The FOMC left interest rates unchanged but signaled a more patient approach to future rate hikes. Inflation remains near the 2% target while economic growth is solid. The statement removed prior language about further gradual rate hikes. The Fed will be patient in determining rate adjustments in light of global risks and muted inflation. Balance sheet normalization may end sooner with a larger balance sheet size than previously estimated.

Fed must relent. Our expectations now is for a state dependent (global financial conditions to stabilise, cushion rising debt repayment burden and allowing domestic leverage to level off, coupled with still moderate economic growth/inflation, policy options to widen positively globally, especially in China) Fed relent with scope for a final 25-50bps, if any (pause otherwise), in late 2019/2020, should the cycle extents, with the FFR hitting cycle terminal at 2.75-3.00%.

201906 FOMC - An ounce of prevention is worth a pound of cure, unless when th...QuanJianChingCFACAIA

Key drivers will revolve around, i) global trade negotiations/future framework and its implications; ii) contagion from global growth slowdown and weakness in the industrial sector (disruptions to semi-cons, autos, energy sectors; Boeing); and iii) changes, if any, to the Fed’s reaction function. We do not see sufficient evidence of a steep slowdown into an outright recession (though recognize the uncertainties) which markets have broadly priced. The scale of policy guidance and aggressively priced rates markets, we believe, will turn out to be an error. Global financial conditions are rapidly easing, pushing up asset valuations on highly uncertain fundamentals with aggressively dovish pricing limiting future policy room to support markets. Instead of seeking to dampen volatility, it would have been better to realign markets to the Fed’s (strategic) reaction function and allow global markets to find its own levels (via two way volatility).

Tactically, we think that duration is rich and see US5T and US10T closer to 2.30-2.60% into 1H20 (+10-15bps in breakevens; +30-40bps in TP), expecting a bear steepening; preferring rolling the 3 month. Duration-adjusted, prefer front/backend to 2-7 years.

With a backdrop of accommodative policy and our view of generally anchored inflation and resilient growth over coming quarters, we believe that risk/carry will remain supported into 2H19, within the current context (using more binary rather than probabilistic analytical lenses; prolonged clarity over the opportunity cost of risk-free asset amid broadly stable growth/inflation).

Lower for longer; constructive ambiguity. Chair Powell took pains to paint an image of constructive ambiguity, repeatedly highlighting that the Committee is focused on pursuing policy that is “appropriate” in achieving its dual mandate. The current policy stance is deemed appropriate with current projections achievable via modest policy adjustments (likely -75bps of cuts). Nonetheless, if the economy turns down, “a more extensive sequence of rate cuts is appropriate”. As we argued prior, “it is better to guide for looser policy in an open-ended manner (flattening backwardation of rate cut expectations) rather than encourage front-loading of rate cut expectations”. We think that the Chair has achieved such an outcome, together with “guidance” for an extended pause at a minimum; the best mix of policy, considering circumstances.

We like rates structurally, both on adequate valuations (breakeven levels: 5y, 3.55% (2.98%); and 10y, 3.36% (3.09%)) and as a hedge for risk assets, taking the under on the (largely) priced base case of a smooth 3 year (2018-2020) rate hiking cycle. Based on our macro risk-neutral model and pure expectations, we see 1.80-2.50% and 2.10-2.30% on the UST 5 and 10. Our view is to stay long on the UST 5-10y, prefer 7y; tactical view suggests range trading, 10T around 2.80-3.20%, into 1H19 (Fed hikes by 75bps to 2.75-3.00% by 1H19; anchor extent of rates rally; near term upside risks of a Republican sweep of the mid-terms, providing the President and the Republican Party with another opportunity to pursue even looser (pro-wealth) fiscal policy.

Over the past thirty years the neutral real interest rate across developed economies has declined substantially. Evidence suggests that secular rather than transitory factors are driving its decline. A lower neutral interest rate implies that the cumulative amount of tightening required for monetary policy to become neutral is much smaller than previously thought.

The Impact of Monetary Policy on Economic Growth and Price Stability in Kenya...iosrjce

The government of Kenya’s economic blueprint dubbed ‘Kenya Vision 2030’ acknowledges the

importance of maintaining a stable macro-economic environment. Despite Kenya implementing monetary

policy aimed at achieving stable prices and fostering economic growth, the economy has been reporting low

economic growth and high rates of inflation. These implies there is still a point of disconnect between what

Central bank of Kenya Pursues and the outcome of the objectives. In this study, structural vector autoregresion

(SVAR) model is estimatedto trace the effects of monetary policy shocks on economic growth and prices in

Kenya. Three alternative monetary policy instruments were put into use i.e. broad money supply (M3), interbank

lending rate (ILR) and the real effective exchange rate (REER). The study found evidence that monetary policy

innovations carried out on the quantity-based nominal anchor (M3) has modest effects on economic growth and

prices with a very fast speed of adjustment. Innovations on the price-based nominal anchors (ILR and REER)

have relative and fleeting effects on real GDP. The study recommended that Central Bank of Kenya should

place more emphasis on the use of the quantity-based nominal anchor rather than the price-based nominal

anchor

Ivo Pezzuto - "FED BITES THE BULLET - Implements First Rate Hike in Nearly a ...Dr. Ivo Pezzuto

The US Federal Reserve finally bites the bullet, increasing the

FFR – a key short-term interest rate – by quarter of a per cent.

