Downloaded 44 times

![PAYMENTS TRANSFORMATION WHITE PAPER

Payments Transformation white paper

3

In each case, the characteristics that drive or hamper delivery

reflect the degree to which the bank is able to look beyond “on-

time, on-budget” as indicators of the program’s success. To lay

the bedrock for effective realization of the targeted outcomes, the

bank should ensure three things:

1. Generate solid management buy-in for the transformation;

2. Empower the project team with the authority and “clout” to

drive the program through;

3. Maintain clear and sustained communication across and

beyond the program around goals, benefits and progress.

With these fundamentals in place, there are several steps that

will determine the ultimate success of the global payments

program. Experience and research highlight the overarching

importance of developing the right strategy and value proposition,

followed by rigorous management of the budget process and

process change, and a strong governance regime [see Figure 1].

We will examine all these factors in greater detail later in this

paper. But first, we will take a look at the current wider industry

trends in payments transformation.

Trends in Global Payments Transformation

The Drivers of Payments Transformation

Payments transformation is being driven by demand from banks’

own clients. Increasingly, bank customers of all types want access

to payments services and capabilities that are specifically tailored

to their own needs, yet delivered in a consistent and standardized

manner across all geographies.

Banks are responding to these requirements by seeking mass-

customizable systems—with differentiated fees and charges

being a key element—supported by automation and operational

standardization, and by productivity aids where full automation is

not possible.

This focus has triggered an accelerating transformation in banks’

payments operations in recent years, characterized by payments

globalization and convergence through the implementation of

payments hubs—a way to orchestrate end-to-end payment flows

through all the relevant areas of the bank. Since 2010, around

30 of the top 50 banks globally have engaged in payments

transformation programs in one form or another.

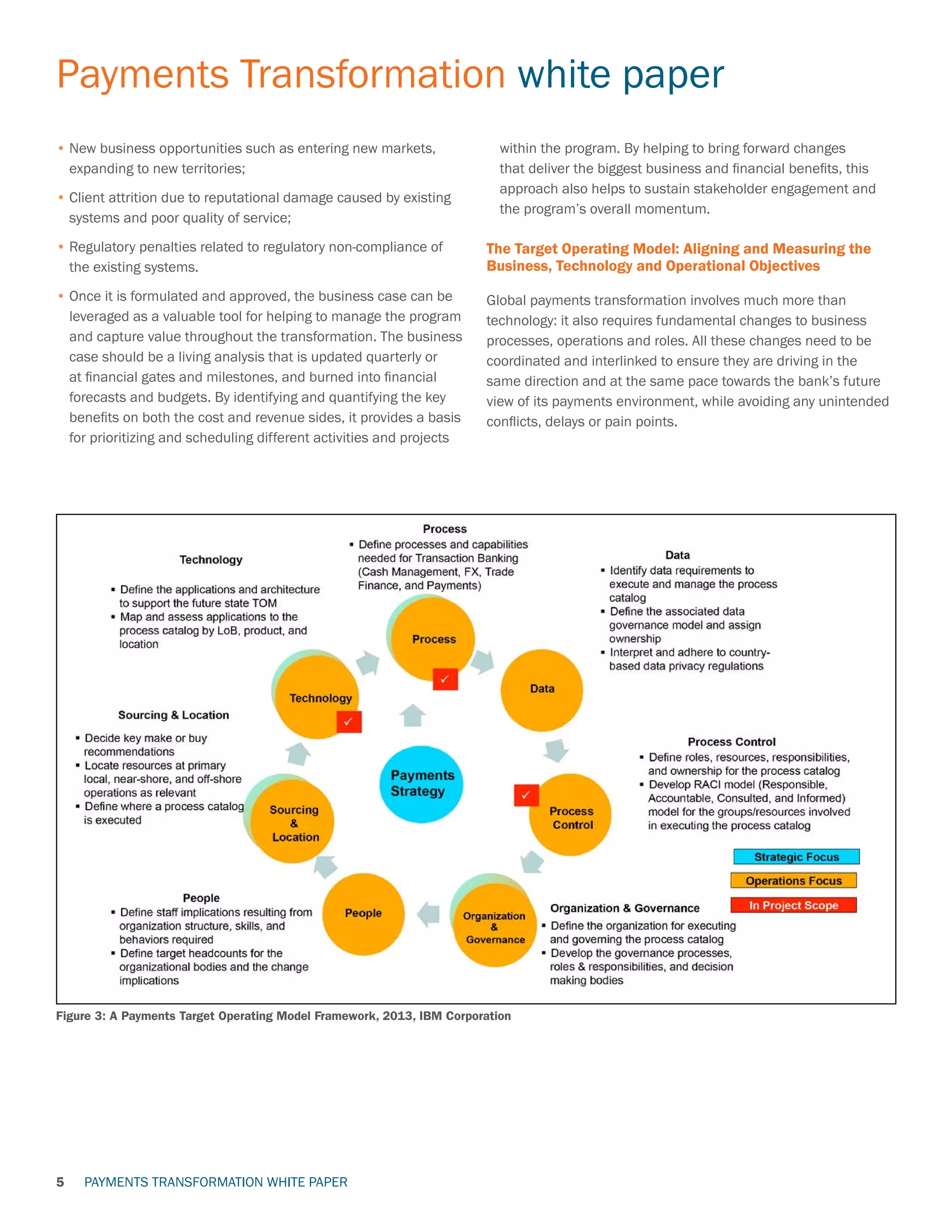

Figure 1: Experience Shows that Program Success Depends on a Wide Array of Factors, 2013, IBM Institute for Business Value Survey and Analysis](https://image.slidesharecdn.com/a88ad3b3-b890-4648-a0e9-8f3327d16dbb-150725070759-lva1-app6891/75/payments-transformation-global-payments-white-paper-4-2048.jpg)

This white paper provides guidance to banks on implementing a global payments system. It discusses trends driving banks to transform their payments operations through centralized payments hubs. The paper outlines the unique complexities of global payments transformations compared to other programs. Key success factors include generating management buy-in, empowering a project team, and clear communication. The paper provides guidance on developing the right strategy, managing budgets and processes, and establishing strong governance for successful transformation programs.

Overview of the payments transformation journey and its importance for banks globally.

Banks face pressures for efficiency and reliability in payments; adopting global payment systems is essential.

Banks are adopting payment hubs to meet competitive demands; 30 of the top 50 banks are involved in transformation efforts since 2010.

Importance of creating a robust business case; aligning business, technology, and operations for effective management.

Key stages in payments transformation execution, including analysis, design, verification, and deployment.

Support processes post-launch, including stakeholder management and enhancing knowledge through training.