Download as PDF, PPTX

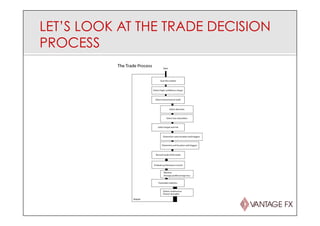

Module 1 of the forex fundamentals presentation by Abe Cofnas focuses on the importance of fundamental analysis, especially post-2008, in trading decisions. It highlights the significance of economic calendars and provides strategies for trading economic data releases, emphasizing the role of central banks and sentiment analysis in shaping market expectations. The module also discusses various trading strategies and the impact of surprise fundamental data on market movements.