With this, the regulator has clearly signaled that it might take

similar actions in future, if need arises, to take the economy

towards full recovery.

Fed must relent. Our expectations now is for a state dependent (global financial conditions to stabilise, cushion rising debt repayment burden and allowing domestic leverage to level off, coupled with still moderate economic growth/inflation, policy options to widen positively globally, especially in China) Fed relent with scope for a final 25-50bps, if any (pause otherwise), in late 2019/2020, should the cycle extents, with the FFR hitting cycle terminal at 2.75-3.00%.

201906 FOMC - An ounce of prevention is worth a pound of cure, unless when th...QuanJianChingCFACAIA

Key drivers will revolve around, i) global trade negotiations/future framework and its implications; ii) contagion from global growth slowdown and weakness in the industrial sector (disruptions to semi-cons, autos, energy sectors; Boeing); and iii) changes, if any, to the Fed’s reaction function. We do not see sufficient evidence of a steep slowdown into an outright recession (though recognize the uncertainties) which markets have broadly priced. The scale of policy guidance and aggressively priced rates markets, we believe, will turn out to be an error. Global financial conditions are rapidly easing, pushing up asset valuations on highly uncertain fundamentals with aggressively dovish pricing limiting future policy room to support markets. Instead of seeking to dampen volatility, it would have been better to realign markets to the Fed’s (strategic) reaction function and allow global markets to find its own levels (via two way volatility).

Tactically, we think that duration is rich and see US5T and US10T closer to 2.30-2.60% into 1H20 (+10-15bps in breakevens; +30-40bps in TP), expecting a bear steepening; preferring rolling the 3 month. Duration-adjusted, prefer front/backend to 2-7 years.

With a backdrop of accommodative policy and our view of generally anchored inflation and resilient growth over coming quarters, we believe that risk/carry will remain supported into 2H19, within the current context (using more binary rather than probabilistic analytical lenses; prolonged clarity over the opportunity cost of risk-free asset amid broadly stable growth/inflation).

Lower for longer; constructive ambiguity. Chair Powell took pains to paint an image of constructive ambiguity, repeatedly highlighting that the Committee is focused on pursuing policy that is “appropriate” in achieving its dual mandate. The current policy stance is deemed appropriate with current projections achievable via modest policy adjustments (likely -75bps of cuts). Nonetheless, if the economy turns down, “a more extensive sequence of rate cuts is appropriate”. As we argued prior, “it is better to guide for looser policy in an open-ended manner (flattening backwardation of rate cut expectations) rather than encourage front-loading of rate cut expectations”. We think that the Chair has achieved such an outcome, together with “guidance” for an extended pause at a minimum; the best mix of policy, considering circumstances.

We like rates structurally, both on adequate valuations (breakeven levels: 5y, 3.55% (2.98%); and 10y, 3.36% (3.09%)) and as a hedge for risk assets, taking the under on the (largely) priced base case of a smooth 3 year (2018-2020) rate hiking cycle. Based on our macro risk-neutral model and pure expectations, we see 1.80-2.50% and 2.10-2.30% on the UST 5 and 10. Our view is to stay long on the UST 5-10y, prefer 7y; tactical view suggests range trading, 10T around 2.80-3.20%, into 1H19 (Fed hikes by 75bps to 2.75-3.00% by 1H19; anchor extent of rates rally; near term upside risks of a Republican sweep of the mid-terms, providing the President and the Republican Party with another opportunity to pursue even looser (pro-wealth) fiscal policy.

Over the past thirty years the neutral real interest rate across developed economies has declined substantially. Evidence suggests that secular rather than transitory factors are driving its decline. A lower neutral interest rate implies that the cumulative amount of tightening required for monetary policy to become neutral is much smaller than previously thought.

The Impact of Monetary Policy on Economic Growth and Price Stability in Kenya...iosrjce

The government of Kenya’s economic blueprint dubbed ‘Kenya Vision 2030’ acknowledges the

importance of maintaining a stable macro-economic environment. Despite Kenya implementing monetary

policy aimed at achieving stable prices and fostering economic growth, the economy has been reporting low

economic growth and high rates of inflation. These implies there is still a point of disconnect between what

Central bank of Kenya Pursues and the outcome of the objectives. In this study, structural vector autoregresion

(SVAR) model is estimatedto trace the effects of monetary policy shocks on economic growth and prices in

Kenya. Three alternative monetary policy instruments were put into use i.e. broad money supply (M3), interbank

lending rate (ILR) and the real effective exchange rate (REER). The study found evidence that monetary policy

innovations carried out on the quantity-based nominal anchor (M3) has modest effects on economic growth and

prices with a very fast speed of adjustment. Innovations on the price-based nominal anchors (ILR and REER)

have relative and fleeting effects on real GDP. The study recommended that Central Bank of Kenya should

place more emphasis on the use of the quantity-based nominal anchor rather than the price-based nominal

anchor

Ivo Pezzuto - "FED BITES THE BULLET - Implements First Rate Hike in Nearly a ...Dr. Ivo Pezzuto

The US Federal Reserve finally bites the bullet, increasing the

FFR – a key short-term interest rate – by quarter of a per cent.

