Download to read offline

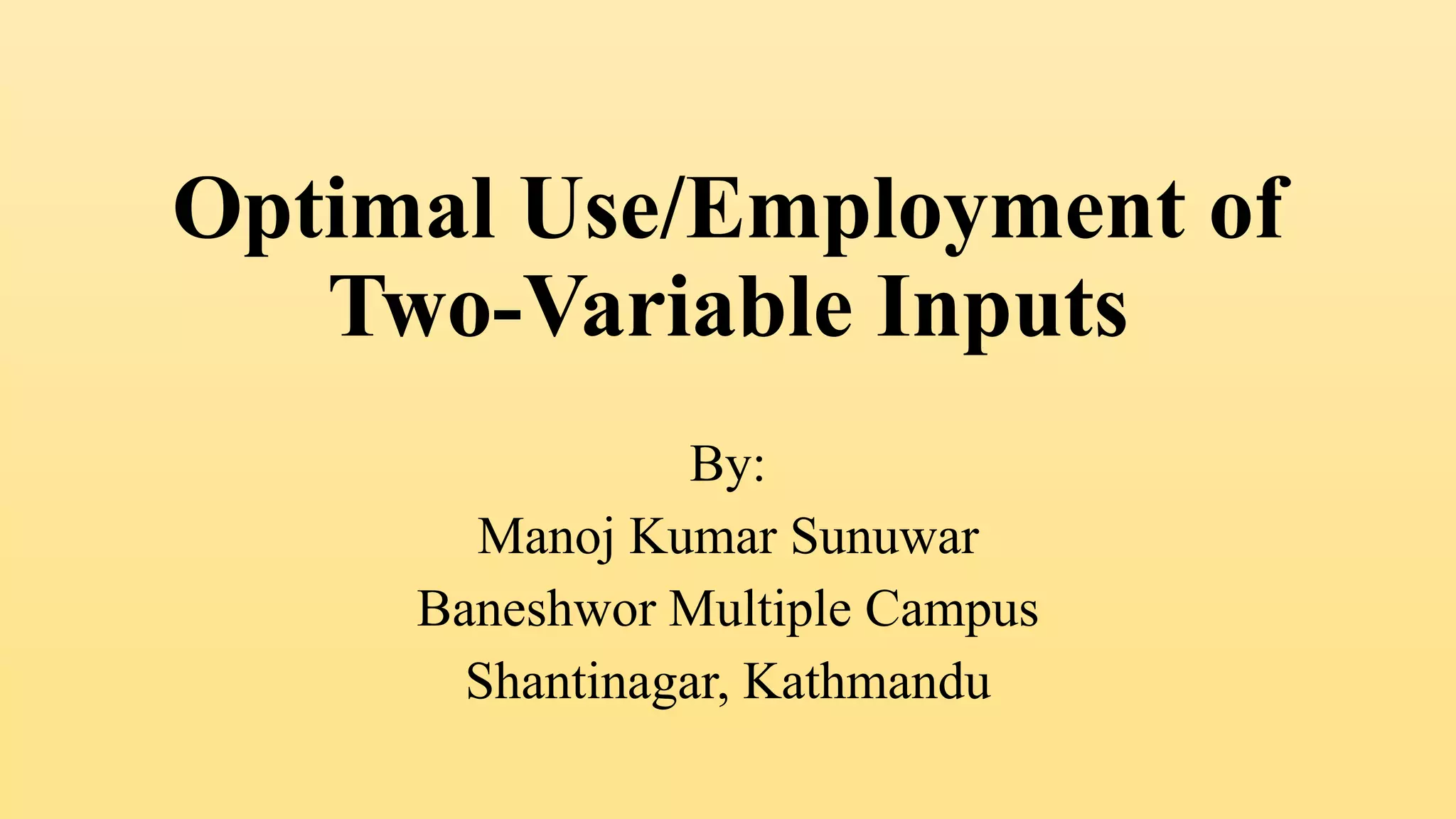

![Numerical Example

1. A company has the following production function,

Q = 100 K0.5 L0.5, w = $30 and r = $40.

a. Determine the expansion path. What does it exhibit?

b. Determine the efficient combination of inputs for producing 1444

units of output.

c. Determine the minimum cost of production.

d.What is the degree of returns this production function exhibits?

[T.U. 2017]

[Ans: (a) L= 4/3K (b) K = 12.5, L = 16.67 (c) $1000 (d) Constant returns

to scale]](https://image.slidesharecdn.com/optimaluseemploymentoftwovariableinputs-230724144636-4bcb0ccb/85/Optimal-Use-Employment-of-Two-Variable-Inputs-pptx-9-320.jpg)

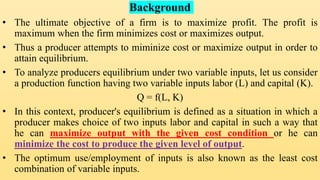

![Numerical Example

2. Let, the production function realized by the Noodle factory is Q = 100 KL, wage rate =

Rs. 50, rate of interest = Rs. 40, P= Rs. 2 per unit.

a. Compute the marginal productivities of two inputs.

b. (i) Show how to determine the amount of labor and capital the firm should use to

minimize the costs of producing 1118 units of output.

(ii) What is the profit and minimum cost?

(iii) What will be the minimum cost and optimal employment of labor and capital

at output 2236 units?

c. (i) What will be the optimal employment of labor and capital in order to maximize

output under a given total cost outlay of Rs.1,000?

(ii) What is the level of output and profit?

(iii) What will be the level of output and optimal employment of labor and capital

when the total cost outlay increases to Rs. 2,000? [T.U. 2016]

[Ans: (a) MPK = 50(L/K)0.5, MPL = 50(K/L)0.5 (b) i. K = 12.5, L = 10 ii. C = 1000, 𝝅 = 1236 iii. K = 25, L

= 20 (c) i. K = 12.5, L= 10 ii. Q=1118, 𝝅 = 1236 iii. K = 25, L=20]](https://image.slidesharecdn.com/optimaluseemploymentoftwovariableinputs-230724144636-4bcb0ccb/85/Optimal-Use-Employment-of-Two-Variable-Inputs-pptx-10-320.jpg)

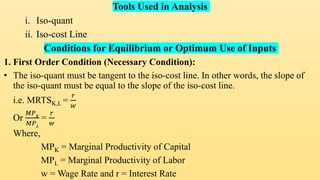

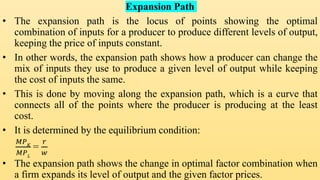

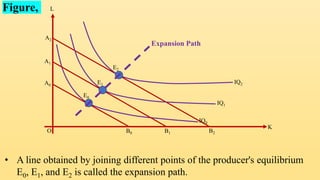

The document discusses the optimal use of two variable inputs, labor and capital, by a firm. It defines producer equilibrium as choosing input levels to maximize output for a given cost or minimize cost for a given output. The conditions for equilibrium are that: 1) The marginal rate of technical substitution equals the input price ratio. 2) The isoquant is convex to the origin at the point of tangency with the isocline. Optimal input combinations can be found by analyzing output maximization for a given cost or cost minimization for a given output. The expansion path shows the optimal inputs as output changes with fixed input prices. Numerical examples demonstrate finding the expansion path and optimal inputs for different output levels and cost constraints