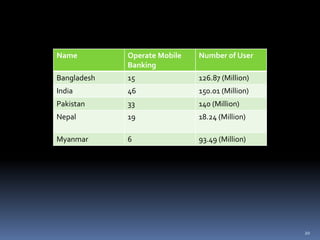

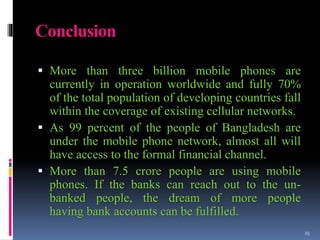

Mobile banking allows users to conduct banking transactions through their mobile phones. It first began in the late 1960s and has since expanded, with the first mobile banking services in Bangladesh launched in the 2000s by Dutch-Bangla Bank and BRAC Bank. Currently around 15 banks in Bangladesh offer mobile banking services through partnerships with major mobile network operators. While mobile banking provides increased access and convenience, challenges remain in expanding awareness and ensuring security of mobile financial transactions.