With this, the regulator has clearly signaled that it might take

similar actions in future, if need arises, to take the economy

towards full recovery.

Inflation targeting in Emerging Market Economies Sarthak Luthra

The presentation represents inflation targeting in EMEs, with a focus on various exchange rate regimes in Asian countries and their susceptibility to financial crisis.

Monetary Policy: Basic Overview of the 'Weapons of Monetary Policy' Use the specific power points and activities on Exchange Rates and Interest Rates to support your knowledge

Adopting Inflation Targeting for Monetary Policy: Practical Issues for Nigeriaiosrjce

IOSR Journal of Humanities and Social Science is a double blind peer reviewed International Journal edited by International Organization of Scientific Research (IOSR).The Journal provides a common forum where all aspects of humanities and social sciences are presented. IOSR-JHSS publishes original papers, review papers, conceptual framework, analytical and simulation models, case studies, empirical research, technical notes etc.

this presentation is currently have this upload set to Public. This means that it will be indexed by search engines and view able by anyone on the web.

The Hitchhiker's Guide to Yellen's Speech

We spent all week waiting anxiously to see what Our Glorious Leader would say only to get a confused mash-up of central bank water-cooler conversation.

If you want to know what she really said - and, more importantly, didn't say - you might like to read this translation.

Inflation targeting in Emerging Market Economies Sarthak Luthra

The presentation represents inflation targeting in EMEs, with a focus on various exchange rate regimes in Asian countries and their susceptibility to financial crisis.

Monetary Policy: Basic Overview of the 'Weapons of Monetary Policy' Use the specific power points and activities on Exchange Rates and Interest Rates to support your knowledge

Adopting Inflation Targeting for Monetary Policy: Practical Issues for Nigeriaiosrjce

IOSR Journal of Humanities and Social Science is a double blind peer reviewed International Journal edited by International Organization of Scientific Research (IOSR).The Journal provides a common forum where all aspects of humanities and social sciences are presented. IOSR-JHSS publishes original papers, review papers, conceptual framework, analytical and simulation models, case studies, empirical research, technical notes etc.

this presentation is currently have this upload set to Public. This means that it will be indexed by search engines and view able by anyone on the web.

The Hitchhiker's Guide to Yellen's Speech

We spent all week waiting anxiously to see what Our Glorious Leader would say only to get a confused mash-up of central bank water-cooler conversation.

If you want to know what she really said - and, more importantly, didn't say - you might like to read this translation.

Printer Version - Board of Governors of the Federal Reserve Sy.docxChantellPantoja184

Printer Version - Board of Governors of the Federal Reserve System

http://www.federalreserve.gov/newsevents/press/monetary/20150917a.htm[9/21/2015 2:49:59 PM]

Print

Press Release

Release Date: September 17, 2015

For immediate release

Information received since the Federal Open Market Committee met in July suggests that economic activity

is expanding at a moderate pace. Household spending and business fixed investment have been increasing

moderately, and the housing sector has improved further; however, net exports have been soft. The labor

market continued to improve, with solid job gains and declining unemployment. On balance, labor market

indicators show that underutilization of labor resources has diminished since early this year. Inflation has

continued to run below the Committee's longer-run objective, partly reflecting declines in energy prices and

in prices of non-energy imports. Market-based measures of inflation compensation moved lower; survey-

based measures of longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price

stability. Recent global economic and financial developments may restrain economic activity somewhat and

are likely to put further downward pressure on inflation in the near term. Nonetheless, the Committee

expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace,

with labor market indicators continuing to move toward levels the Committee judges consistent with its

dual mandate. The Committee continues to see the risks to the outlook for economic activity and the labor

market as nearly balanced but is monitoring developments abroad. Inflation is anticipated to remain near

its recent low level in the near term but the Committee expects inflation to rise gradually toward 2 percent

over the medium term as the labor market improves further and the transitory effects of declines in energy

and import prices dissipate. The Committee continues to monitor inflation developments closely.

To support continued progress toward maximum employment and price stability, the Committee today

reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains

appropriate. In determining how long to maintain this target range, the Committee will assess progress--

both realized and expected--toward its objectives of maximum employment and 2 percent inflation. This

assessment will take into account a wide range of information, including measures of labor market

conditions, indicators of inflation pressures and inflation expectations, and readings on financial and

international developments. The Committee anticipates that it will be appropriate to raise the target range

for the federal funds rate when it has seen some further improvement in the labor market and is

reasonably confident that inflation will move back to its 2 percent objective over the medium ter.

