Downloaded 26 times

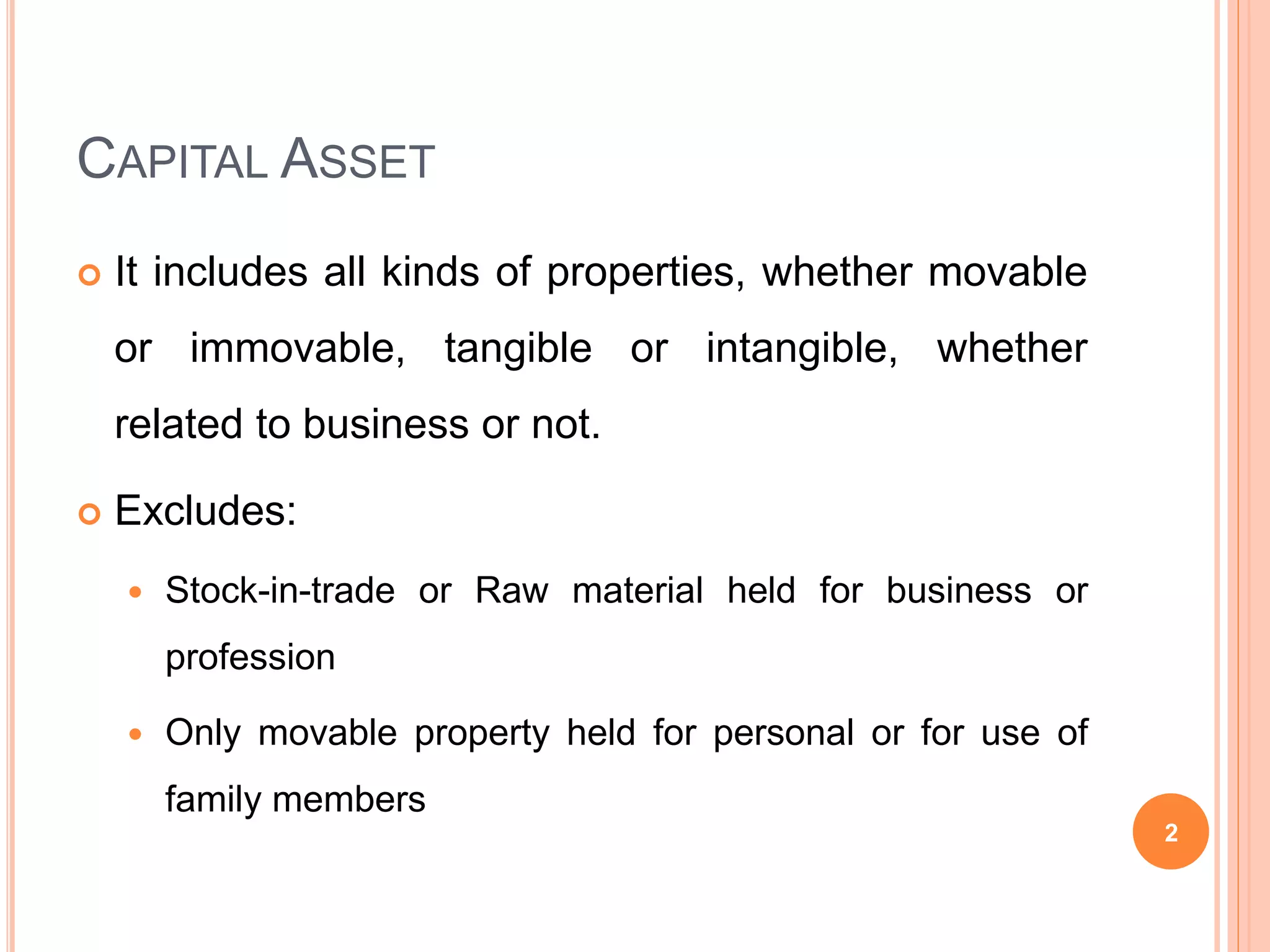

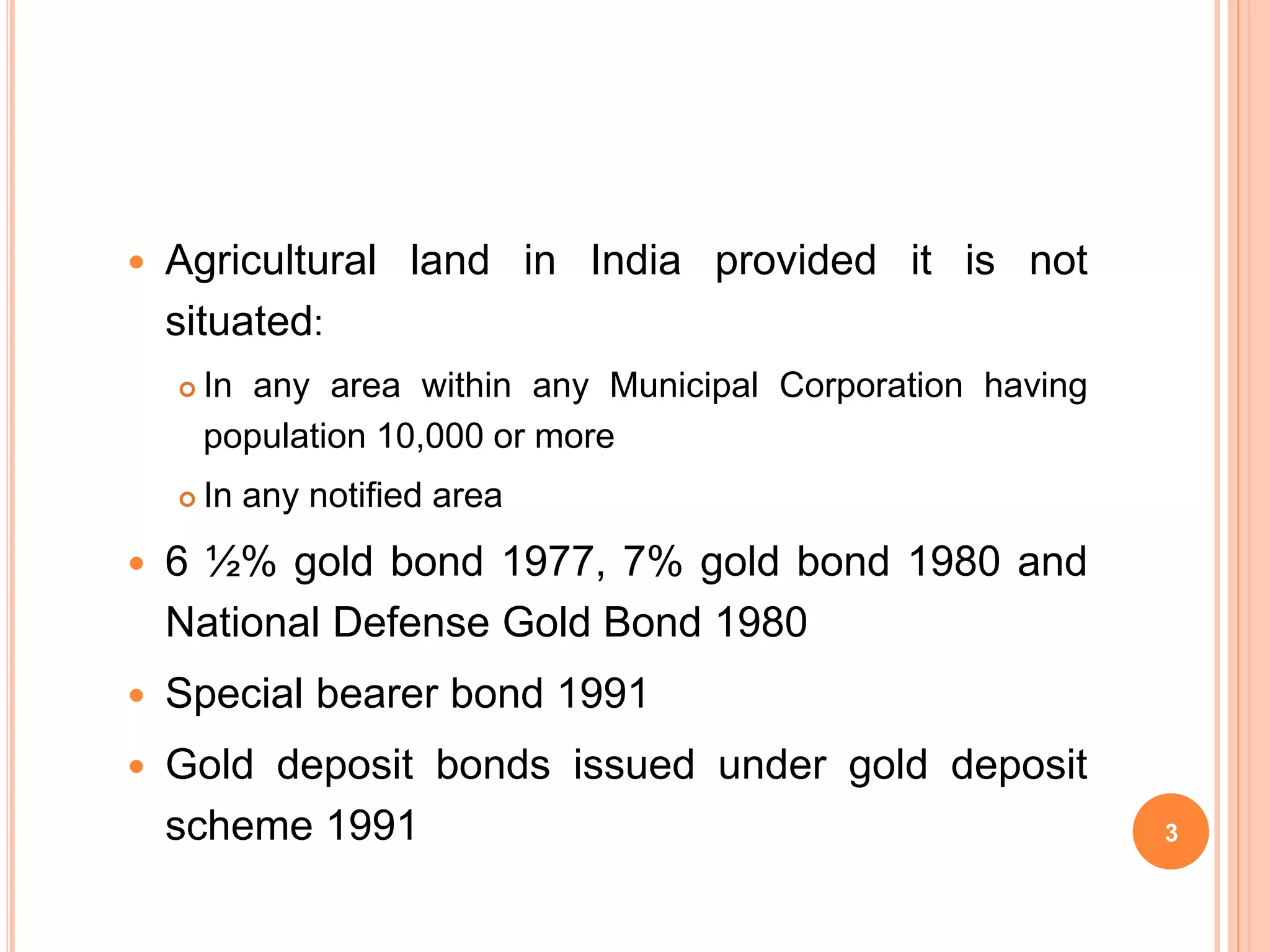

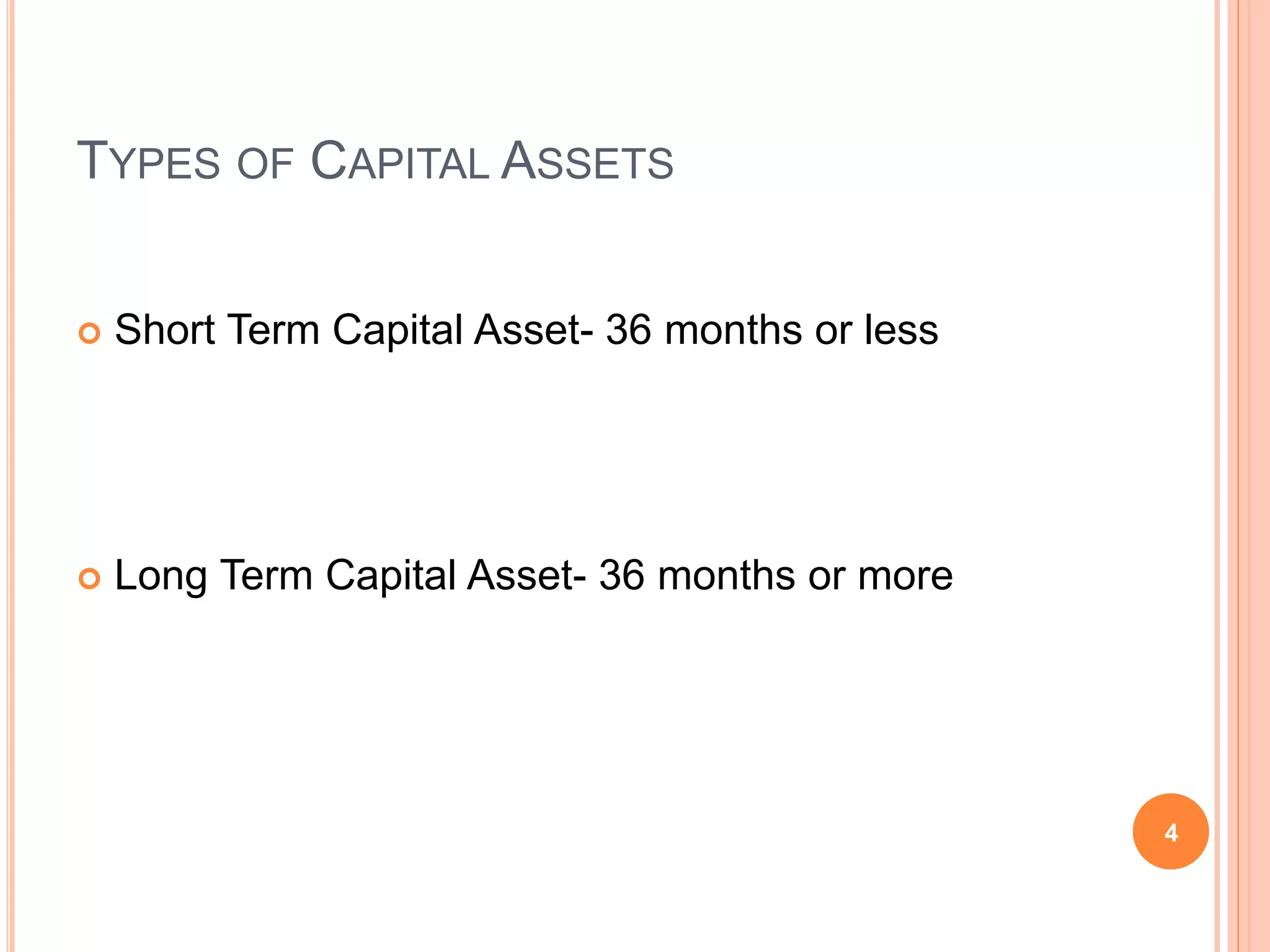

