This document is from a chapter in an introduction to managerial accounting textbook. It discusses several key topics:

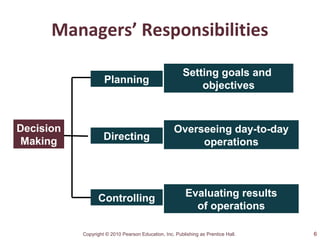

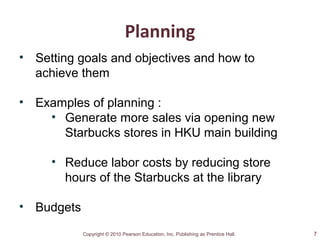

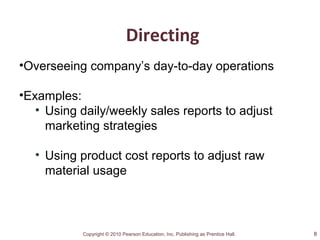

1. It outlines the main responsibilities of managers, which include planning, directing, controlling, decision making, and setting goals and objectives. Examples are provided for each responsibility.

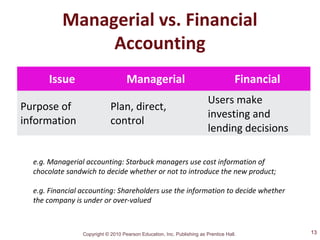

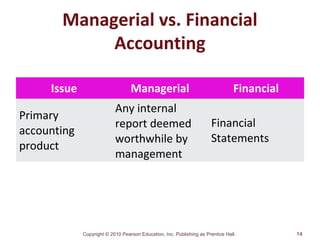

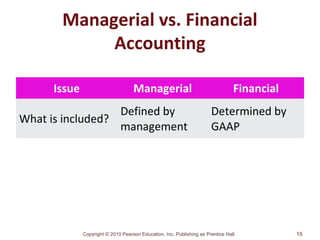

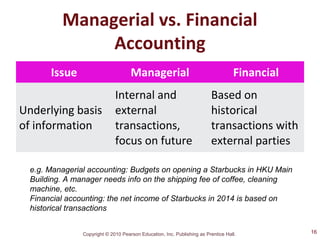

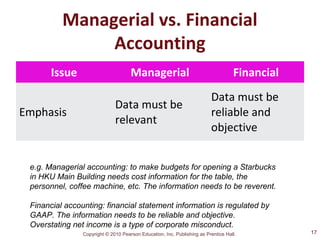

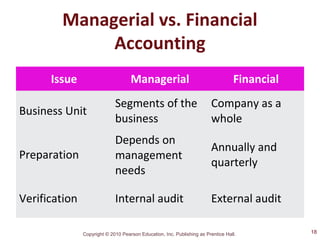

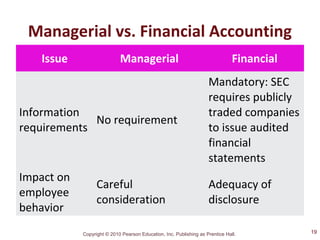

2. It distinguishes between managerial accounting and financial accounting. Managerial accounting focuses on internal reporting for managers, while financial accounting provides external reporting for creditors and shareholders.

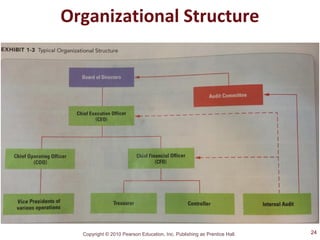

3. It describes typical organizational structures and the changing roles of management accountants, which include ensuring accurate records, analyzing data, and providing decision support. Skills like analytical abilities and communication skills are important for management accountants.

4. It discusses