This is a study attempting to statistically measure the impact of Government policies on the economy and the stock market. The “causal” Government policies considered will include:

Fiscal Policy, entailing Budget Deficit spending;

Monetary Policy with the Federal Reserve managing the Federal Funds rate; and

Monetary Policy with the Federal Reserve conducting large purchases of securities (Treasuries, MBS);

The dependent or impacted macroeconomic variables affected by the above Government policies will include:

The overall economy (RGDP);

Inflation (CPI);

Unemployment Rate; and

Stock market.

INTERNATIONAL MONETARY FUND

Abstract

The U.S. financial and economic crisis has had severe global repercussions. The run-up to the crisis involved a substantial and widespread underestimation of risks—especially in housing—and growing leverage and liquidity mismatches, in particular through off-balance-sheet vehicles and non-bank entities in less-regulated areas. Against a backdrop of easy global financial conditions, this dynamic fed an unsustainable buildup of financial imbalances, above all in housing markets. The sharp decline in housing prices that started in 2007 weakened several systemically important financial institutions, culminating in the collapse of Lehman Brothers, and revealing major weaknesses in the U.S. regulatory and resolution frameworks. This was followed by the worst global financial panic since the Great Depression, with extreme strains in a broad range of markets, volatility in capital flows and exchange rates, and a cascade of systemic events. Economic activity collapsed globally, with trade contracting sharply and advanced economies as a group registering the steepest decline in production in the postwar period. Emerging markets economies also experienced intense pressure, amid retrenching trade and tighter international financing conditions.

I. Overview ; Outlook and Risks

1. Recent data suggest that the sharp fall in output may now be ending, although economic activity remains weak. Economic indicators point to a decelerating rate of deterioration, particularly in labor and housing markets, both of which are key to economic recovery and financial stability. In tandem, financial conditions have noticeably improved, with narrowing interest-rate spreads and growing confidence in financial stability in the wake of measures deployed by the Administration, the Federal Deposit Insurance Corporation (FDIC), and the Federal Reserve. That said, both financial and economic indicators remain at stressed or weak levels by historical standards.

2. 4. The staff's outlook remains for a gradual recovery, consistent with past international experience of financial and housing market crises. The combination of financial strains and ongoing adjustments in the housing and labor markets is expected to restrain growth for some time, with a solid recovery projected to emerge only in mid-2010. Against this background, GDP is expected to contract by 2½ percent in 2009, followed by a modest ¾ percent expansion in 2010 on a year-average basis (on a Q4-over-Q4 basis, -1 ½ percent in 2009 and 1 ¾ percent in 2010). Meanwhile, growing economic slack—with unemployment peaking at close to 10 percent in 2010—would push core inflation to very low levels, with the headline CPI expected to decrease by ½ percent in 2009 and increase by 1 percent in 2010. rates, on concerns about fiscal sustainability; and rising corporate distress. Much will also depend on developments abroad, including progress made in strengthening financial institutions and markets.

II. Near-term stabilization

1. Macroeconomic policies are providing welcome support to demand. The fiscal stimulus—well targeted, timely, diversified, and sizeable—is projected to boost annual GDP growth by 1 percent in 2009 and ¼ percent in 2010. This is being appropriately complemented by a highly expansionary monetary stance and “credit easing” measures that are also relieving financial strains. Continued clear communication on the near-term outlook will be essential to anchor inflation expectations, given the prevailing uncertainty. If activity proves weaker than expected, the Fed could undertake additional credit easing, and further strengthen its commitment to maintain a highly accommodative stance. If necessary, additional fiscal stimulus could also be considered, focused on fast-acting measures, although this would need to be complemented by a concomitantly stronger medium-term adjustment.

2. Steps to s

Ivo Pezzuto - FEDERAL RESERVE'S RATE RISE. COMING SOON? The Global Analyst Se...Dr. Ivo Pezzuto

This article, written on August 31st, 2015 by Prof. Ivo Pezzuto, predicts that mostly likely the Federal Reserve will hike interest rates at the December 16th-17th FOMC meeting, given the current global economic turbulence and outlook, and that a rate rise will be more likely at the end of 2015 or in early 2016 if the US economy will continue to improve and in the absence of systemic crises.

What recent and past actions have Canada and the US taken to counter.pdfmeejuhaszjasmynspe52

What recent and past actions have Canada and the US taken to counteract their exchange rates

with the economy in such distress over the past 10 years?

Solution

Since 2007, the world has experienced a period of severe financial stress, not seen since the time

of the Great Depression. This crisis started with the collapse of the subprime residential

mortgage market in the United States and spread to the rest of the world through exposure to

U.S. real estate assets, often in the form of complex financial derivatives, and a collapse in global

trade. Many countries were significantly affected by these adverse shocks, causing systemic

banking crises in a number of countries, despite extraordinary policy interventions. Systemic

banking crises are disruptive events not only to financial systems but to the economy as a whole.

