Download to read offline

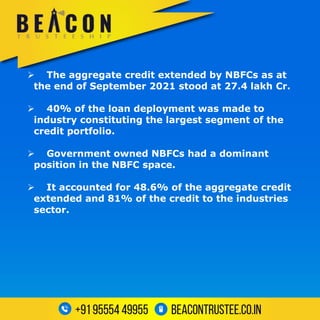

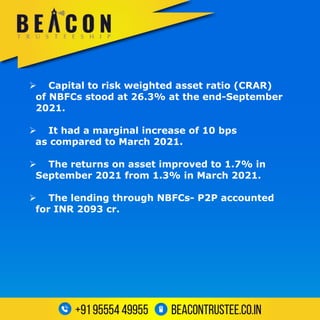

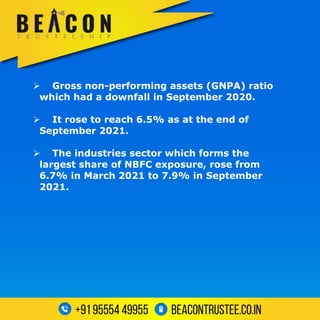

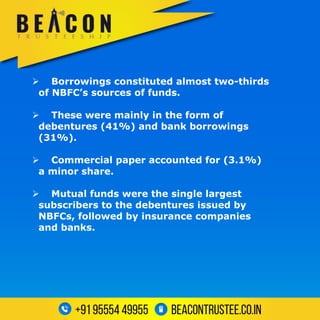

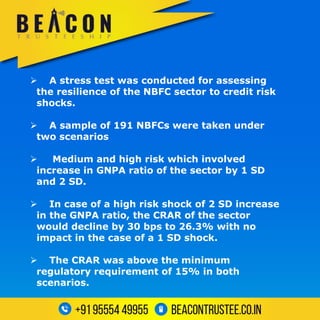

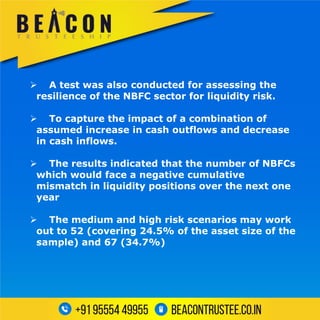

The document analyzes the recent performance of non-banking financial companies (NBFCs) in India as of September 2021. It finds that NBFCs extended a total of 27.4 lakh crore rupees in credit, with 40% going to industry. Government-owned NBFCs dominated the sector, accounting for 48.6% of total credit and 81% of credit to industry. Capital levels remained healthy, with the capital to risk-weighted asset ratio at 26.3%, though gross non-performing assets rose to 6.5% overall and 7.9% for industry loans. Stress tests found the sector remained resilient to credit and liquidity risks under medium and high shock scenarios.