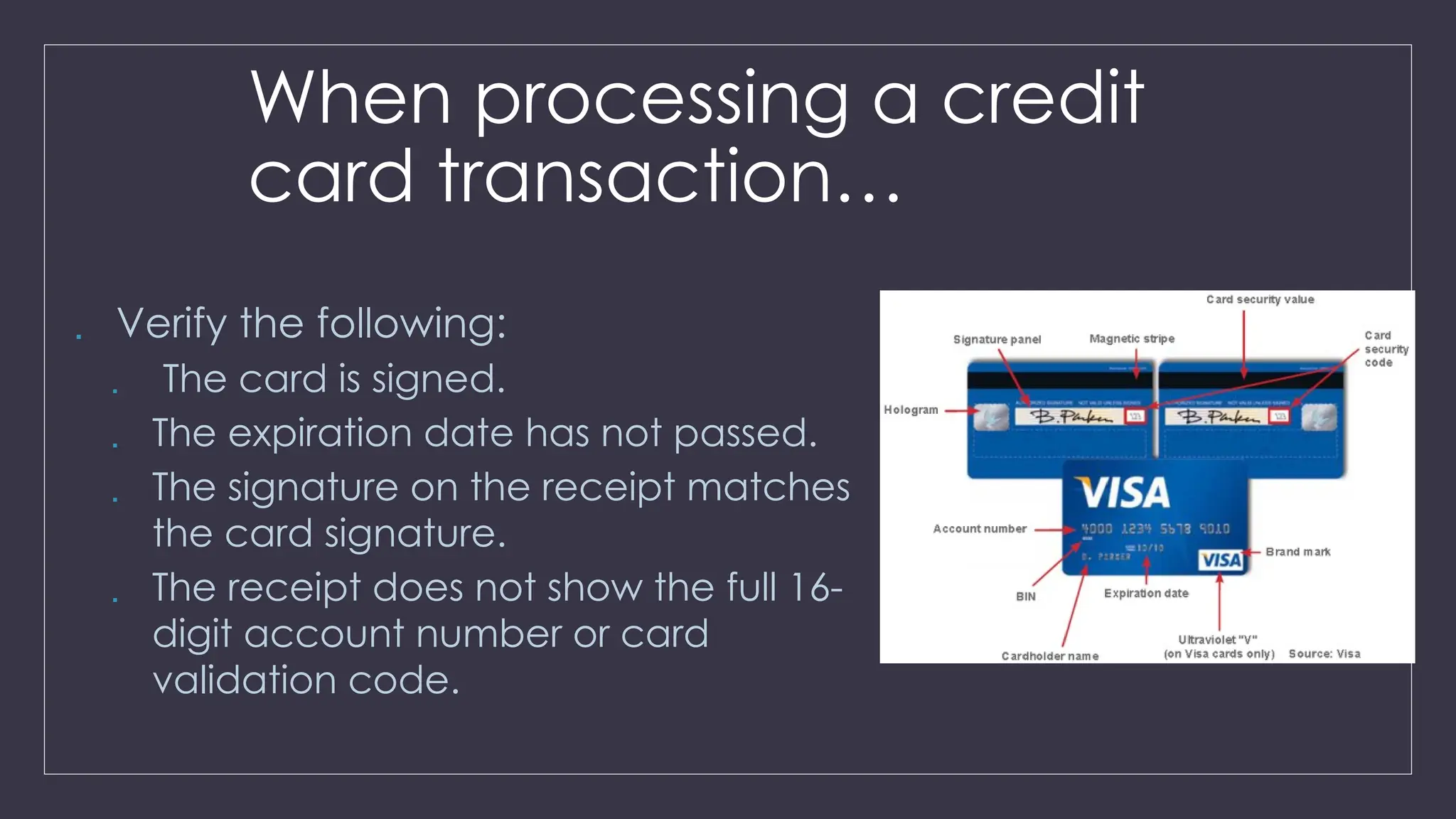

When processing acredit

card transaction…

Verify the following:

The card is signed.