Such crises are not specific to the recent past or specific countries – almost no country has

avoided the experience and some have had multiple banking crises. While the banking crises of

the past have differed in terms of underlying causes, triggers, and economic impact, they share

many commonalities. Banking crises are often preceded by prolonged periods of high credit

growth and are often associated with large imbalances in the balance sheets of the private sector,

such as maturity mismatches or exchange rate risk, that ultimately translate into credit risk for

the banking sector.

Crisis management starts with the containment of liquidity pressures through liquidity support,

guarantees on bank liabilities, deposit freezes, or bank holidays. This containment phase is

followed by a resolution phase during which typically a broad range of measures (such as capital

injections, asset purchases, and guarantees) are taken to restructure banks and reignite economic

growth. It is intrinsically difficult to compare the success of crisis resolution policies given

differences across countries and time in the size of the initial shock to the financial system, the

size of the financial system, the quality of institutions, and the intensity and scope of policy

interventions. With this caveat we now compare policy responses during the recent crisis episode

with those of the past. The policy responses during the 2007-2009 crises episodes were broadly

similar to those used in the past. First, liquidity pressures were contained through liquidity

support and guarantees on bank liabilities. Like the crises of the past, during which bank

holidays and deposit freezes have rarely been used as containment policies, we have no records

of the use of bank holidays during the recent wave of crises, while a deposit freeze was used only

in the case of Latvia for deposits in Parex Bank. On the resolution side, a wide array of

instruments was used this time, including asset purchases, asset guarantees, and equity injections.

All these measures have been used in the past, but this time around they seem to have been put in

place quicker (for detailed informatio.

Signs of inflation will raise the stakes for the Fed’s policy communications. Favorable conditions for leveraged strategies could reverse quickly. Reasonable valuations and the Fed’s policy goals continue to support risk assets.

Global Economic Update & Strategic Investment Outlook Q2 2014Cohen and Company

An informative overview of the current state of the global economy and the many factors that impact investment strategies, and a look at domestic economic indicators that may impact them.

Trekking markets & more with InvestrekkInves Trekk

The report presents a summary of the Indian market activity during the week ended 27 June 2021. It also provides some important insights about the global market trends and Indian Market outlook for the Week beginning 28 June 2021.

The classic balanced portfolio for more than 7 decades has been the blend of equities and bonds in the ratio of 60% to 40% respectively. But declining interest rates have forced investors to divert from this investing strategy and look over other alternatives. This has affected bond returns. And once again due to pandemic interest rates were

cut down to near zero resulting in very little returns in bonds. To overcome this, alternative investment opportunities should be looked for and several factors which are important in deciding the future investments are to be considered. Some of them are interest rates, valuations, volatility, etc. Based upon the factors and other parameters, the best alternatives will be Equities (cyclical industry, stocks providing dividends, etc), Corporate bonds (with higher

investment grades), and government bonds of emerging markets (like China and Peru). These alternatives will act as better investment alternatives to traditional 60/40 asset allocation in the current scenario.

Bank of Canada Decision and Real GDP – Preview

We expect a very close call for the monetary policy decision on Wednesday, with the Bank of Canada (BoC) leaving the overnight rate target unchanged at 1.25%.

Bank of Canada Decision and Real GDP – Preview

We expect a very close call for the monetary policy decision on Wednesday, with the Bank of Canada (BoC) leaving the overnight rate target unchanged at 1.25%.

Bank of Canada Decision and Real GDP – Preview

We expect a very close call for the monetary policy decision on Wednesday, with the Bank of Canada (BoC) leaving the overnight rate target unchanged at 1.25%.

What website can I sell pi coins securely.DOT TECH

Currently there are no website or exchange that allow buying or selling of pi coins..

But you can still easily sell pi coins, by reselling it to exchanges/crypto whales interested in holding thousands of pi coins before the mainnet launch.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and resell to these crypto whales and holders of pi..

This is because pi network is not doing any pre-sale. The only way exchanges can get pi is by buying from miners and pi merchants stands in between the miners and the exchanges.

How can I sell my pi coins?

Selling pi coins is really easy, but first you need to migrate to mainnet wallet before you can do that. I will leave the telegram contact of my personal pi merchant to trade with.

Tele-gram.

@Pi_vendor_247

how to sell pi coins in South Korea profitably.DOT TECH

Yes. You can sell your pi network coins in South Korea or any other country, by finding a verified pi merchant

What is a verified pi merchant?

Since pi network is not launched yet on any exchange, the only way you can sell pi coins is by selling to a verified pi merchant, and this is because pi network is not launched yet on any exchange and no pre-sale or ico offerings Is done on pi.

Since there is no pre-sale, the only way exchanges can get pi is by buying from miners. So a pi merchant facilitates these transactions by acting as a bridge for both transactions.

