Downloaded 192 times

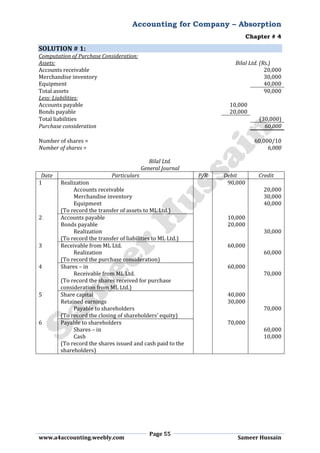

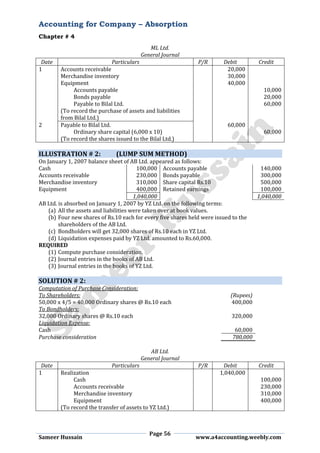

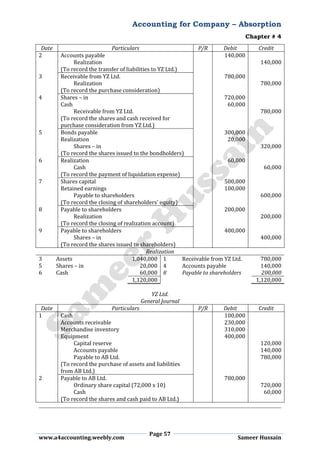

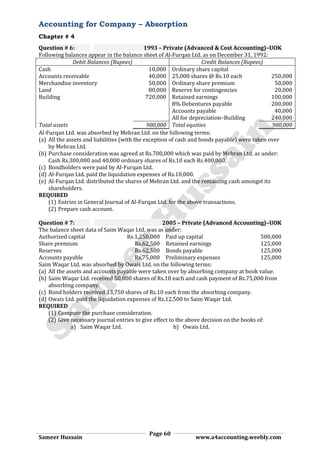

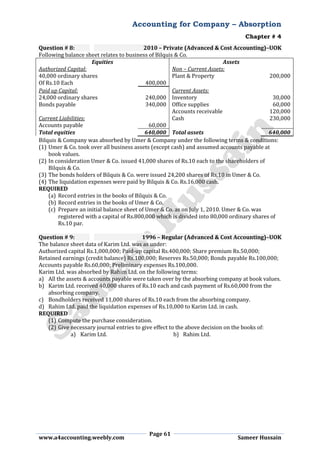

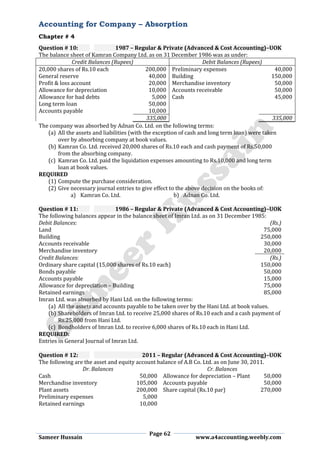

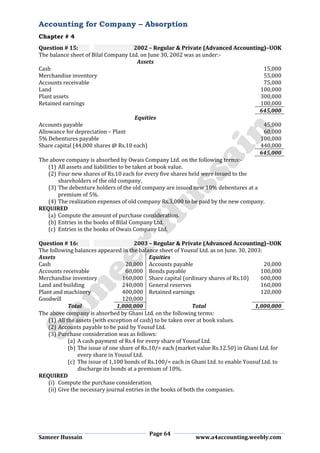

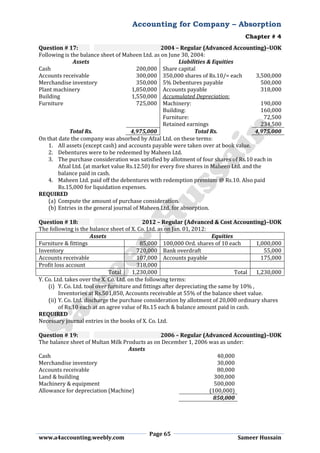

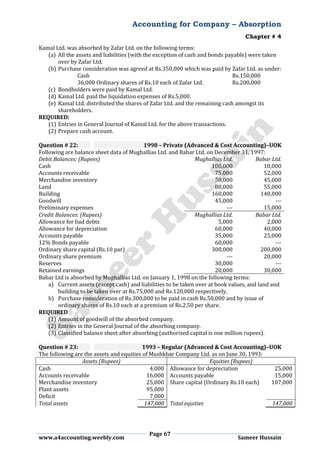

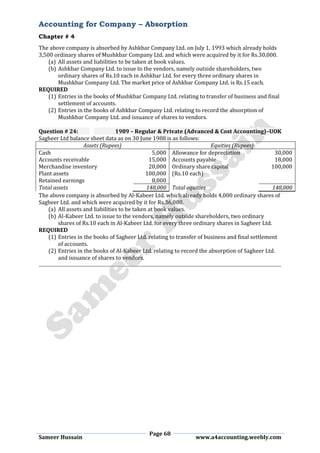

This document provides information about accounting for company absorption. It defines absorption as when one company acquires another and the acquired company ceases to exist while the acquiring company continues. It discusses purchase consideration, which is the amount paid by the new company, and can be calculated via net asset method or lump sum method. It provides journal entries for both the old and new companies, and includes two illustrations applying the concepts to example company mergers.