MyTownCryer Mid Year 2010 Analysis

•

0 likes•292 views

1. Foreclosures have declined for almost three years after peaking in 2008. However, short sales continue to be common as lenders work with borrowers. The short sale cycle may continue for 2-5 more years before a normal market trend returns. 2. The ratio of home listings to sales indicates the market may drift into oversupply in the second half of 2010 if current trends continue, potentially leading to more foreclosures and short sales. 3. While average home prices have increased in the first half of 2010, particularly for higher-end homes, prices have actually declined in many individual areas. Average prices should only be used as a general guide, not to assess specific markets or properties.

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Similar to MyTownCryer Mid Year 2010 Analysis

Similar to MyTownCryer Mid Year 2010 Analysis (20)

More from Tom Cryer

More from Tom Cryer (20)

MyTownCryer Mid Year 2010 Analysis

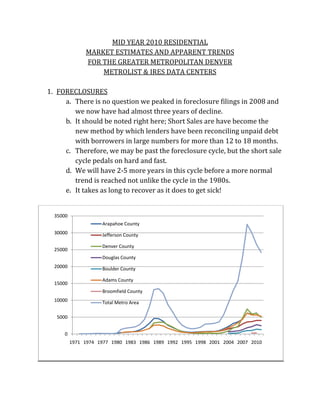

- 1. MID YEAR 2010 RESIDENTIAL MARKET ESTIMATES AND APPARENT TRENDS FOR THE GREATER METROPOLITAN DENVER METROLIST & IRES DATA CENTERS 1. FORECLOSURES a. There is no question we peaked in foreclosure filings in 2008 and we now have had almost three years of decline. b. It should be noted right here; Short Sales are have become the new method by which lenders have been reconciling unpaid debt with borrowers in large numbers for more than 12 to 18 months. c. Therefore, we may be past the foreclosure cycle, but the short sale cycle pedals on hard and fast. d. We will have 2‐5 more years in this cycle before a more normal trend is reached not unlike the cycle in the 1980s. e. It takes as long to recover as it does to get sick! 35000 Arapahoe County 30000 Jefferson County Denver County 25000 Douglas County 20000 Boulder County Adams County 15000 Broomfield County 10000 Total Metro Area 5000 0 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

- 2. 2. SALES TO LISTING RATIOS a. The ratio of sales to listings has been of paramount importance to predicting the health of a market for many years. b. What we are seeing right now is an estimated trend of rapidly increasing supply and the absorption from sales activity remaining constant. c. This is creating a trend or movement toward over supply. d. If the second half of 2010 were to continue on this same trend line as the first six months, we will drift into an oversupply market creating more foreclosure and short sale potential. Ratio of Listings to Sales 4.00 3.00 Ratio 2.00 1.00 0.00 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 Date 3. AVERAGE PRICE TRENDS a. Average price trends should only be considered as a guide to market conditions and not an absolute for all properties in a given market place. b. In the first half of 2010, we have seen average prices inch up. c. They have increased significantly in areas that have higher end inventory, because we have seen increased activity there due to the new price paradigm which is often 20, 30, 40 and even 50% of 2007 values. d. This elevates the average price particularly if there is less activity at the lower end of the market as we have seen since the Tax Credits were eliminated from this equation. e. Overall, average prices are up, but in many individual MLS areas, prices have actually declined. f. Remember, each and every enclave, community or neighborhood needs to be addressed for their own individual price trend. Average prices can only be used as a guide, and then and only

- 3. then can they assist with computing the health of a residential market area. History of Average Residential Prices in Denver Metro Area $700,000 $600,000 ALL AREAS $500,000 DSE $400,000 SSE Price $300,000 DEC/DHR/DHL $200,000 $100,000 $0 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 Date 4. MARKET SHARE BY PRICE RANGE & SUPPLY OF INVENTORY a. There is much to learn from this next chart. It can tell us the story about the health of the market. b. Is the market growing in the higher priced market segment or is it growing at the bottom of the price ladder? c. Here’s what we know. In the last 6 months, there has been considerable growth in the middle of the market from $200K to $750K. d. This makes sense since we literally ran out of inventory under $200K due to the tax credits, the $200‐400K price segment grew by almost 2% in just 6 months. e. We know from NAR data that each entry level transaction creates an upward movement of parties to the market place hopefully displacing residents along the way until there have been 6 more transactions. (Keep in mind, many of the bank owned properties were vacant at the time of sale a less “friction” in the market place resulted.) f. We know the higher the price the greater the months’ supply of inventory. This has historically been a result of greater builder margins therefore more supply was created at this end of the market, but with virtually no new construction in the market at