How can i find a pi vendor/merchant?

Well for those who haven't traded with a pi merchant or who don't already have one. I will leave the telegram id of my personal pi merchant who i trade pi with.

Tele gram: @Pi_vendor_247

#pi #sell #nigeria #pinetwork #picoins #sellpi #Nigerian #tradepi #pinetworkcoins #sellmypi

The Evolution of Non-Banking Financial Companies (NBFCs) in India: Challenges...beulahfernandes8

Role in Financial System

NBFCs are critical in bridging the financial inclusion gap.

They provide specialized financial services that cater to segments often neglected by traditional banks.

Economic Impact

NBFCs contribute significantly to India's GDP.

They support sectors like micro, small, and medium enterprises (MSMEs), housing finance, and personal loans.

Even tho Pi network is not listed on any exchange yet.

Buying/Selling or investing in pi network coins is highly possible through the help of vendors. You can buy from vendors[ buy directly from the pi network miners and resell it]. I will leave the telegram contact of my personal vendor.

@Pi_vendor_247

Exploring Abhay Bhutada’s Views After Poonawalla Fincorp’s Collaboration With...beulahfernandes8

The financial landscape in India has witnessed a significant development with the recent collaboration between Poonawalla Fincorp and IndusInd Bank.

The launch of the co-branded credit card, the IndusInd Bank Poonawalla Fincorp eLITE RuPay Platinum Credit Card, marks a major milestone for both entities.

This strategic move aims to redefine and elevate the banking experience for customers.

how to sell pi coins on Bitmart crypto exchangeDOT TECH

Yes. Pi network coins can be exchanged but not on bitmart exchange. Because pi network is still in the enclosed mainnet. The only way pioneers are able to trade pi coins is by reselling the pi coins to pi verified merchants.

A verified merchant is someone who buys pi network coins and resell it to exchanges looking forward to hold till mainnet launch.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

what is the future of Pi Network currency.DOT TECH

The future of the Pi cryptocurrency is uncertain, and its success will depend on several factors. Pi is a relatively new cryptocurrency that aims to be user-friendly and accessible to a wide audience. Here are a few key considerations for its future:

Message: @Pi_vendor_247 on telegram if u want to sell PI COINS.

1. Mainnet Launch: As of my last knowledge update in January 2022, Pi was still in the testnet phase. Its success will depend on a successful transition to a mainnet, where actual transactions can take place.

2. User Adoption: Pi's success will be closely tied to user adoption. The more users who join the network and actively participate, the stronger the ecosystem can become.

3. Utility and Use Cases: For a cryptocurrency to thrive, it must offer utility and practical use cases. The Pi team has talked about various applications, including peer-to-peer transactions, smart contracts, and more. The development and implementation of these features will be essential.

4. Regulatory Environment: The regulatory environment for cryptocurrencies is evolving globally. How Pi navigates and complies with regulations in various jurisdictions will significantly impact its future.

5. Technology Development: The Pi network must continue to develop and improve its technology, security, and scalability to compete with established cryptocurrencies.

6. Community Engagement: The Pi community plays a critical role in its future. Engaged users can help build trust and grow the network.

7. Monetization and Sustainability: The Pi team's monetization strategy, such as fees, partnerships, or other revenue sources, will affect its long-term sustainability.

It's essential to approach Pi or any new cryptocurrency with caution and conduct due diligence. Cryptocurrency investments involve risks, and potential rewards can be uncertain. The success and future of Pi will depend on the collective efforts of its team, community, and the broader cryptocurrency market dynamics. It's advisable to stay updated on Pi's development and follow any updates from the official Pi Network website or announcements from the team.

what is the best method to sell pi coins in 2024DOT TECH

The best way to sell your pi coins safely is trading with an exchange..but since pi is not launched in any exchange, and second option is through a VERIFIED pi merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and pioneers and resell them to Investors looking forward to hold massive amounts before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade pi coins with.

@Pi_vendor_247

how to sell pi coins at high rate quickly.DOT TECH

Where can I sell my pi coins at a high rate.

Pi is not launched yet on any exchange. But one can easily sell his or her pi coins to investors who want to hold pi till mainnet launch.

This means crypto whales want to hold pi. And you can get a good rate for selling pi to them. I will leave the telegram contact of my personal pi vendor below.

A vendor is someone who buys from a miner and resell it to a holder or crypto whale.

Here is the telegram contact of my vendor:

@Pi_vendor_247

where can I find a legit pi merchant onlineDOT TECH

Yes. This is very easy what you need is a recommendation from someone who has successfully traded pi coins before with a merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi network coins and resell them to Investors looking forward to hold thousands of pi coins before the open mainnet.

I will leave the telegram contact of my personal pi merchant to trade with

@Pi_vendor_247

how to sell pi coins in all Africa Countries.DOT TECH

Yes. You can sell your pi network for other cryptocurrencies like Bitcoin, usdt , Ethereum and other currencies And this is done easily with the help from a pi merchant.

