Downloaded 10 times

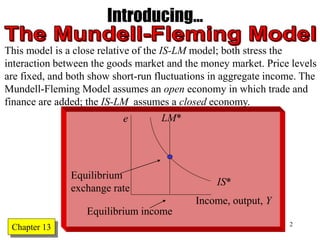

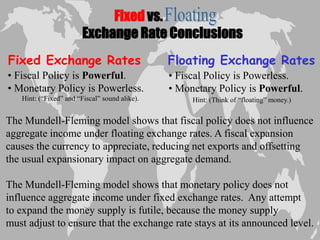

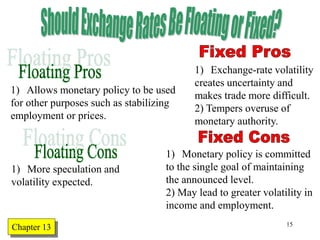

1) The Mundell-Fleming model examines the effects of fiscal and monetary policy in open economies under different exchange rate regimes. 2) Under floating exchange rates, fiscal policy has no effect on output as currency appreciation offsets demand changes, while monetary policy is powerful by changing the exchange rate. 3) Under fixed exchange rates, fiscal policy can boost output as the exchange rate is held constant, but monetary policy has no effect as the money supply adjusts to maintain the fixed rate.