- 4. this time, this suggests significant weakness for price improvement in this segment moving forward. MONTHS SUPPLY 40 35 30 25 20 15 10 MONTHS SUPPLY 5 0 g. Additionally, we know, the higher the price the smaller the market share in terms of the number of transactions. This trend has never changed as long as this chart has been compiled. % MKT SHARE 120.00% 100.00% 80.00% 60.00% 40.00% % MKT SHARE 20.00% 0.00% 5. IN CLOSING a. There are always competing ways to read the data and present the data in any report.

- 5. b. The data in this analysis has been presented in this fashion since 1975. c. The result has been a relatively accurate method of predicting future trends in this market place. d. Everything points toward more of the same. i. Uncertainty ii. Price sensitivity iii. Inventory teetering on the tipping point of dangerous oversupply iv. External factors affecting consumer sentiment which affects home buying confidence v. The cost of borrowing vi. The cost of energy vii. Residential taxes e. As a result, we can’t bet on price appreciation to “bail out” the price depressed residential market any time soon. f. It’s going to take some time to heal all these wounds. All data obtained, compiled and edited from Metrolist, Inc. which compiles their data from individual Realtor sources. This report was completed by Tom Cryer, SCRP Broker Associate with The Kentwood Company. Information obtained from sources believed to be reliable but not guaranteed.

- 6. FORECLOSURES BY COUNTY AND METRO DENVER AREA TOTAL MID YEAR 2010 (ESTIMATED) 35000 Arapahoe County 30000 Jefferson County Denver County 25000 Douglas County 20000 Boulder County Adams County 15000 Broomfield County 10000 Total Metro Area 5000 0 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

- 7. Total # of Listings and Sales at Mid Year 2010 Denver MLS System YEAR LISTINGS SALES RATIO Total Count Total Count 12/31/75 35,728 19,156 1.87 Potential negative market signal (Above 2.50) 12/31/76 40,223 24,354 1.65 Potential positive market signal (Below 2.00) 12/31/77 41,598 29,875 1.39 Potential neutral market signal (Between 2.00 & 2.50) 12/31/78 49,675 31,213 1.59 Too soon to tell // Year to date // Inconclusive 12/31/79 59,384 31,024 1.91 Indicates all time high or low 12/31/80 55,438 23,952 2.31 12/31/81 49,755 22,125 2.25 12/31/82 52,817 18,756 2.82 12/31/83 63,585 23,566 2.70 12/31/84 69,041 23,264 2.97 12/31/85 73,279 24,489 2.99 12/31/86 75,694 25,865 2.93 12/31/87 69,740 23,414 2.98 12/31/88 62,521 24,120 2.59 12/31/89 50,112 25,142 1.99 12/31/90 53,682 26,436 2.03 12/31/91 53,286 27,375 1.95 12/31/92 48,103 34,828 1.38 12/31/93 69,118 40,291 1.72 12/31/94 73,637 40,068 1.84 12/31/95 78,969 37,767 2.09 12/31/96 84,909 39,849 2.13 12/31/97 90,813 41,959 2.16 12/31/98 103,402 47,836 2.16 12/31/99 72,842 48,795 1.49 12/31/00 100,672 50,499 1.99 12/31/01 133,688 49,372 2.71 12/27/02 138,445 49,326 2.81 12/29/03 123,596 47,731 2.59 12/31/04 127,989 53,710 2.38 12/31/05 135,008 54,072 2.50 12/31/06 152,807 52,220 2.93 12/31/07 143,400 51,304 2.80 12/31/08 123,655 48,926 2.53 12/31/09 104,330 48,926 2.13 12/31/10 125,954 42,892 2.94 MID YEAR 7/1/2008 (EST) LISTINGS SALES RATIO Res 92,894 33,012 2.81 Cond 26,772 8,968 2.99 Land 4,134 452 9.15 Inc 2,154 460 4.68 Totals 125,954 42,892 2.94 Ratio of Listings to Sales 4.00 3.00 Ratio 2.00 1.00 0.00 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 Date Information obtained from sources believed to be reliable but not guaranteed. All data obtained from year to date statistics provided by Metrolist, Inc. and compiled by Tom Cryer, SCRP Broker Associate with The Kentwood Company

