Downloaded 337 times

![AL-QURAN

Believers, fear Allah and give up

what is still due to you from usury, if

you are believers;

[SURAH AL-BAQARAH AYAH 278]](https://image.slidesharecdn.com/mudarbaha-140607044026-phpapp01/75/Mudarbaha-ppt-6-2048.jpg)

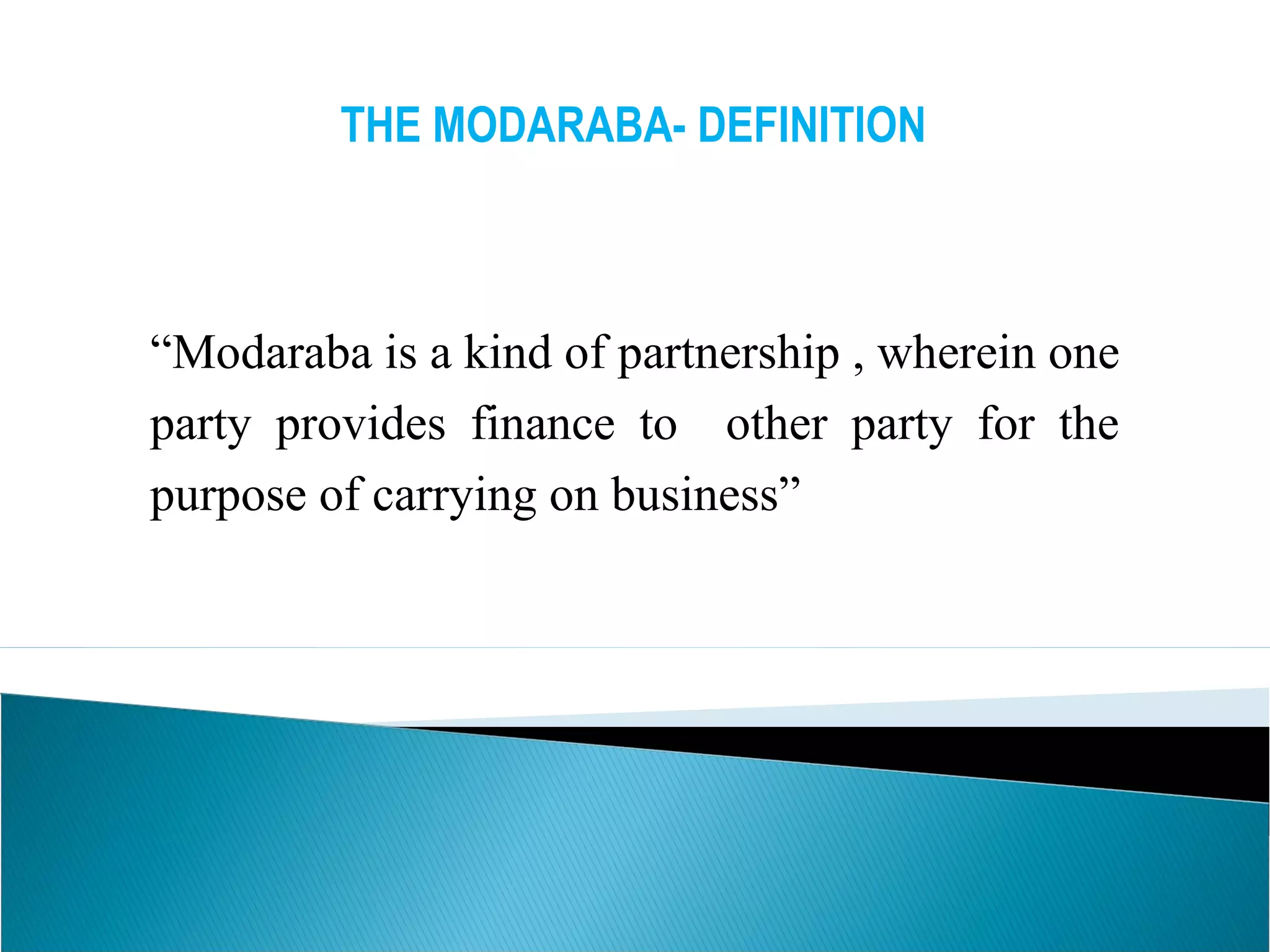

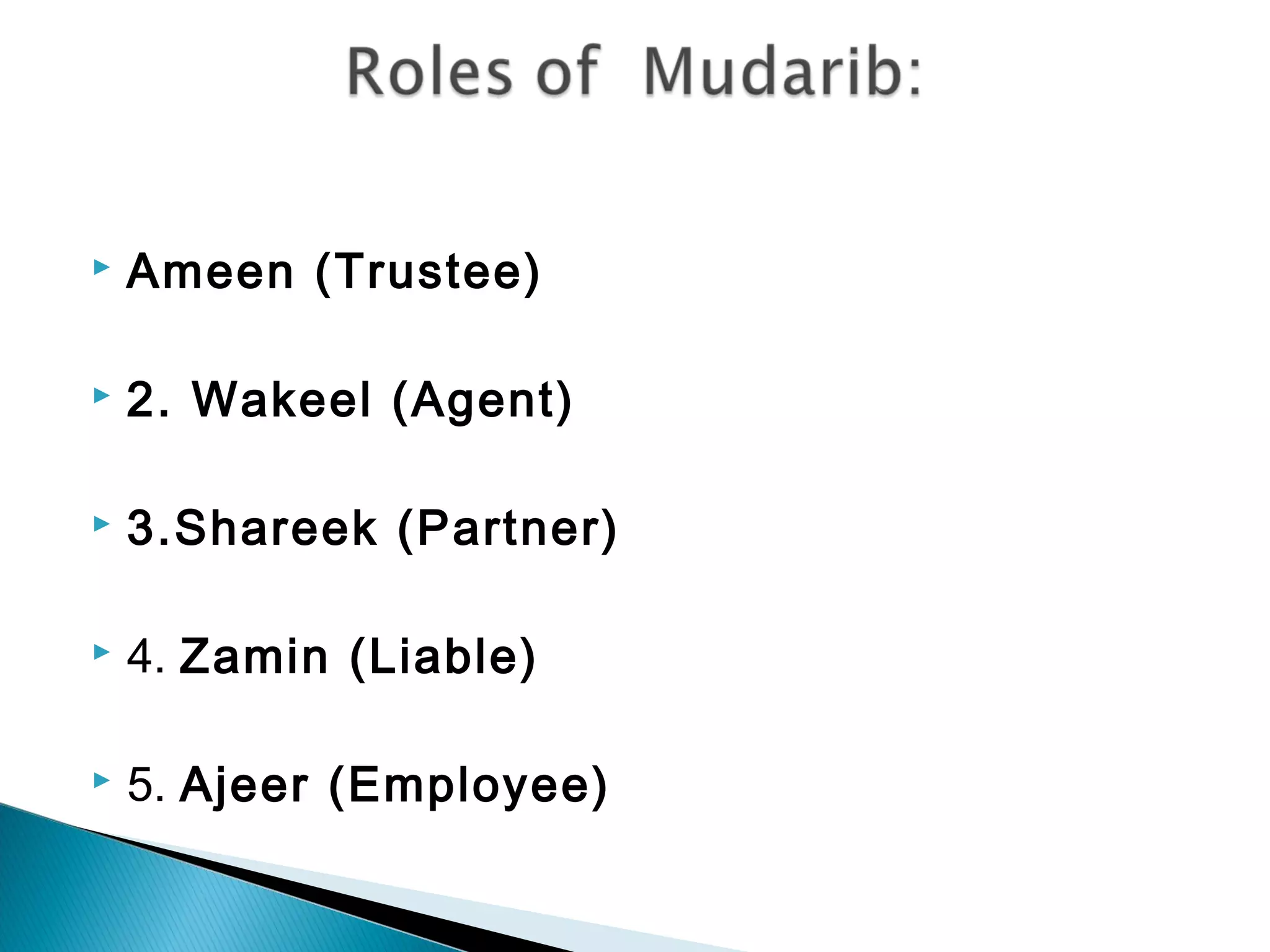

