Downloaded 1,200 times

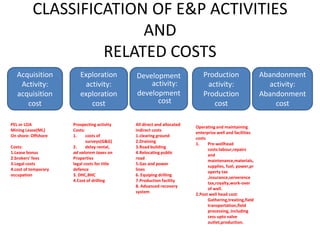

The document provides guidance on accounting for costs incurred on oil and gas exploration, development and production activities. It discusses two methods - successful efforts and full cost - for accounting for acquisition, exploration and development costs. Under successful efforts, unsuccessful exploration costs are charged to expense while under full cost, even unsuccessful costs are capitalized. The document also provides guidance on accounting for other costs like support equipment, abandonment costs, impairment of assets and interests in joint ventures. Extensive disclosures around reserves and costs are also required to be made as per the guidance.

![OVERVIEW OF THE OIL & GAS EXPLORATION AND [Autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/f980b2ed-b37b-4c91-b049-14cec3820fe3-150826222206-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![CU_2nd_lecture_24012024_Final_Version3[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/cu2ndlecture24012024finalversion31-240131154947-8ae77d7f-thumbnail.jpg?width=640&height=640&fit=bounds)