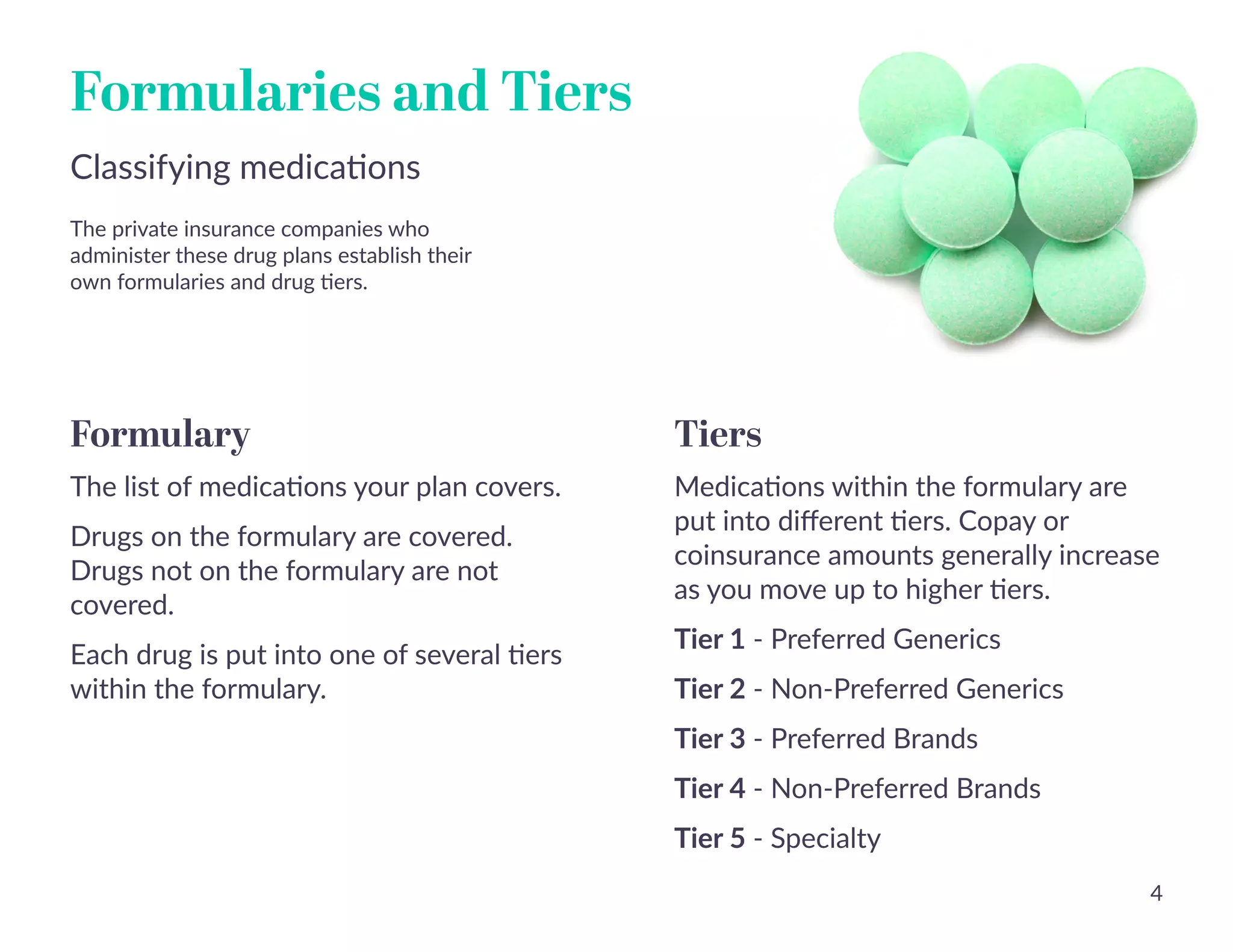

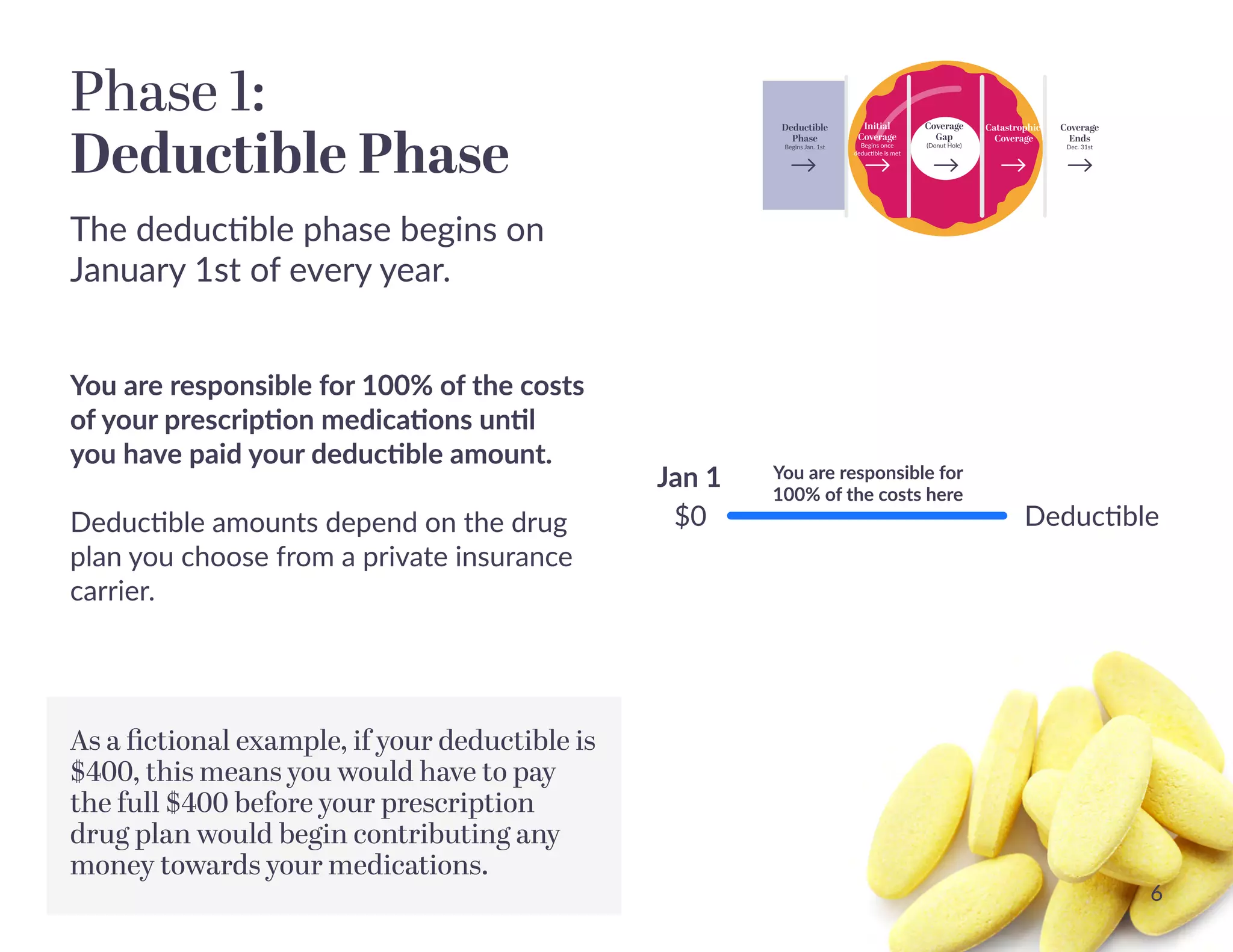

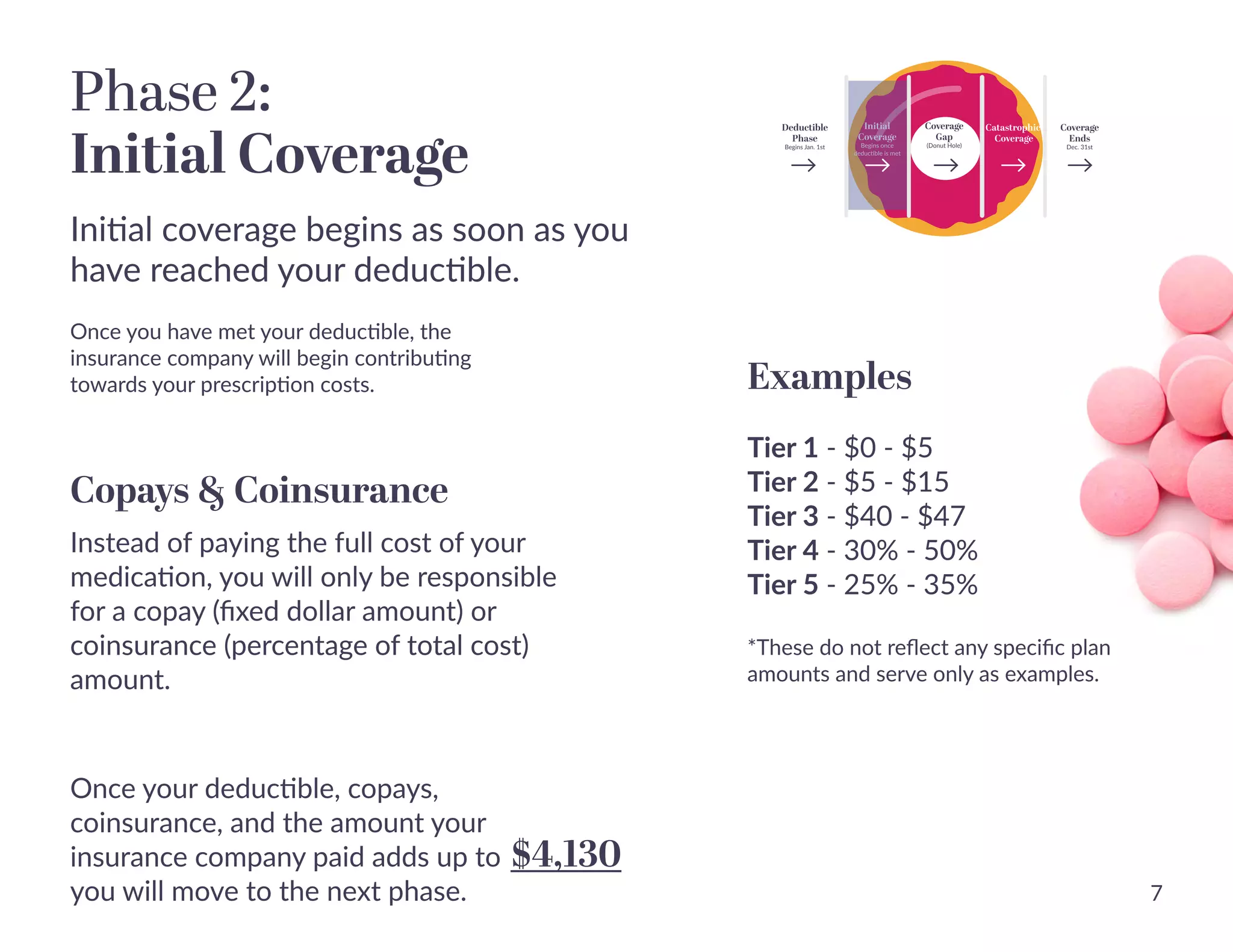

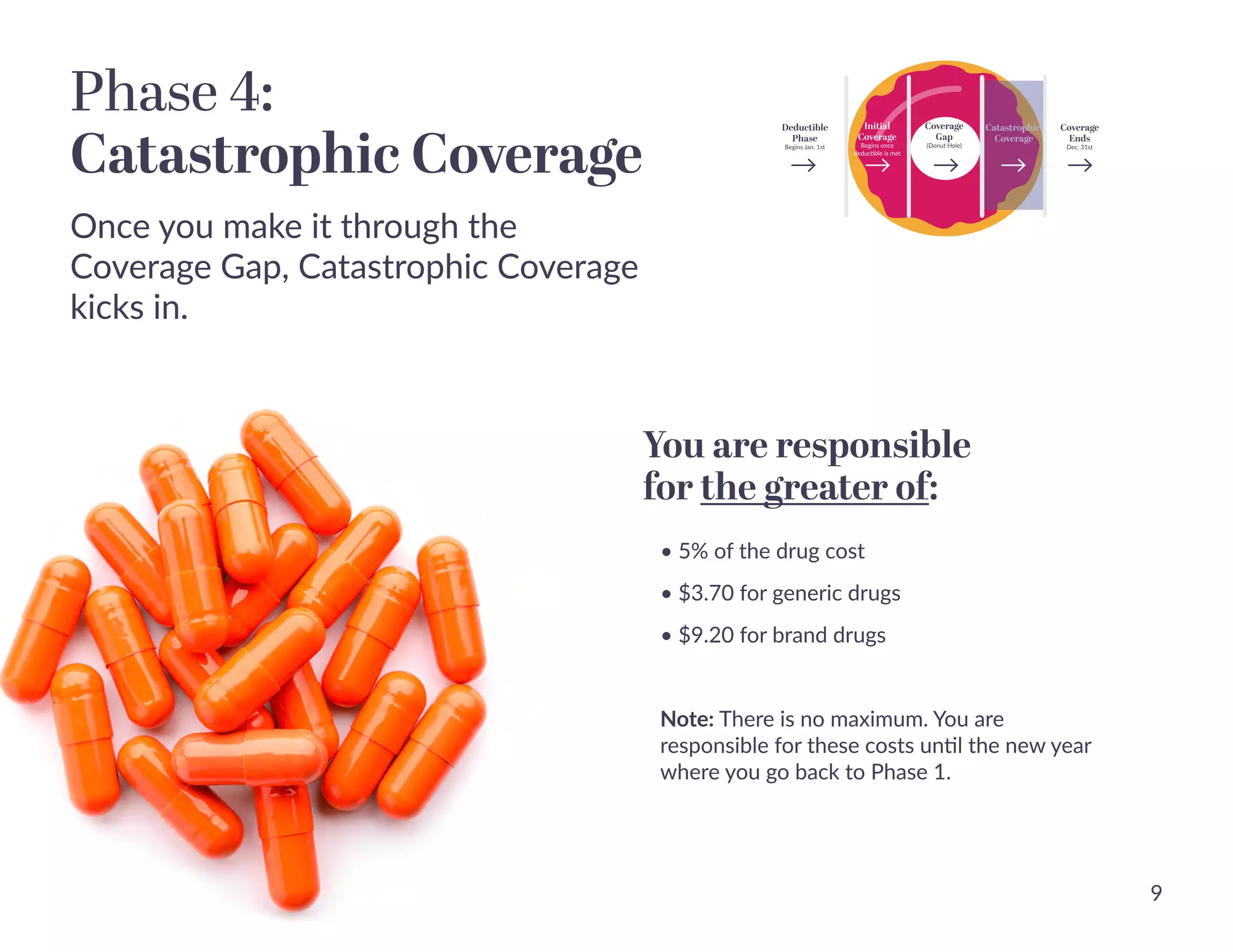

Medicare Part D provides coverage for prescription drugs, filling a gap left by original Medicare, and is administered by private insurance companies with their own formularies and tiered medication lists. It consists of four phases: deductible, initial coverage, coverage gap (donut hole), and catastrophic coverage, affecting costs and payment responsibilities at each stage. Enrollment is crucial to avoid penalties and high out-of-pocket costs for medications if a plan is not selected during the initial enrollment window.

![Understanding Parkinson’s Disease: Causes, Symptoms, and Treatment [2025]](https://cdn.slidesharecdn.com/ss_thumbnails/understandingparkinson-251208102525-80ba3223-thumbnail.jpg?width=640&height=640&fit=bounds)