What is a pi merchant ?

Since pi is not launched yet in any exchange. The only way you can sell right now is through merchants.

A verified Pi merchant is someone who buys pi network coins from miners and resell them to investors looking forward to hold massive quantities of pi coins before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

when will pi network coin be available on crypto exchange.DOT TECH

There is no set date for when Pi coins will enter the market.

However, the developers are working hard to get them released as soon as possible.

Once they are available, users will be able to exchange other cryptocurrencies for Pi coins on designated exchanges.

But for now the only way to sell your pi coins is through verified pi vendor.

Here is the telegram contact of my personal pi vendor

@Pi_vendor_247

when will pi network coin be available on crypto exchange.

201901 FOMC

1. FOMC Jan 2019 statement. Highlights (1)

•No change, 2.25-2.50%. Unanimous, regional voting members rotated with J.Bullard and C.Evans deemed more dovish members, E.Rosengren, a

neutral and E.George more hawkish.

•Characterisation of economic activities downgraded slightly. Economic activity is now seen to be rising at a “solid rate” instead of “strong”.

Outside of this slight change, the characterisation of the economy was left unchanged. Household spending “continued to grow strongly” while growth of

business fixed investment has “moderated from its rapid pace earlier”. The labour market has “continued to strengthen”; job gains have been “strong”

(unchanged compared to economic activity – “solid”), on average, and the unemployment rate remained low.

•Inflation “remain near 2%”, market-based measures of inflation compensation “moved lower”. Both headline and core prices remain

“near 2%”. However, market-based measures of inflation compensation have “moved lower” though survey-based measures of longer-term inflation

expectations are “little changed”.

•Sharp dovish turn in forward guidance, appropriateness of the level of FFR vis-à-vis “further” increases. The Committee “in support” of its

mandate decided to keep the FFR unchanged instead of its previous judgement (statement explicitly removed in Jan) that further gradual increases will

be consistent with its mandate. As a base case, the Fed continues to view sustained expansion of economic activity, strong labour market conditions and

inflation near the symmetric 2% objective over the medium term as the most likely outcomes. The Committee will be “patient” in light of “global

economic and financial developments and muted inflation pressures” in determining “what” future “adjustments” (introducing policy symmetry) to the

FFRs may be appropriate to support these outcomes.

During QnA, when asked whether policy is still deemed “accommodative” as purported in Dec, the Chair replied that the Committee see the current

stance of policy as “appropriate” with spot FFR within the range of Committee’s neutral estimates. Further, the degree of the Committee’s patient will

depend on the evolution of incoming data and its implications on the outlook. The Chair did state that current cross-currents may yet play out “for a

while”.

Prudent risk management in play, uncertainty over balance of risks. Explicit characterisation of risks to the economic outlook have been

dropped, suggesting more heightened uncertainties.

2. FOMC Jan 2019 statement. Highlights (2)

•Data dependency still in play. In determining the timing and size of adjustments to the FFR, realized and expected economic conditions will be

assessed relative to the i) maximum employment objective and ii) symmetric 2% inflation target. The Committee will take into account a wide range of

information including labour market conditions, inflation pressures and expectations, and readings on financial and international developments.

•Dovish guidance on balance sheet policy; clearly not on auto-pilot. Despite again highlighting the primacy of interest rate policy, the

Committee now sees the balance sheet as an active part of monetary policy consideration. First, on size, the Committee intends to implement monetary

policy whereby “an ample supply of reserves” ensures that control over rates is exercised primarily through the setting of administered rates (in which

active management of the supply of reserves is not required); and, secondly, on monetary policy, the Committee is prepared to “adjust any of the details”

for completing balance sheet normalization in light of economic and financial developments. The Committee stands ready “to use its full range of tools,

including altering the size and composition of its balance sheet”, if future economic conditions were to warrant a more accommodative monetary policy

than can be achieved solely by reducing the FFR.

On 1), the ultimate size of our balance sheet will be driven principally by FIs’ demand for reserves, plus a buffer so that fluctuations in reserve demand do

not require frequent sizable market interventions. Based on surveys and market intelligence, current estimates of reserve demand are considerably

higher than estimates of a year or so ago. The implication is that the normalization of the size of the portfolio will be completed sooner, and with a larger

balance sheet, than in previous estimates.

•Rationale behind policy shifts. The Committee decided that the “cumulative” effects of recent developments (global growth slowdown, global and

domestic politics and geo-politics, tightening financial conditions, and weakening domestic survey data) and rising risks of a less favourable outlook

warrant a “patient, wait and see” approach to future policy-making. This is within a context of muted inflationary pressures (muted realised data, lower

oil, stable/lower expectations) and receding risk of financial imbalances.