The expiration date has not passed.

The signature on the receipt matches

the card signature.

The receipt does not show the full 16-

digit account number or card

validation code.

12.

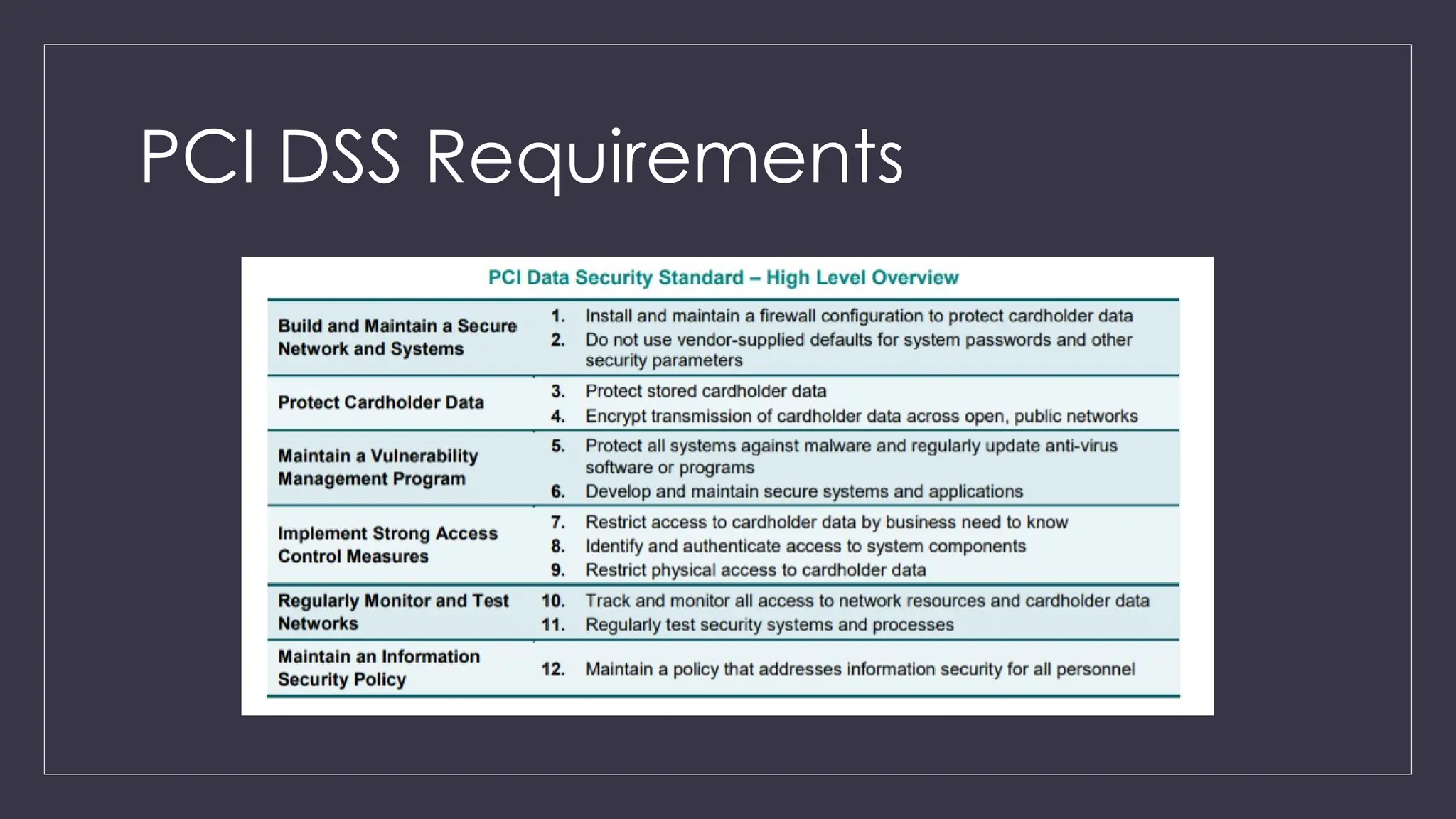

12 requirements

1. Protectyour system with firewalls

2. Configure passwords and settings

3. Protect stored cardholder data

4. Encrypt transmission of cardholder data across open, public networks

5. Use and regularly update anti-virus software

6. Regularly update and patch systems

7. Restrict access to cardholder data to business need to know

8. Assign a unique ID to each person with computer access

9. Restrict physical access to workplace and cardholder data

10. Implement logging and log management

11. Conduct vulnerability scans and penetration tests

12. Documentation and risk assessments

Compliance Levels

All companieswho are subject to PCI DSS standards

must be PCI compliant. There are four levels of PCI

Compliance and these are based on how much you

process per year, as well as other details about the level

of risk assessed by payment brands.

At a high level, the levels are following:

• Level 1 – Over 6 million transactions annually

• Level 2 – Between 1 and 6 million transactions annually

• Level 3 – Between 20,000 and 1 million transactions

annually

• Level 4 – Less than 20,000 transactions annually

16.

What can Ido?

1) Never see, store or have access to cardholder

data

2) Never tokenize credit card information

3) Never use third-party payment gateway

4) Logging, testing, audit trials before launching

website

5) Strictly follow security policies set by payment

partners

17.

Application

• PCI compliancecan be achieved by completing the Self-

Assessment Questionnaire (SAQ). The test you take depends on

how you integrate payment gateway and cardholder data.

• However, PCI certification requires a severe self-audit and a

special audit conducted by Qualified Security Assessor (QSA).

#8 The history of PCI-DSS begins in 2004. As payment fraud began to rise, credit card industry leaders convened to develop a common set of security standards. The PCI’s founding members—American Express, Discover Financial Services, JCB International, Mastercard and Visa—introduced PCI DSS 1.0 in December 2004.

#12 1. Protect your system with firewalls- The first and foremost requirement of the PCI DSS is to protect your system with firewalls. Ensuring proper configuration of firewalls shall ensure the protection of your card data environment.