- 8. MID YEAR 2010 AVERAGE RESIDENTIAL PRICES IN THE DENVER METROLIST SYSTEM YEAR ALL AREAS DSE SSE DEC/DHR/DHL 1974 $34,722 $36,668 $50,912 $36,291 1975 $35,921 $36,381 $52,938 $59,250 1976 $39,740 $43,195 $61,135 $60,925 1977 $44,876 $50,825 $67,072 $64,473 1978 $55,610 $64,650 $83,446 $77,178 1979 $66,051 $77,648 $96,058 $80,129 1980 $78,594 $97,128 $127,856 $94,337 1981 $83,893 $98,263 $149,426 $101,684 1982 $87,816 $105,454 $161,047 $108,409 1983 $90,346 $109,035 $169,407 $113,755 1984 $95,137 $112,423 $167,934 $132,430 1985 $95,447 $112,415 $160,672 $119,942 1986 $97,049 $113,650 $170,716 $137,264 1987 $102,773 $116,006 $171,634 $137,204 1988 $98,937 $114,095 $171,848 $127,303 1989 $103,868 $117,491 $173,571 $133,061 1990 $102,848 $120,200 $194,900 $151,544 1991 $109,071 $120,485 $207,658 $146,456 1992 $115,154 $127,078 $212,173 $154,699 1993 $126,168 $140,513 $251,099 $164,913 1994 $138,301 $156,144 $278,046 $184,909 1995 $150,736 $172,185 $292,631 $192,643 1996 $159,328 $185,406 $315,670 $193,398 1997 $169,587 $201,601 $315,143 $205,132 1998 $185,785 $226,862 $358,542 $211,589 1999 $208,296 $259,311 $433,756 $231,368 2000 $257,394 $325,126 $492,378 $305,952 2001 $239,779 $301,211 $506,959 $277,089 2002 $268 926 $268,926 $348 850 $348,850 $507 371 $507,371 $315 375 $315,375 2003 $279,279 $365,652 $497,179 $315,402 2004 $290,876 $387,094 $527,605 $342,193 2005 $309,047 $426,258 $602,644 $355,242 2006 $317,112 $468,266 $589,911 $361,927 2007 $310,418 $486,515 $595,345 $372,880 2008 $270,261 $461,630 $529,667 $362,328 2009 $241,876 $435,726 $490,787 $358,684 2010 $252,041 $425,402 $485,992 $359,179 Mid Year History of Average Residential Prices in Denver Metro Area $700,000 $600,000 ALL AREAS $500,000 DSE $400,000 SSE Price $300,000 DEC/DHR/DHL $200,000 $100,000 $0 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 Date Information obtained from sources believed to be reliable but not guaranteed. All data obtained from Metrolist, Inc. and compiled by Tom Cryer, SCRP Broker Associate with The Kentwood Company.

- 9. DENVER METRO SINGLE FAMILY MARKET SHARE BY PRICE RANGE AS OF MID YEAR 2010** **Annualized LISTING RANGES ACTIVE LISTINGS UNDER CONTRACT SALES % MKT SHARE ALL PRICES 24,731 5,288 41,174 100.00% $0‐200K 6,175 2,327 16,227 39.41% $200‐400K 10,670 2,091 18,679 45.37% $400‐750K 5,249 741 5,440 13.21% $750K‐1M 1306 105 689 1.67% $1M + 1,639 89 533 1.29% 100.96% SUPPLY IN MONTHS OF SFR INVENTORY LISTING RANGES TOTAL # SALES MONTHS SUPPLY ALL PRICES 41,174 7.21 $0‐200K 16227 4.57 $200‐400K 18679 6.85 $400‐750K 5440 11.58 $750K‐1M 689 22.75 $1M + 533 36.90