7 Governors, Board FRBNY (VC FOMC)

J.Powell (C) J.Williams J.Bullard St. Louis

R.Clarida (VC) C.Evans Chicago

L.Brainard E.Rosengren Boston

R.Quarles E.George Kansas

M.Bowman

M.Goodfriend*

Nellie Liang*

*Pending

FOMC, 10/12 Members; 2019

4 Groups: (Boston, Philadelphia, Richmond);

(Cleveland, Chicago); (Atlanta, St. Louis,

Dallas); (Minneapolis, Kansas, St Francisco)

Permanent, 7 + 1 Rotating, 1Yr Term, 4/11

4 Regional Presidents

4. Thoughts (1)

Fed relented, in a big way. The Fed is seemingly now on hold, being patient in policy-making and awaiting macroeconomic and financial data in

determining what its next move (policy symmetry) will most likely be vis-à-vis its expectations of further tightening previously. Further, balance sheet

policy is apparently not on auto-pilot with the Fed willing to consider changes to the size and end point of run-off as dictated by developments. This likely

reflects a sense of heightened downside risks with the Chair suggesting that changes were made (to forward policy rate and balance sheet guidance) in

order to offset such concerns over rising risks, considering broadly unchanged spot levels of employment/inflation (both in line with mandates). The Fed

is thus unlikely to shift policy in 1H19.

Policy whiplash. Again, we think that the Fed is making a communication error (swinging from being too nonchalant in Dec to too dovish now). The

scale of dovish policy guidance, compared with likely trajectory of the economy, considering realised and evolving market movements, will likely place

the Fed in a bind should it seeks to raise rates, going forward. The economy is not that weak with financial conditions already starting to ease, on the back

of Fed speeches following Dec’s FOMC (which have help contained financial distress risks). External demand may yet be challenged but following an

improvement in financial conditions, coupled with more dovish domestic policy-making (globally, especially in China and Europe) should start to see a

cyclical improvement, going forward. Instead of seeking to dampen volatility via essentially a form of statement based guidance (patient, balance of risk,

appropriate), it would have been better to allow global markets to find its own levels (via two way volatility) in accordance to a new evolving market

perceived neutral (which markets are trying to do prior to this new perceived policy “put”) rather than anchoring at current levels (in accordance with the

“appropriate” language).

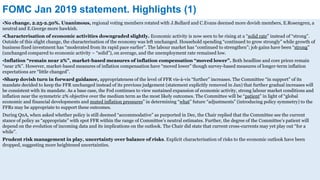

-18

-10

-39

-26

86

59

29 24

-80

-60

-40

-20

0

20

40

60

80

100

5Y 10Y

2018, bps chng TP Breakevens Implied Real Rate Nominal

-1

-6

12 6

-6 -1

5

-1

-10

-5

0

5

10

15

5Y 10Y

2019, bps chng TP Breakevens Implied Real Rate Nominal

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

Impulse, z-score, yoy chng FCI

5. Thoughts (2)

Policy “collar” not “put”. Prior expectations for a Fed relent has been (overly) met, hence our state dependent (global financial conditions to stabilise,

cushion rising debt repayment burden and allowing domestic leverage to level off, coupled with still moderate economic growth/inflation, policy options

to widen positively globally, especially in China) expectations for a final 25-50bps will likely be met in 2H19, should the cycle extents, with the FFR

hitting cycle terminal at 2.75-3.00%. Fed relent, we believe, is a policy collar, not a put. Global financial conditions are now easing pretty rapidly (on Fed

anchoring), pushing up asset valuations on uncertain fundamentals with aggressively dovish pricing limiting future policy room to support markets, if

needed. More importantly, a hike (to anchor financial conditions, asset pricing, term out leverage) will now be a communication nightmare with a likely

more dramatic negative impact on volatility and markets. The Fed has seemingly yet to learn the lesson on the impossibility for central bankers to

manage/time the impact of monetary policy adjustments on financial conditions (reflects inherent complexities of markets).

Rates commentary

Markets have pricing dovishly. Rates markets are priced for a Fed that is on hold for 2019 and then a cut and hold for 2020 and 2021 with a neutral

around 2.25-2.50%. Key drivers will revolve around, i) extent of the easing of financial conditions easing; ii) global growth trajectory, and iii) extent of US

growth/inflation momentum moderation via-a-vis Fed’s outlook. Tactically, we think duration is rich, expecting a bear steepening, preferring the 2-5yr.

-0.5

0.0

0.5

1.0

1.5

2.0

Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18 Jan-19

% 5Yr Implied Real Rate 10Yr Implied Real Rate

0

1

2

3

4

5

6

1Q62 1Q68 1Q74 1Q80 1Q86 1Q92 1Q98 1Q04 1Q10 1Q16

% Laubach-Williams Real Neutral Interest Rate

-4

-2

0

2

4

6

8

10

12

14

16

Jan-87 Jan-91 Jan-95 Jan-99 Jan-03 Jan-07 Jan-11 Jan-15 Jan-19

Policy-rule Models, % Williams, Orphanides Robust 1st Diff FFR