2. Configure passwords and settings – Ensure you avoid keeping vendor-supplied passwords as your default password. Default passwords could pose a great threat to your system security.

3. Protect stored cardholder data- Protect and secure stored cardholder data and prevent a data breach. Card data stored in the system should be encrypted along with the encryption keys themselves being protected.

4. Encrypt transmission of cardholder data across networks- You need to use encryption and have security policies in place when you transmit cardholder data over open, public networks.

5. Use and regularly update an anti-virus software- Anti-virus software should be installed on all systems. Further, ensure anti-virus or anti-malware programs are updated regularly to detect known malware

6. Regularly update and patch systems- One should frequently release updates to patch security holes. This is very crucial to your security posture.

7. Restrict access to cardholder data- Access to cardholder data should be only provided to those who are appointed as an authorized person. this will secure data from being misused.

8. Assign a unique ID to each person with computer access- As a part of the security process, assigns a unique ID to every person who has access to computer access. This will ensure controlled access to sensitive data.

9. Restrict physical access to cardholder data- One should implement and strictly restrict physical access to cardholder data. This will prevent a data breach or misuse of data.

10. Implement logging and log management – Regularly review logs to identify errors, anomalies, and suspicious activities. You are also required to have a process in place to respond to these anomalies and exceptions. Use Security Information and Event Monitoring tools (SIEM), for monitoring systems regularly, oversee network activity, inspect system events, identify suspicious activity, inside your systems.

11. Conduct vulnerability scans and penetration tests- Conduct Vulnerability scans and pen test to detect unknow risks and threats. This should safeguard your system from any potential threats or risks.

12. Documentation and risk assessments- The final requirement for PCI compliance is to keep documentation, policies, procedures, and evidence relating to your company’s security practices in place for easy audit and remediation.