Downloaded 55 times

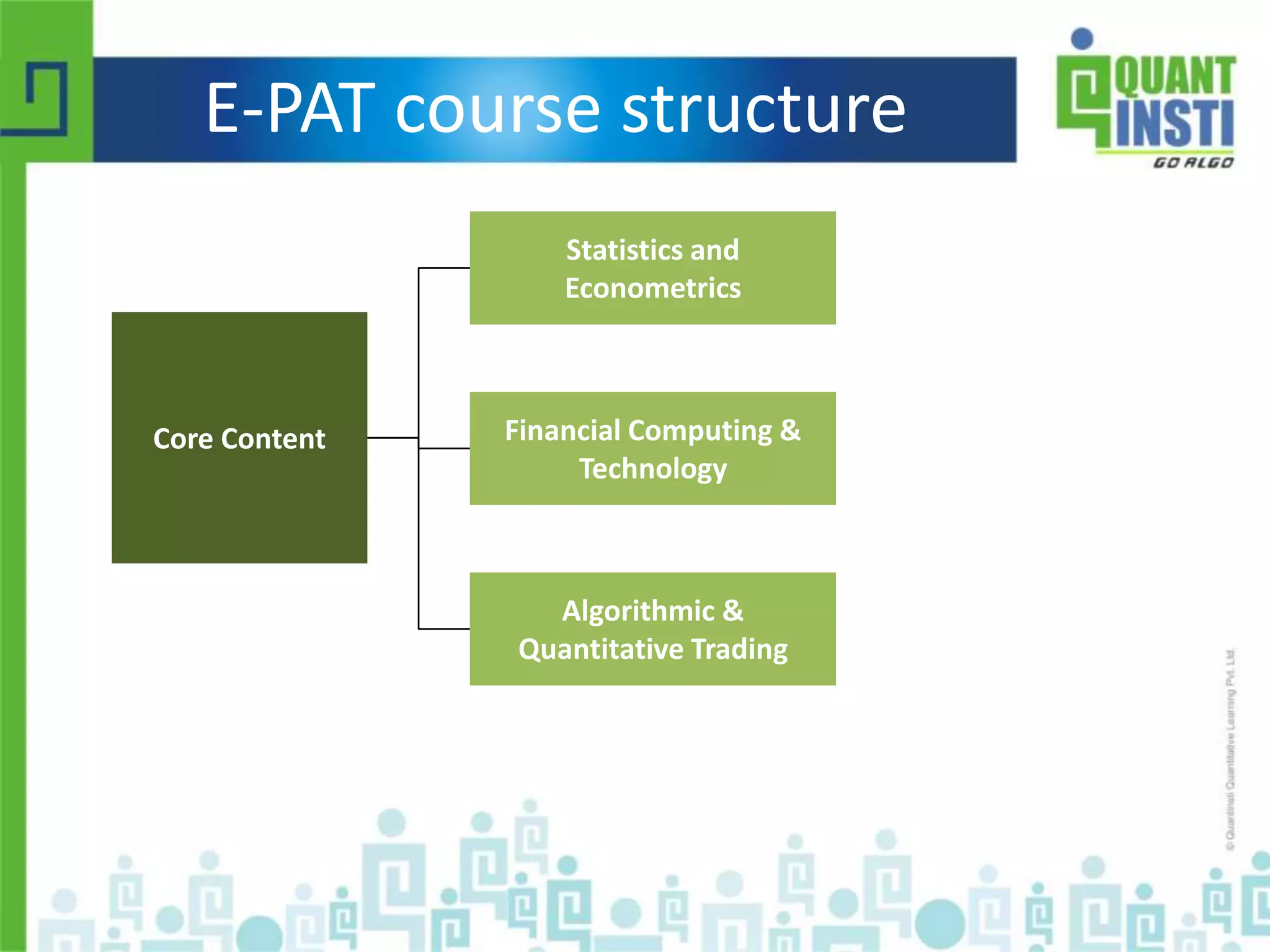

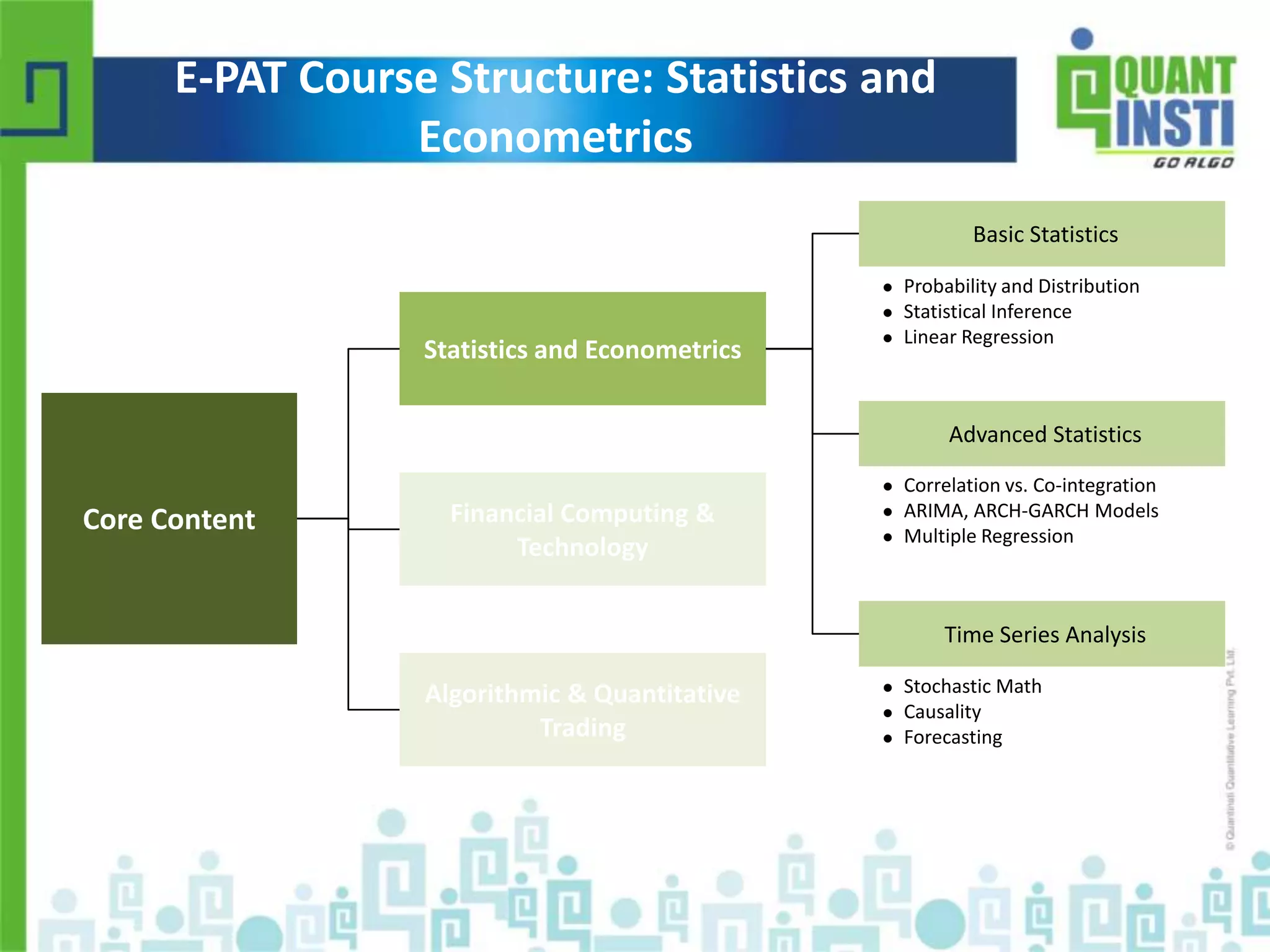

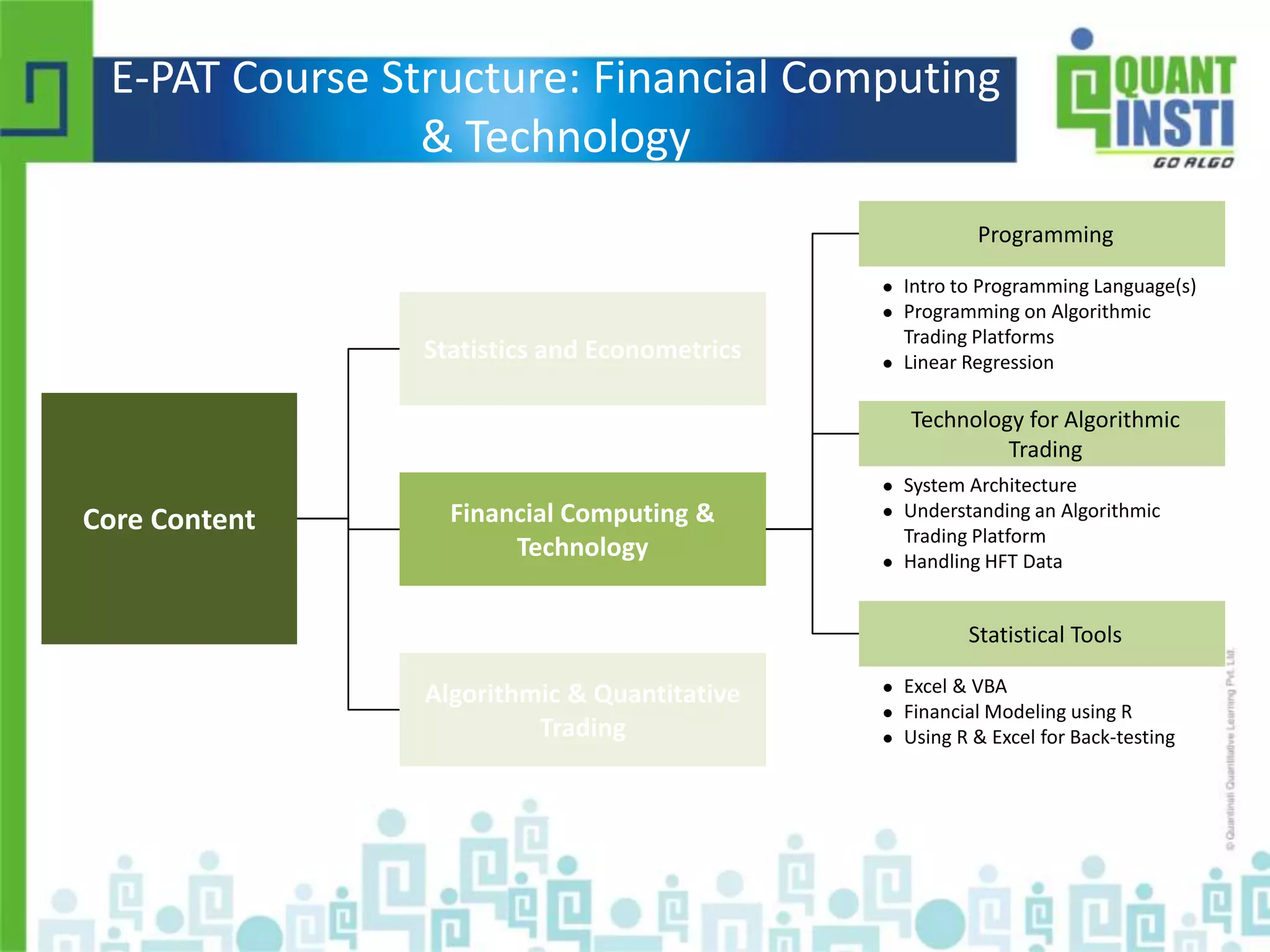

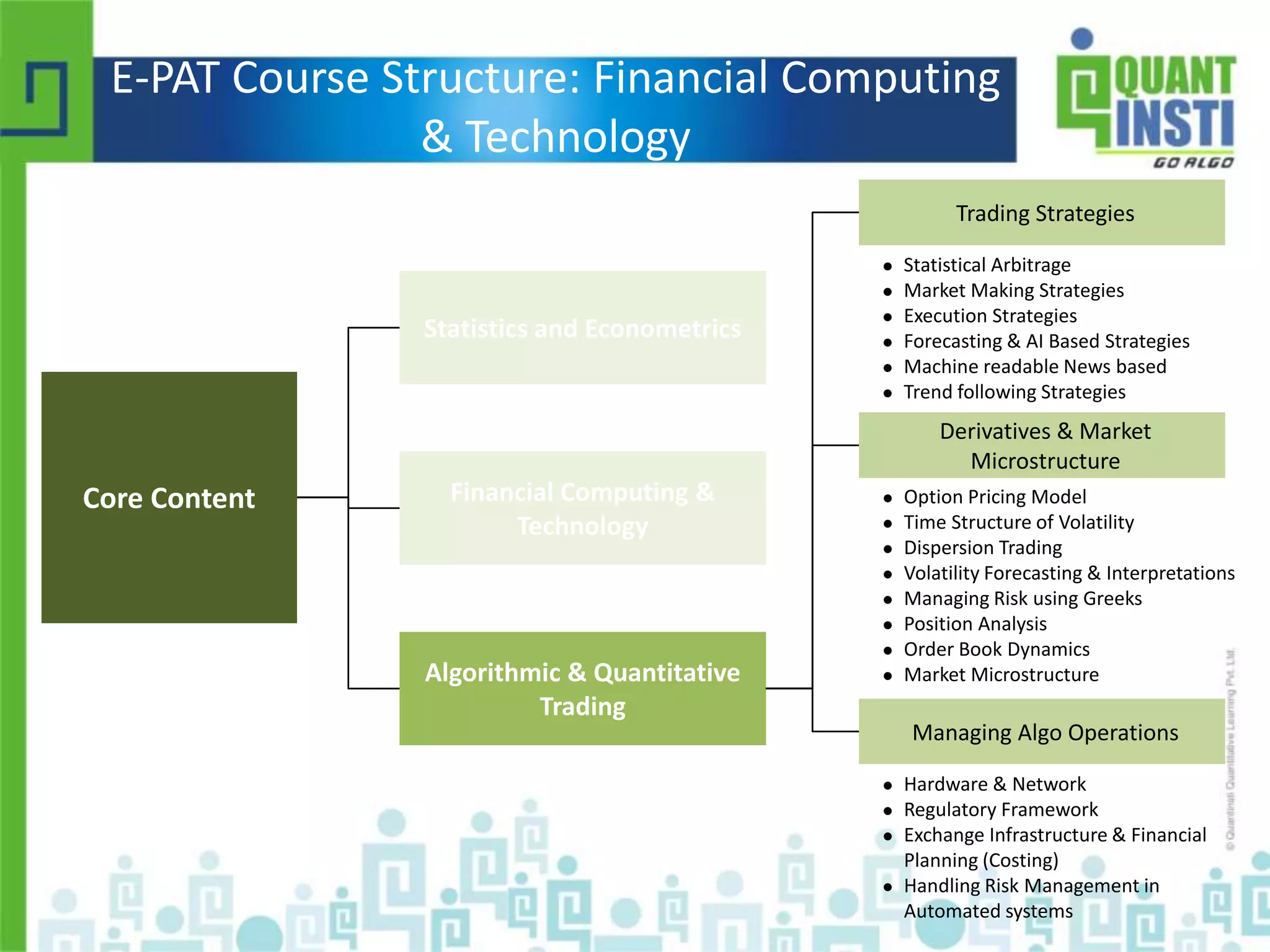

The document outlines the process of designing and implementing trading strategies, emphasizing the importance of hypothesis formulation, back-testing, and optimization. It discusses various trading strategies, the significance of risk assessment, and provides sample results for a trading strategy based on moving averages. Additionally, it offers details about a structured course on algorithmic and quantitative trading, including course content and delivery methods.

![[Data Meetup] Data Science in Finance - Building a Quant ML pipeline](https://cdn.slidesharecdn.com/ss_thumbnails/buildingaquantmlpipeline-191009091209-thumbnail.jpg?width=640&height=640&fit=bounds)