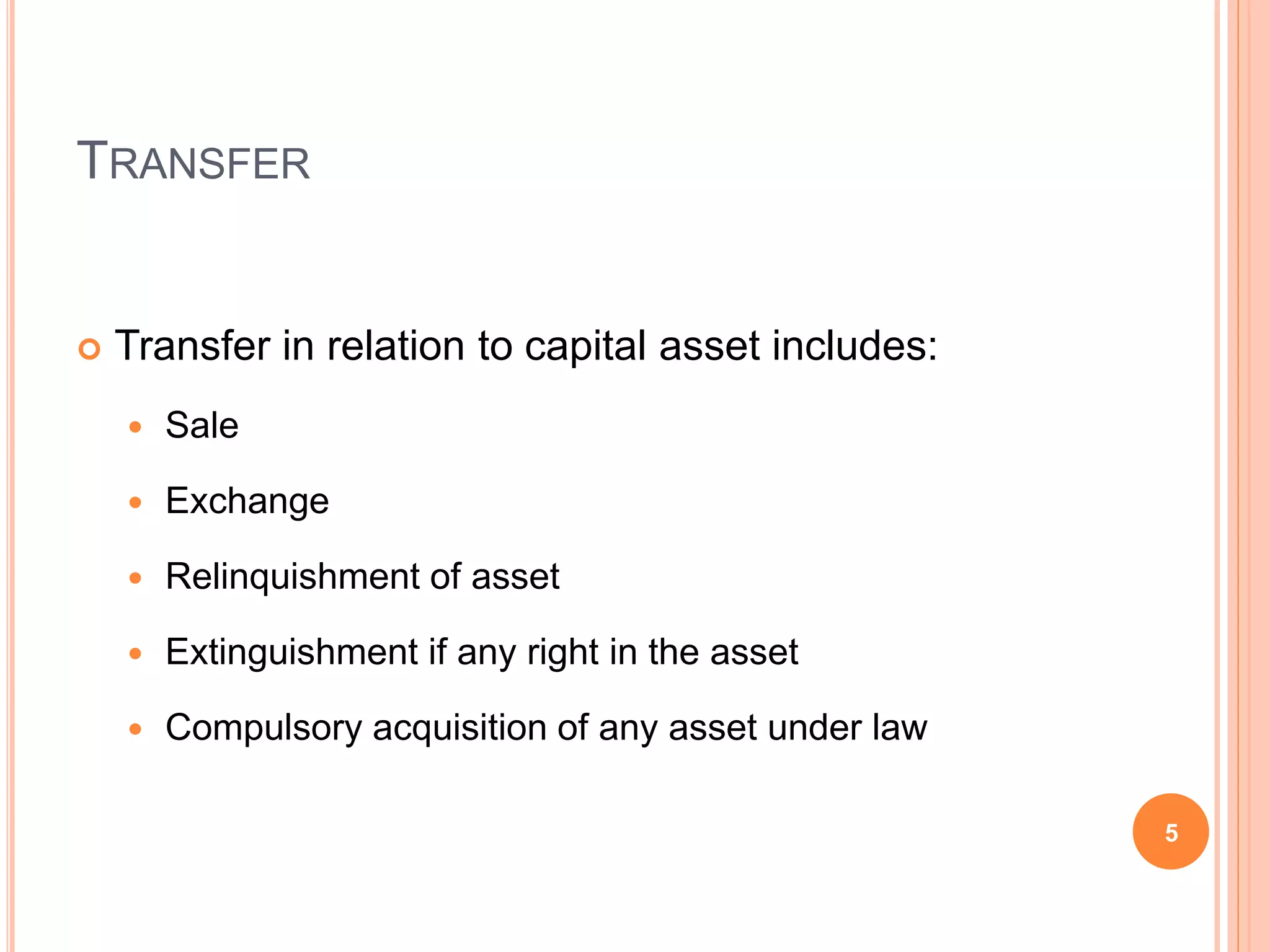

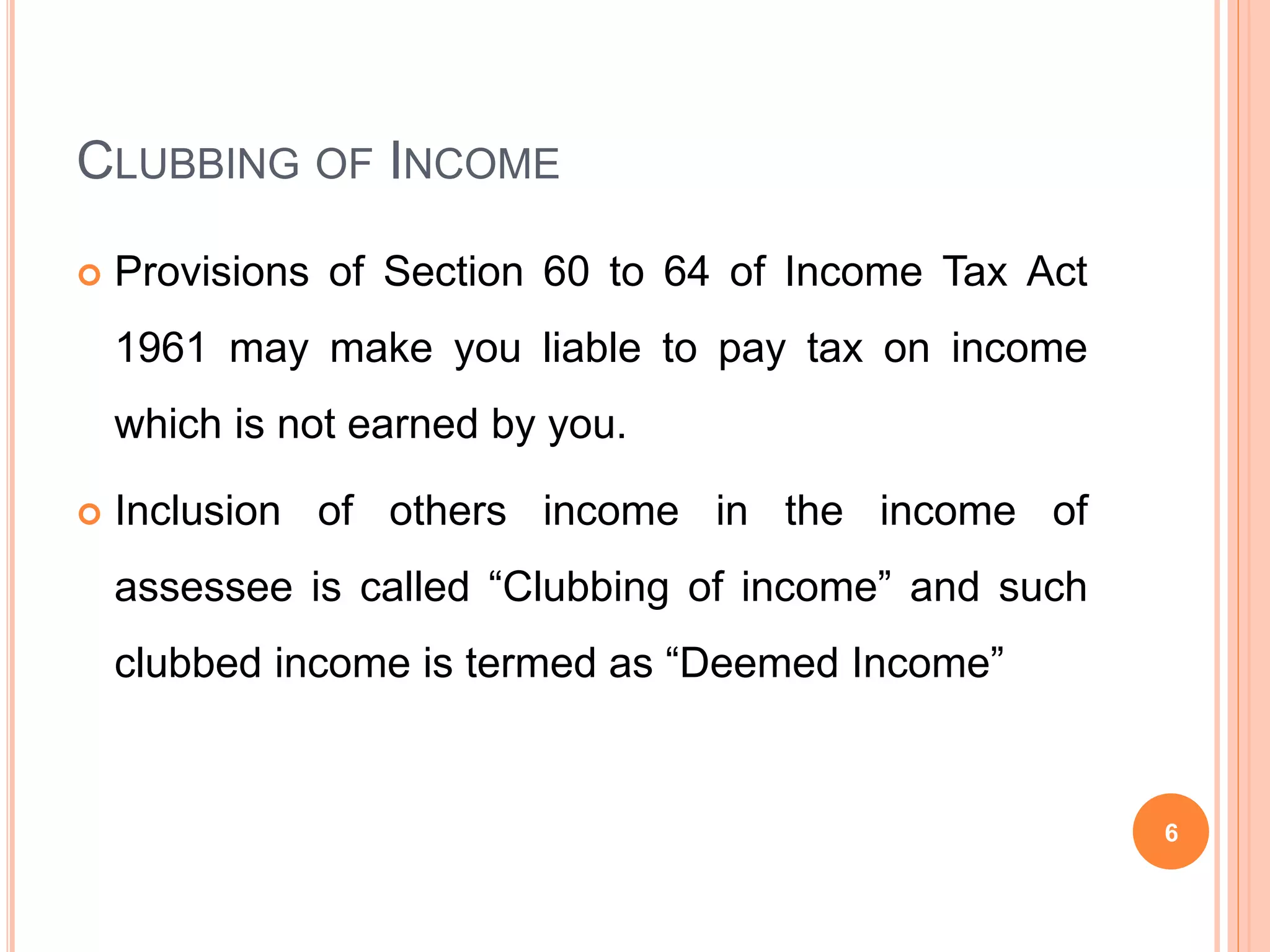

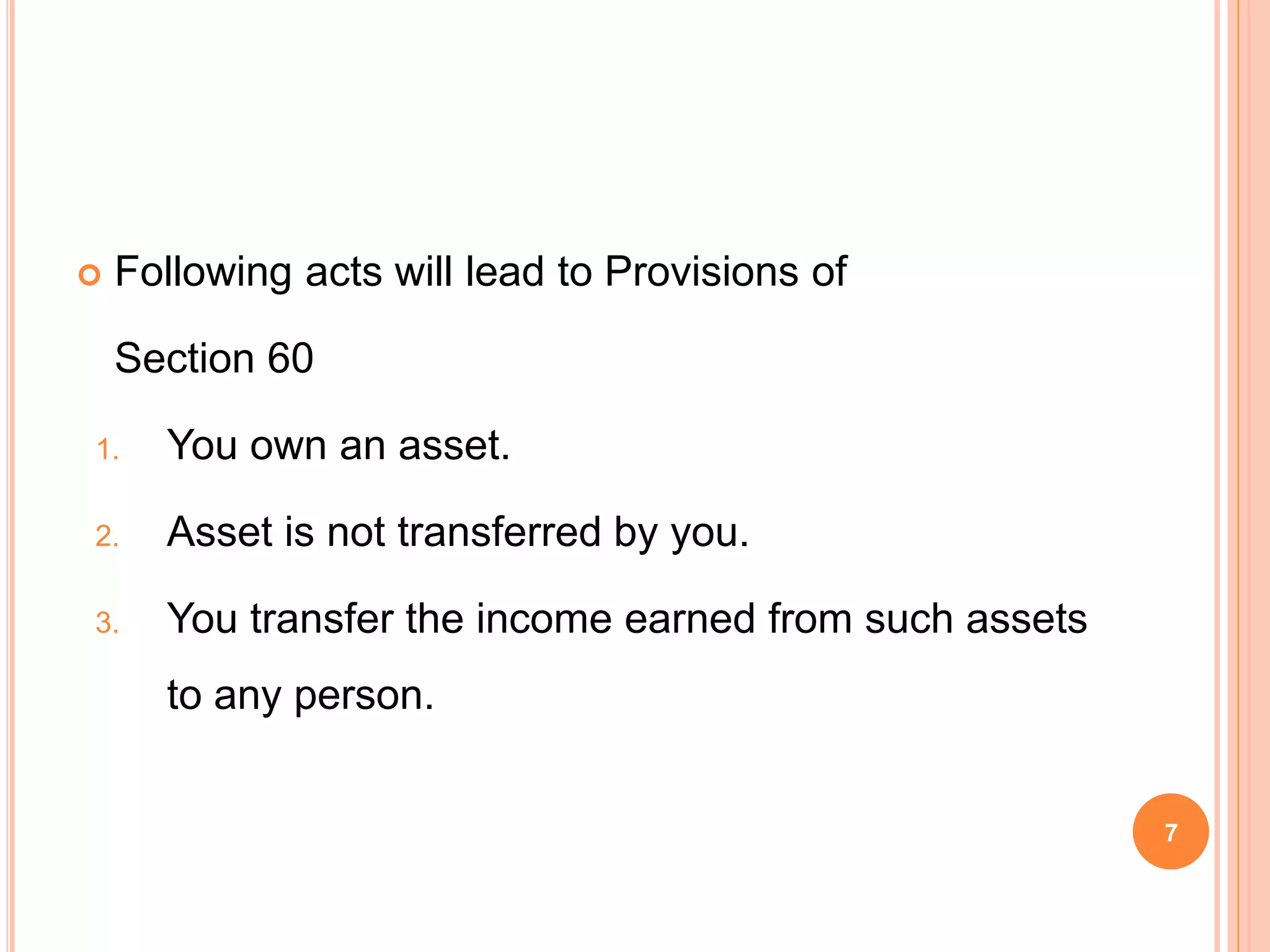

This document defines capital assets and their types, as well as the meaning of transfer and clubbing of income under Indian tax law. It states that capital assets include all movable and immovable properties related to business or not, excluding stock-in-trade. It distinguishes between short-term (36 months or less) and long-term capital assets (36 months or more). Transfer is defined as sale, exchange, relinquishment or compulsory acquisition of an asset. Clubbing of income refers to provisions where a person can be taxed on income not earned by them, such as income transferred from assets they own.