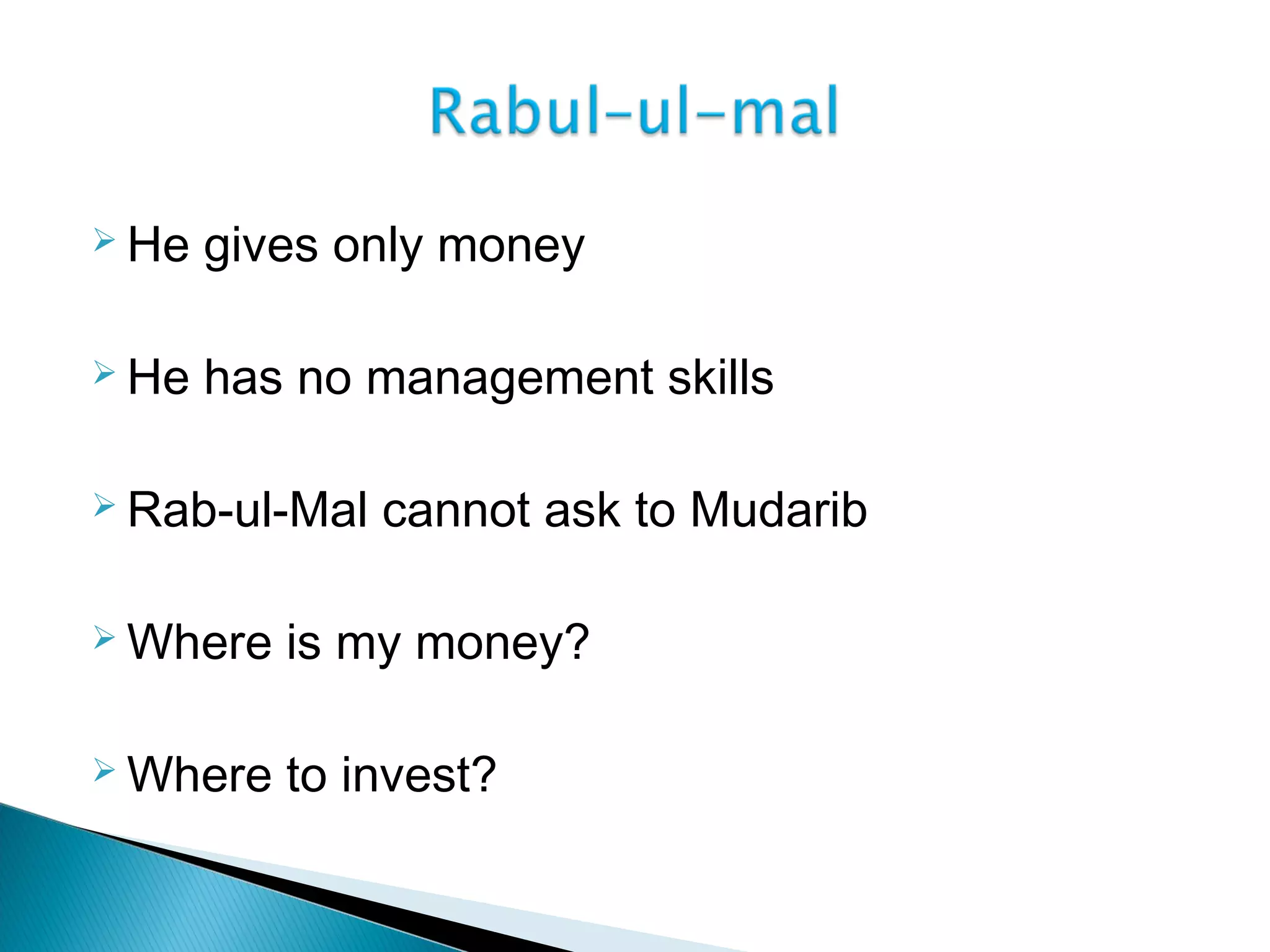

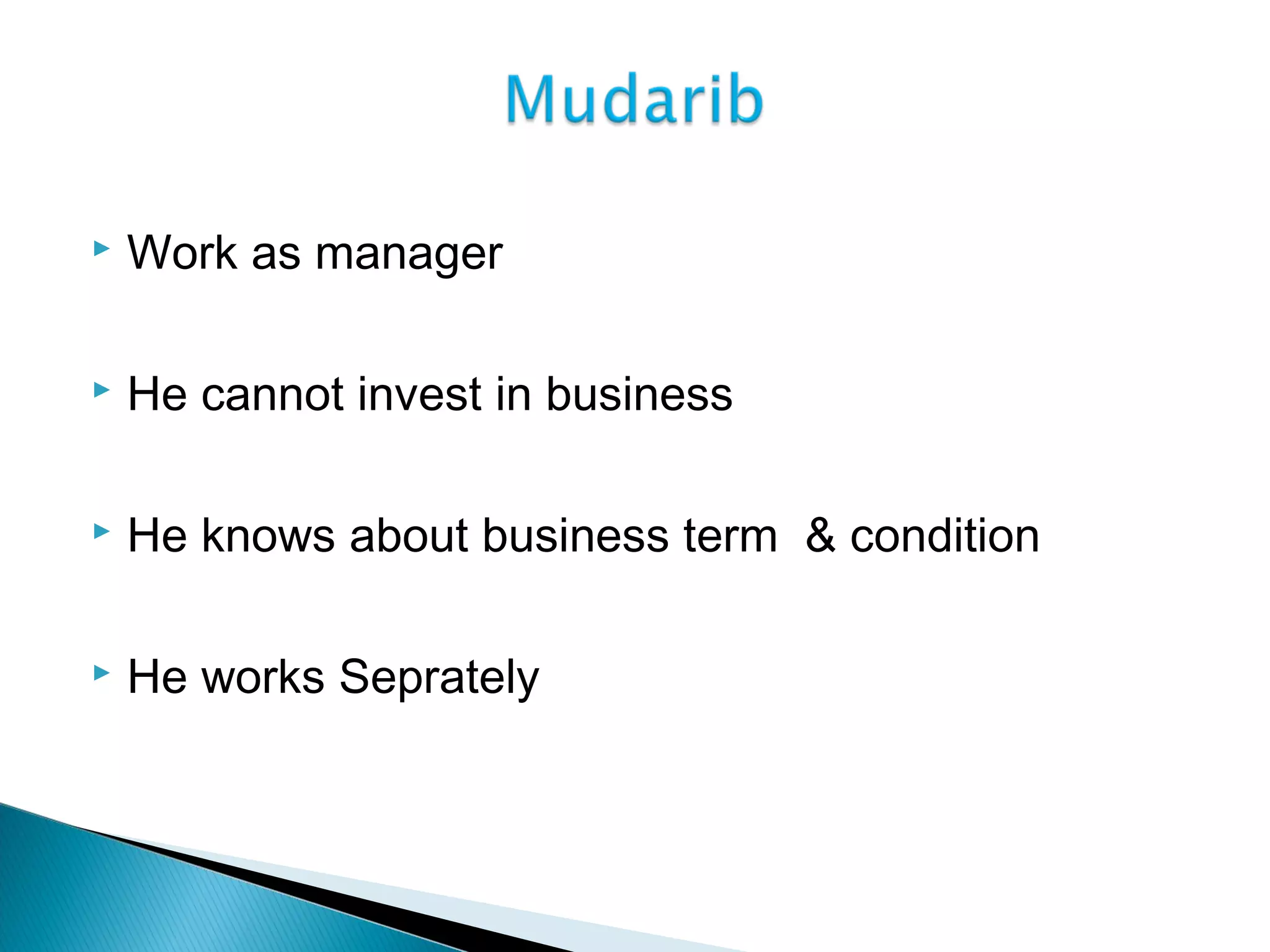

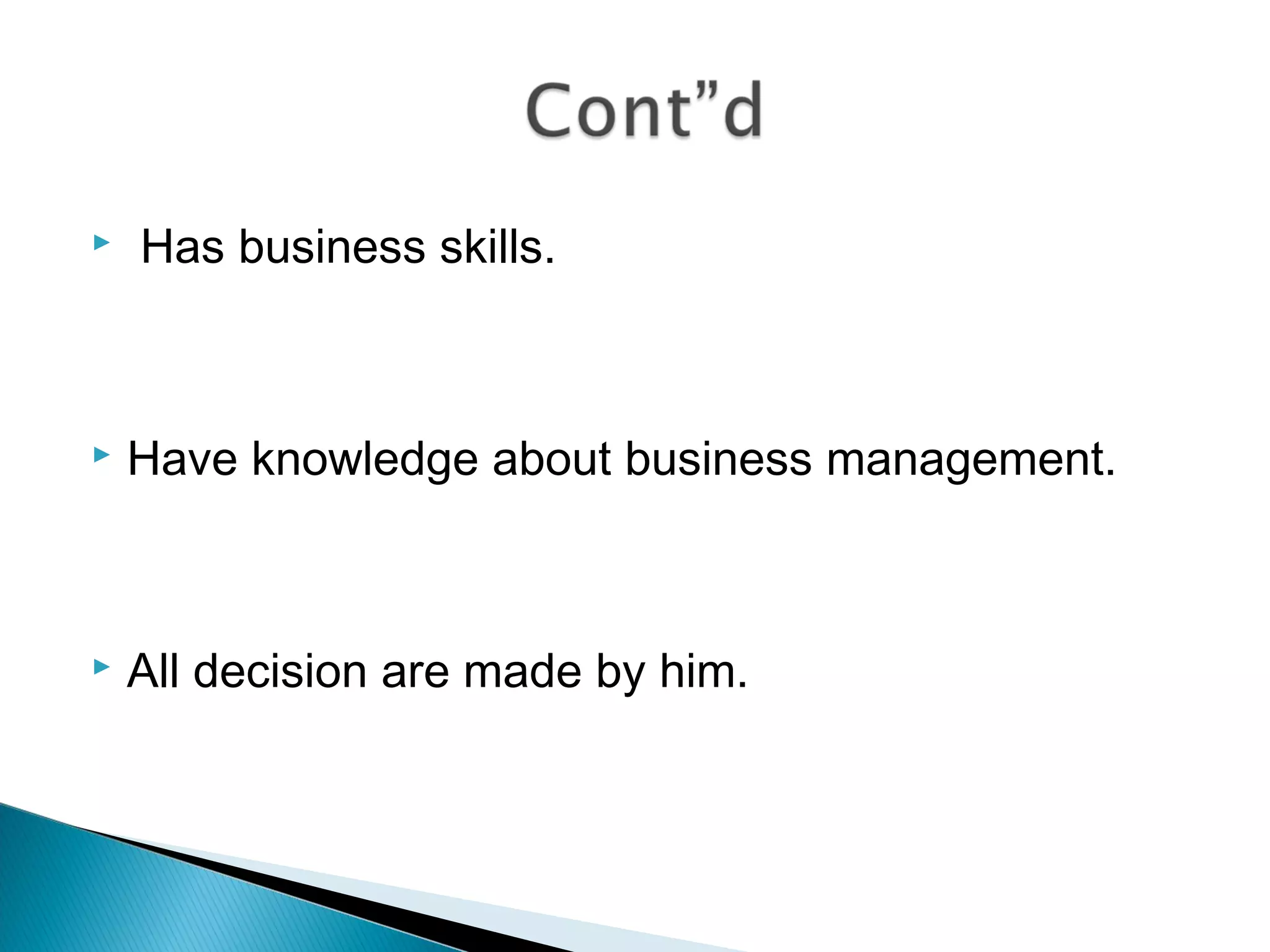

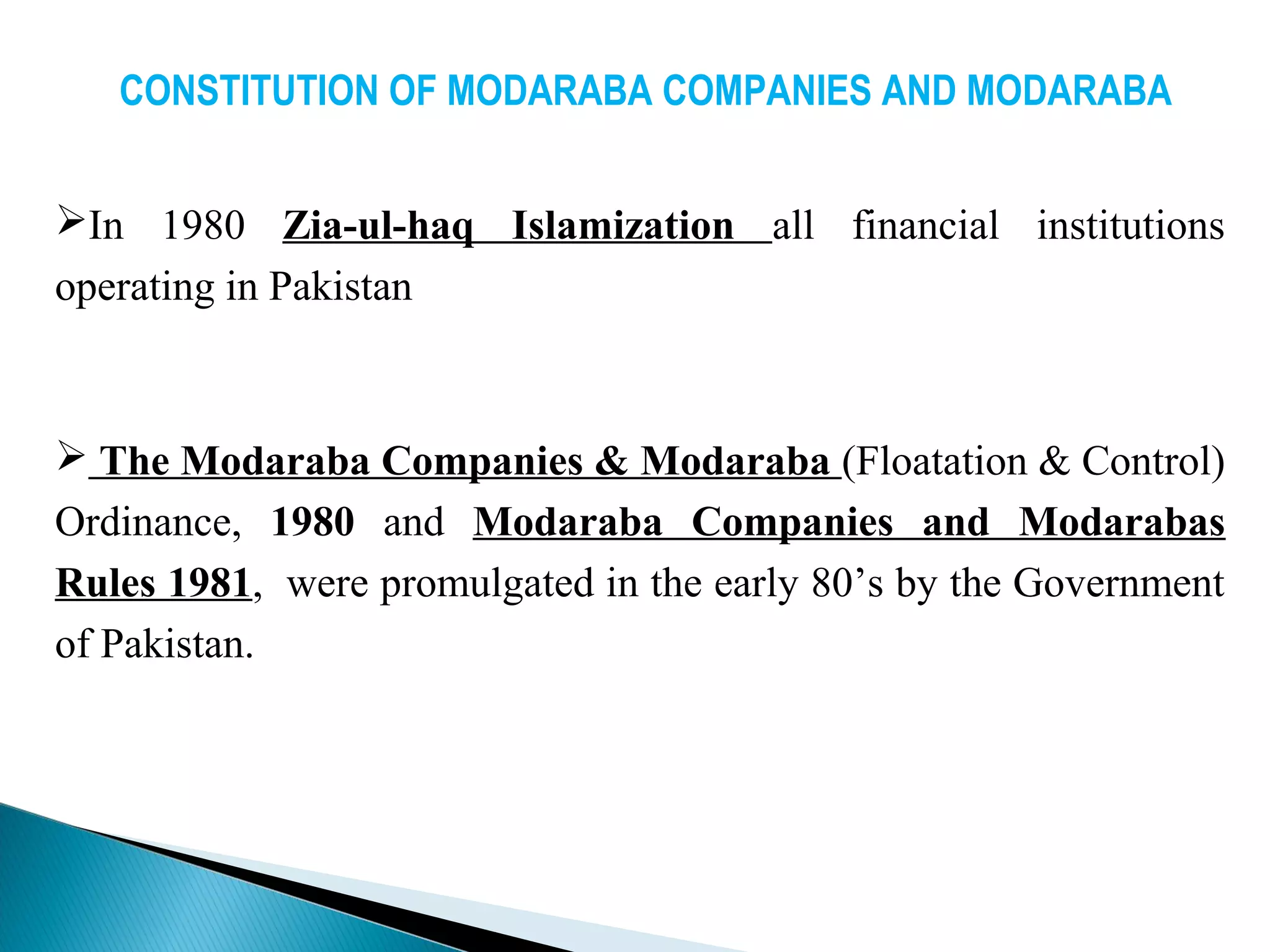

