Download as PDF, PPTX

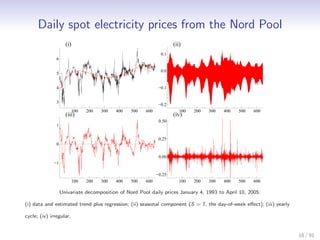

This document discusses time series forecasting and summarizes four illustrations of time series analysis and forecasting: 1. A multivariate model is used to analyze the European business cycle based on trends, common cycles, and leads/lags between economic indicators like GDP, industrial production, and confidence. 2. A bivariate unobserved components model is applied to daily Nordpool electricity spot prices and consumption data. The model decomposes the data into trends, seasons, cycles and residuals. Forecasting results show the bivariate model outperforms the univariate. 3. A periodic dynamic factor model is jointly modeled to 24 hours of French electricity load data. The model accounts for long-term trends, various seasonal patterns,

![Lecture on nk [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/lectureonnkcompatibilitymode-110825092241-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)