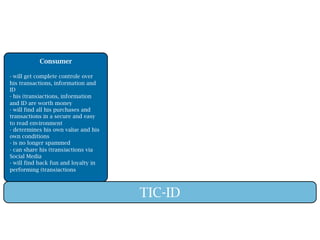

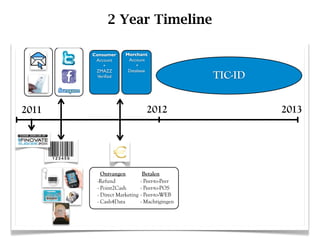

The document discusses how the world is rapidly changing due to technology and the rise of new generations. It notes that younger generations have different skills and ways of working compared to older generations. The document then outlines the vision, mission, and ambitions of Euro-Wallet, which aims to give people control over their money, data, and identities by creating a widely accepted mobile payment and intelligence platform across Europe that makes transactions free, easy, and fun.