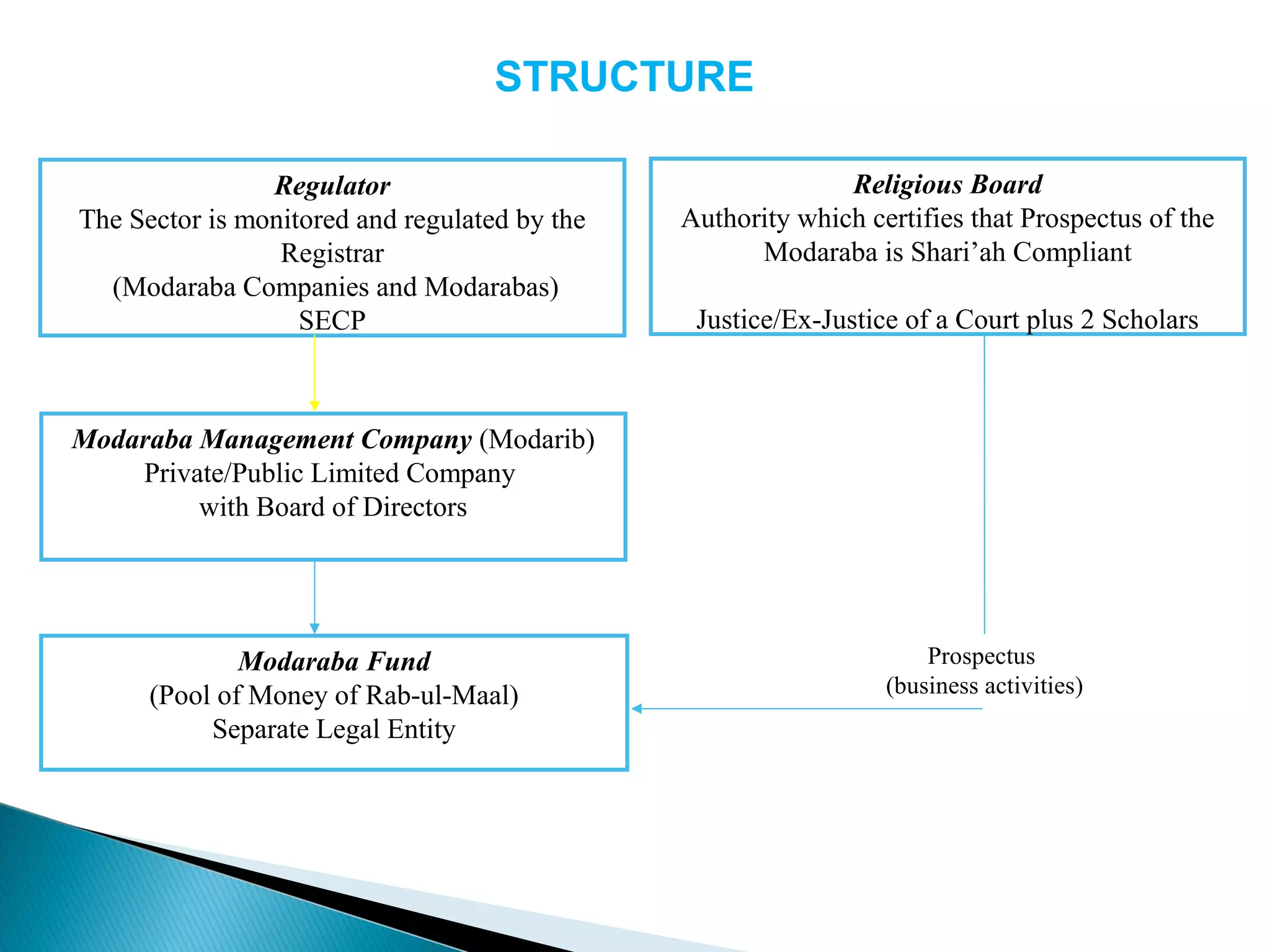

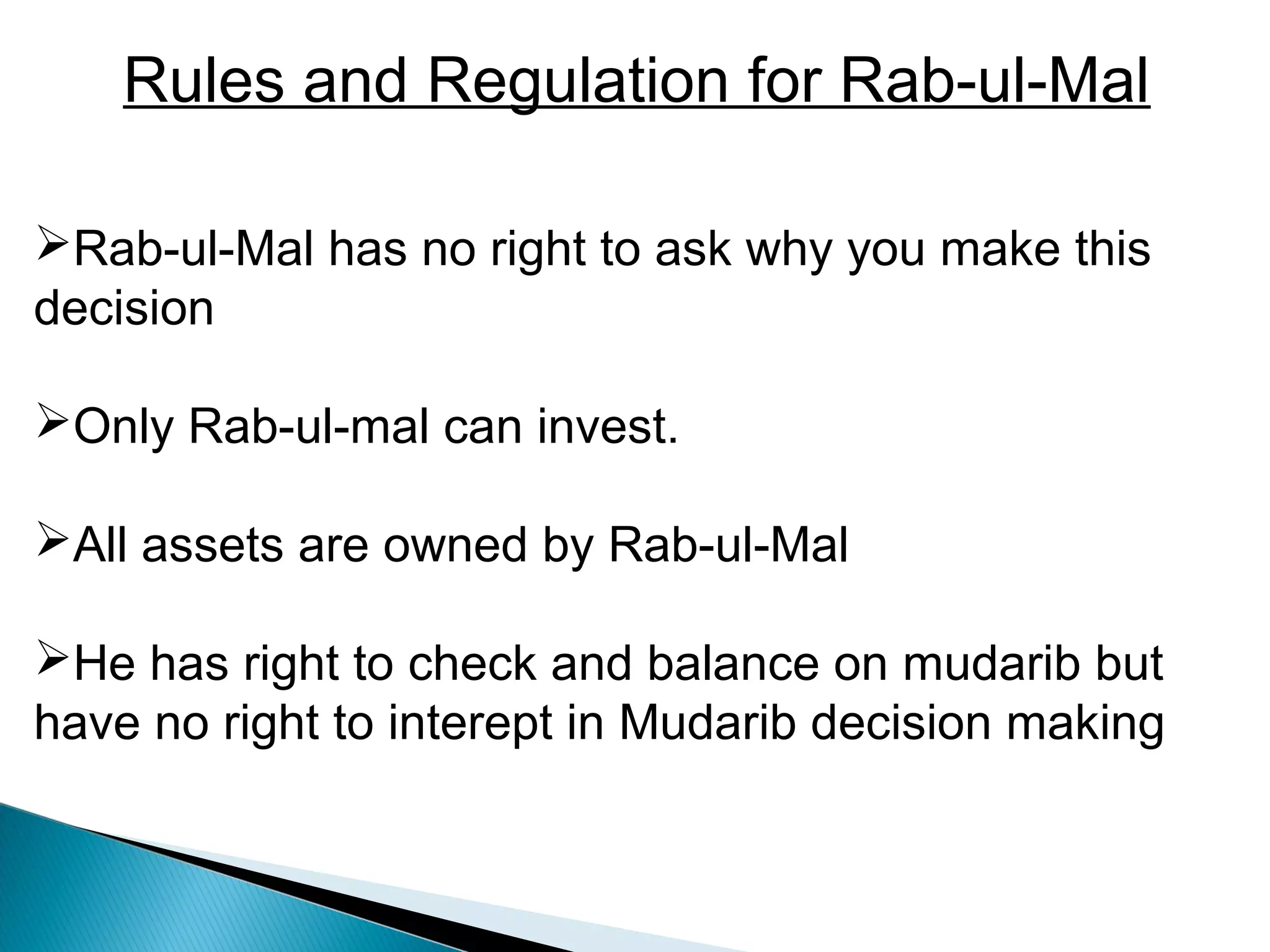

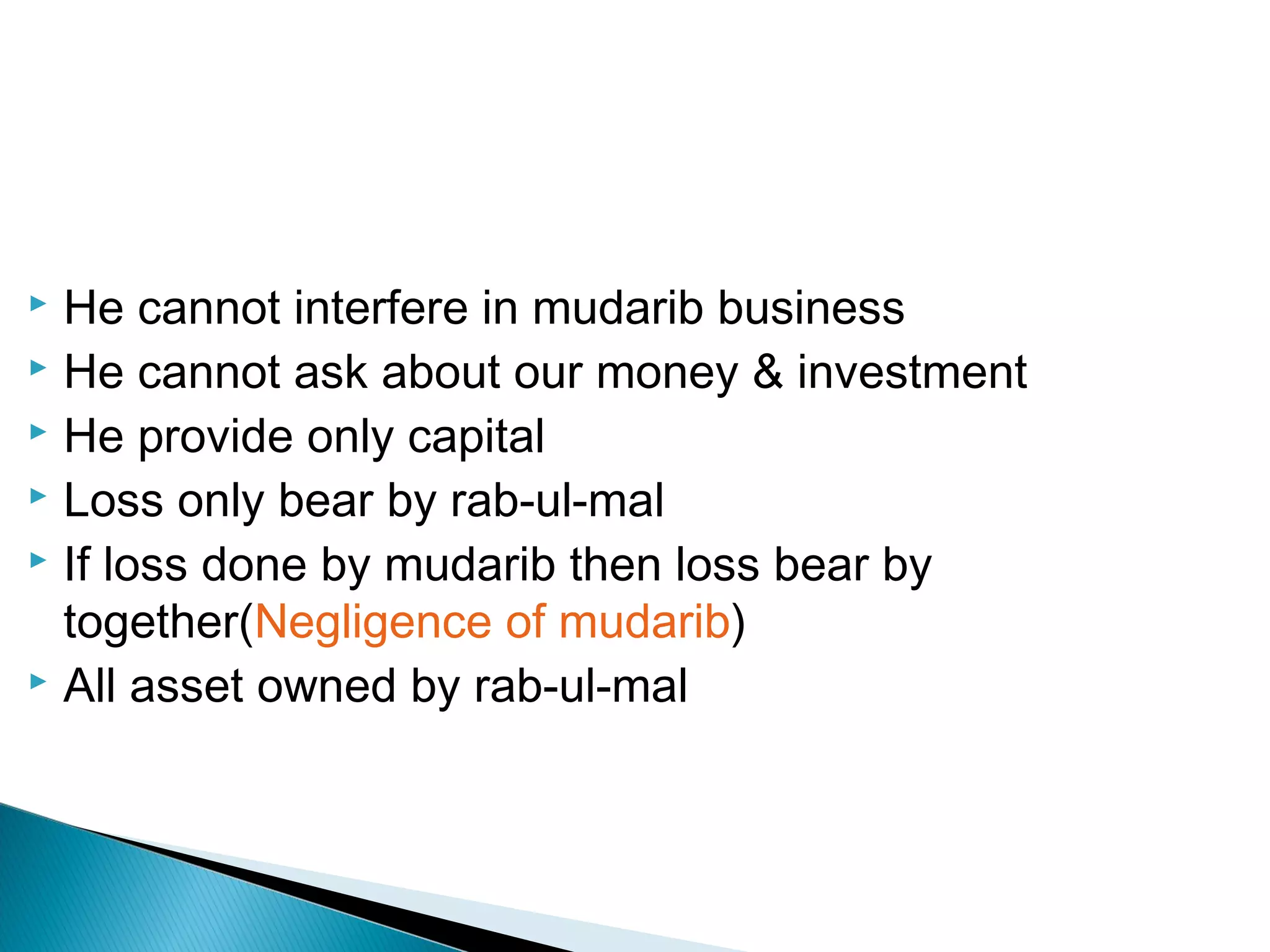

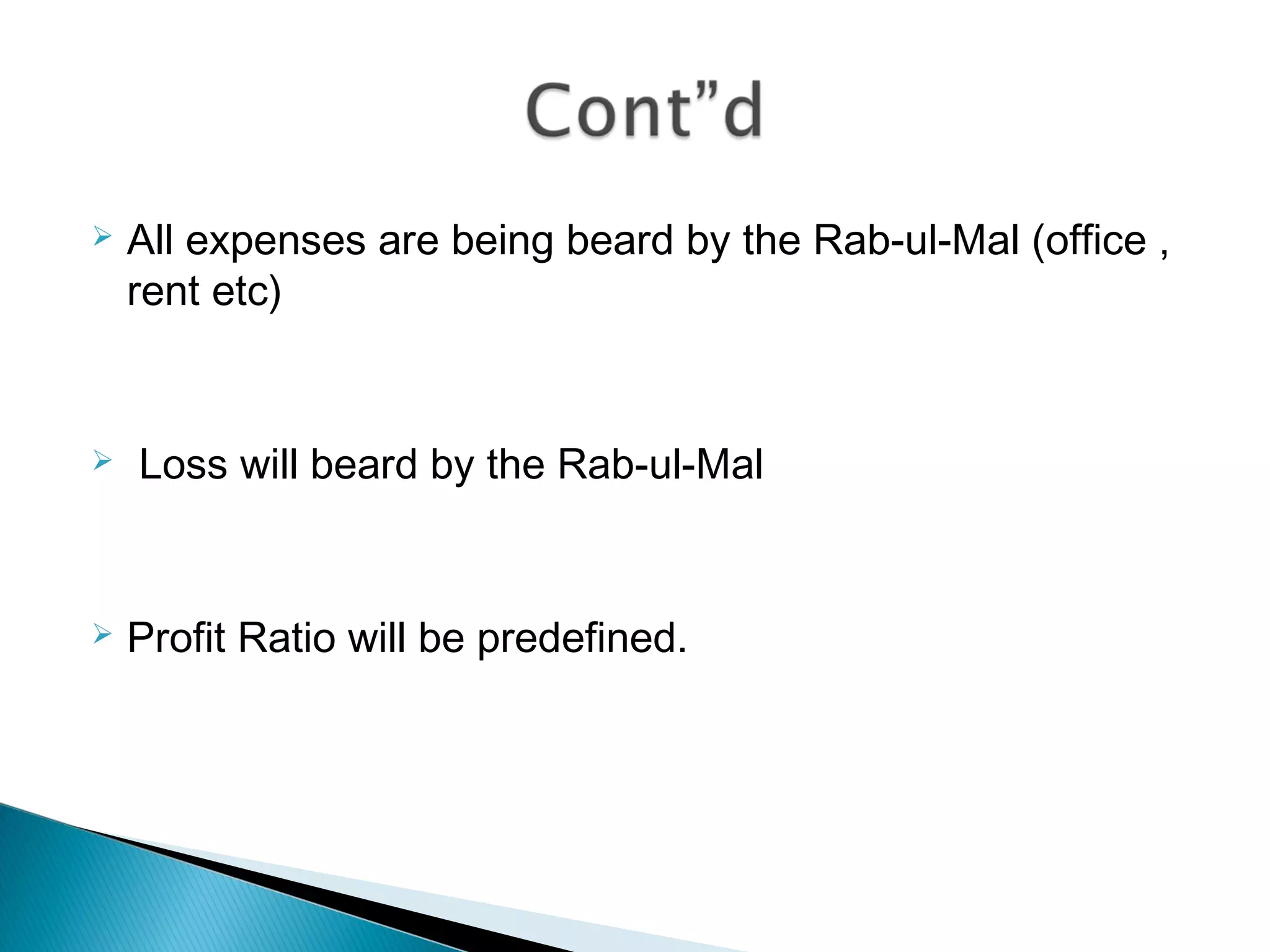

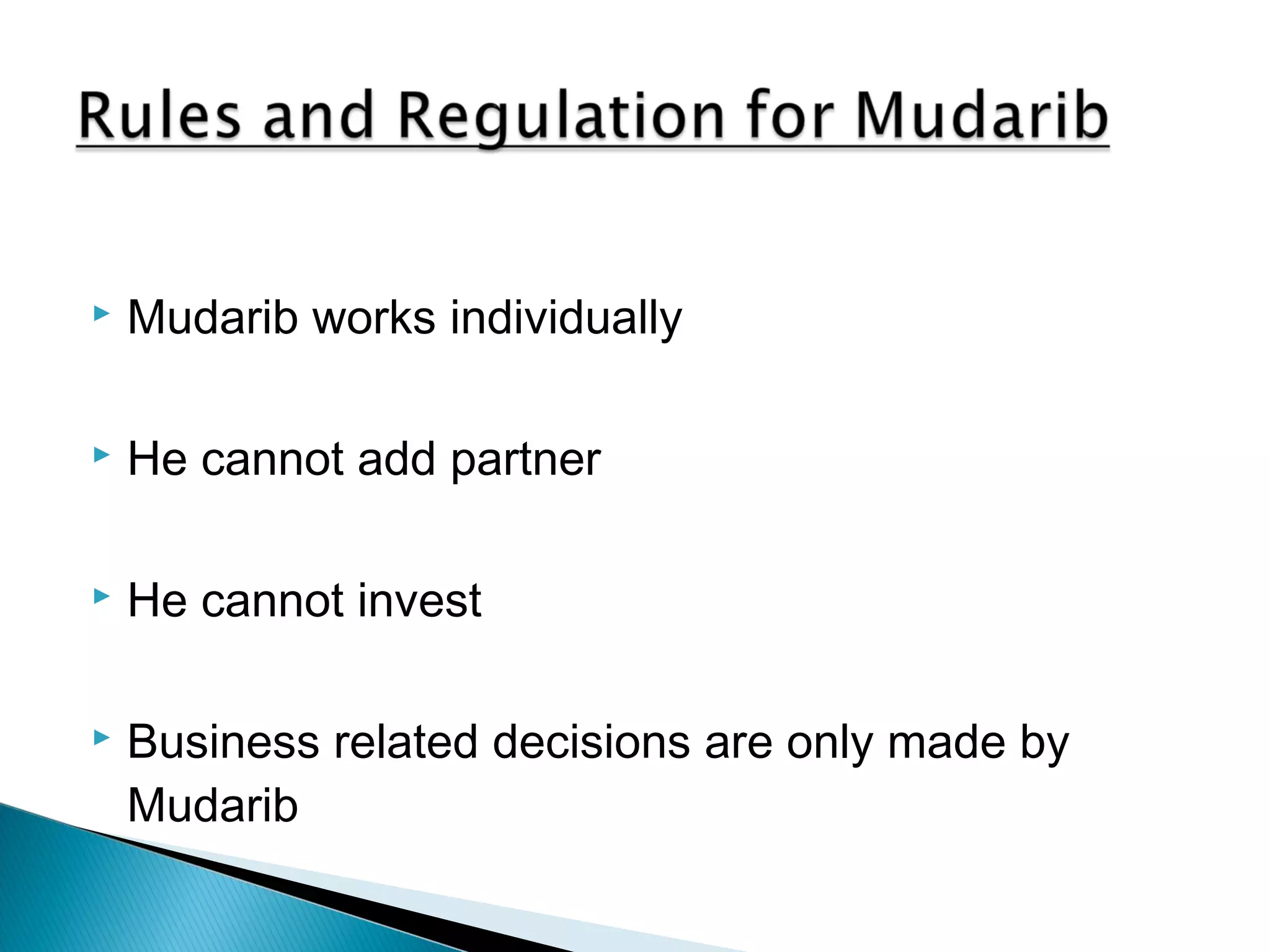

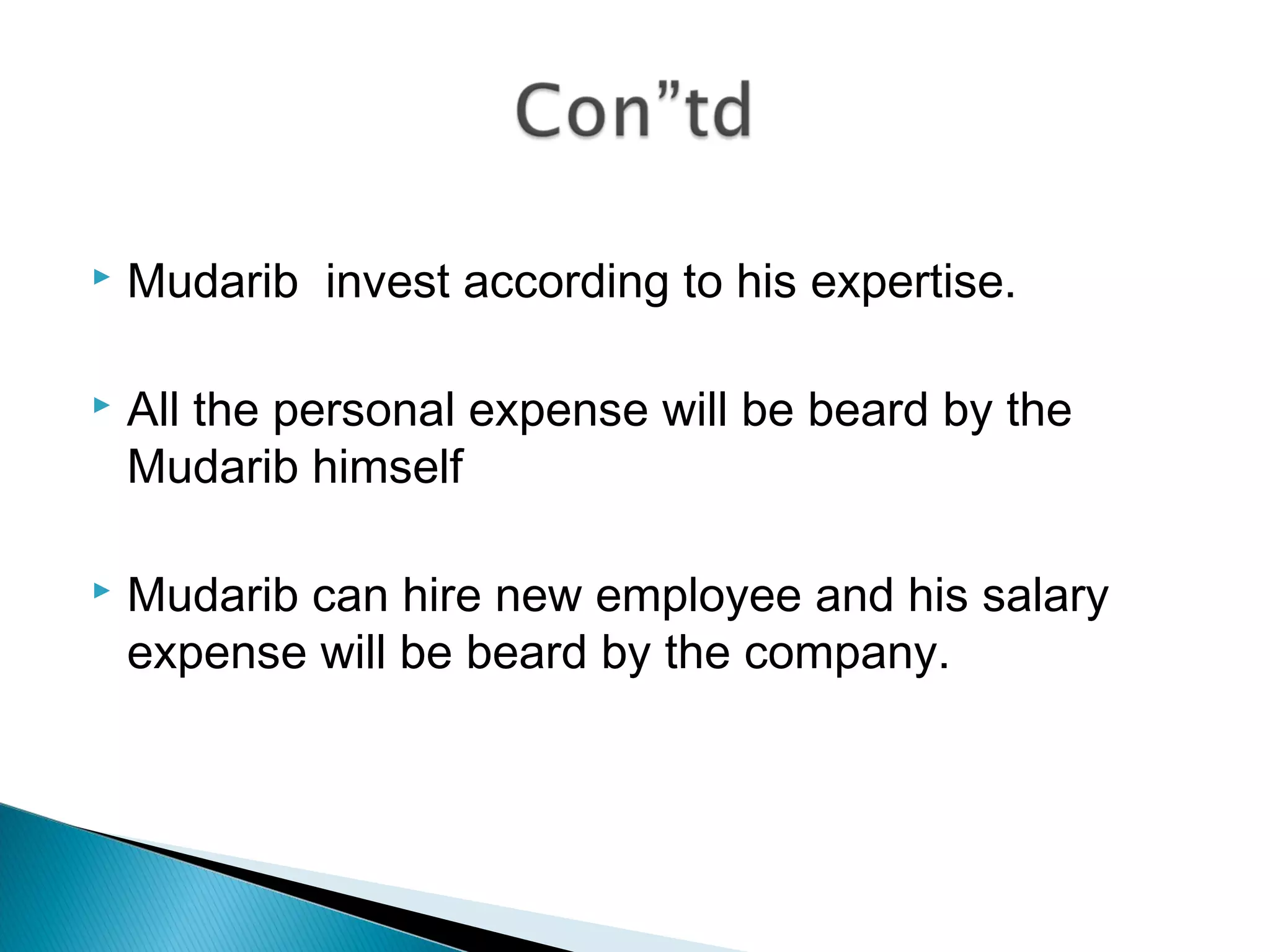

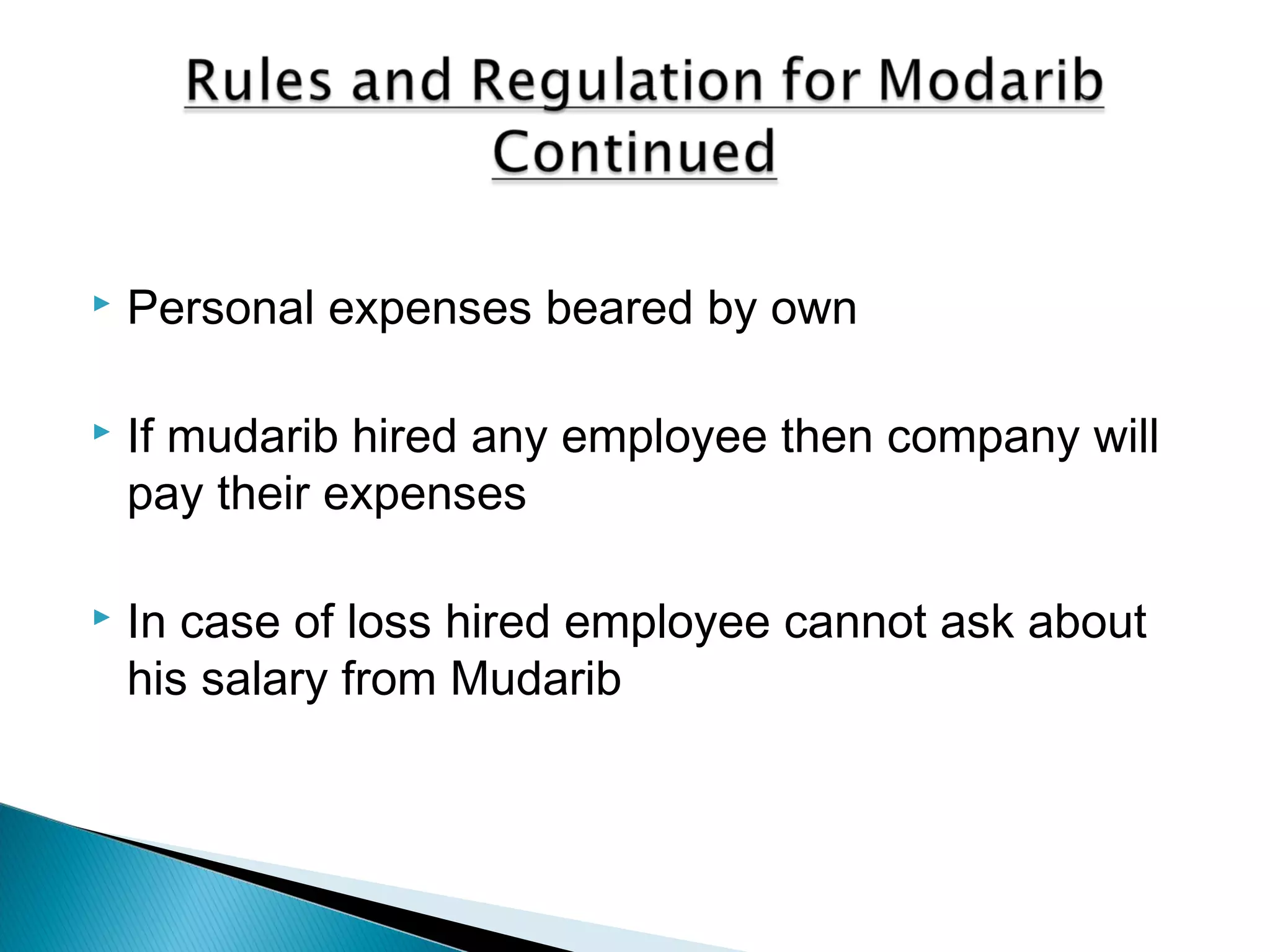

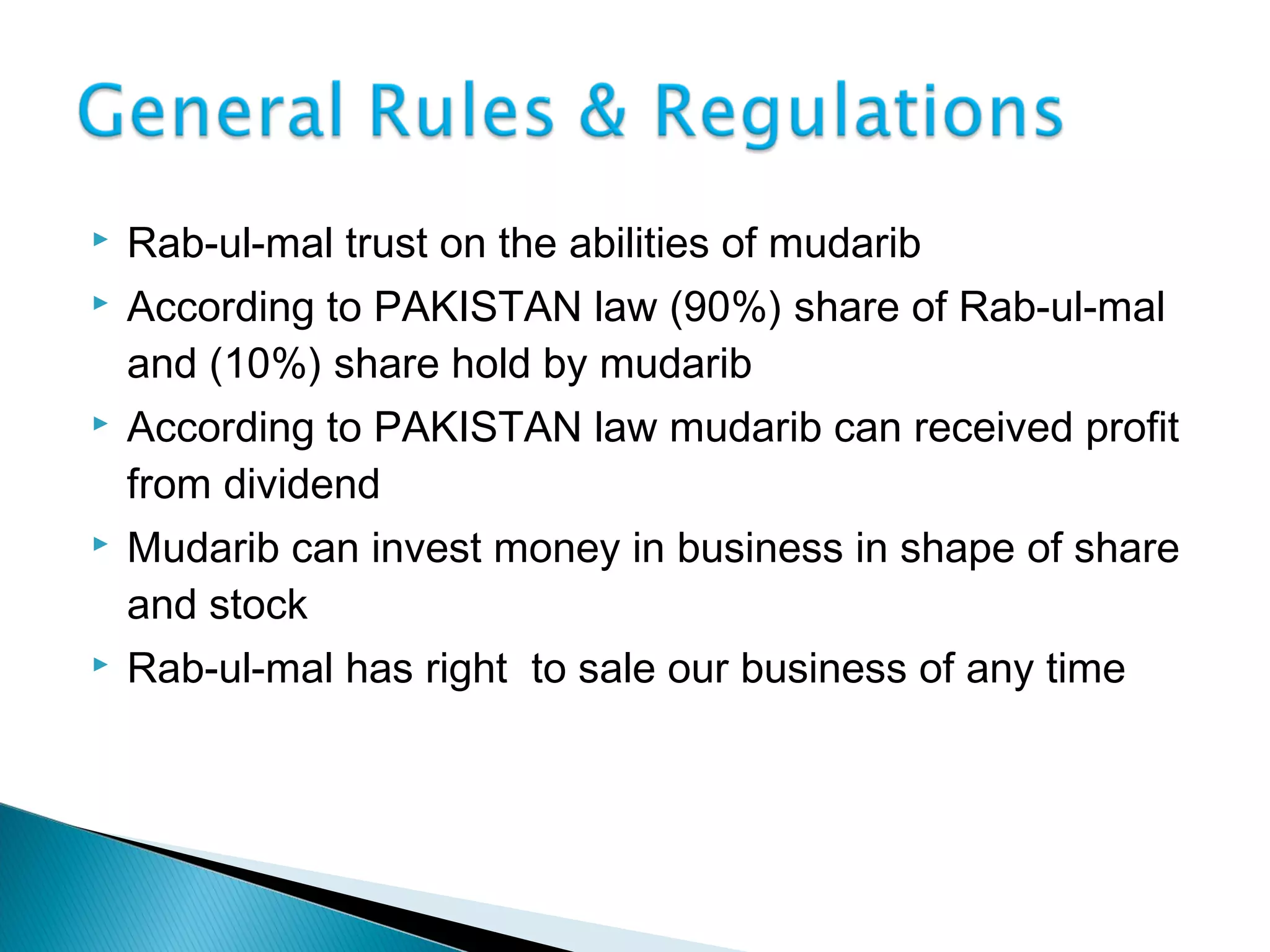

The document discusses Mudaraba, which is an Islamic financing concept where one party provides capital to another party to carry out a business venture. The two main parties are the Rab-ul-Mal, who provides the capital, and the Mudarib, who manages the business. The document outlines the roles and responsibilities of each party, as well as how profits and losses are distributed. It also provides information on the regulatory framework for Mudaraba companies in Pakistan and discusses ways to further develop the Islamic capital market.