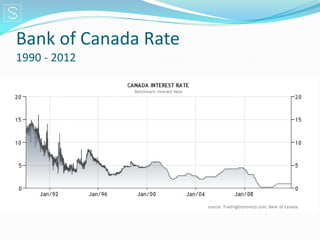

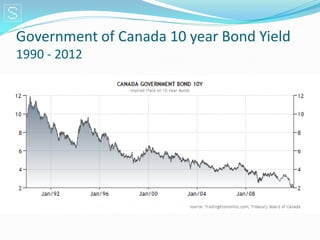

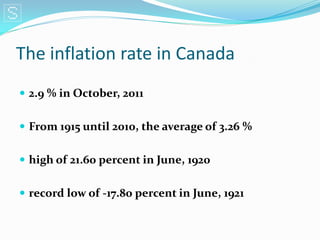

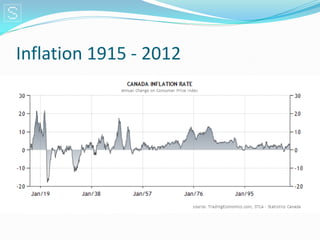

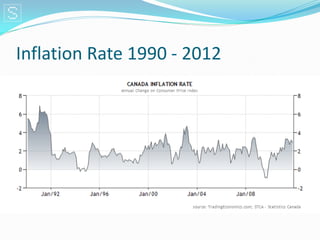

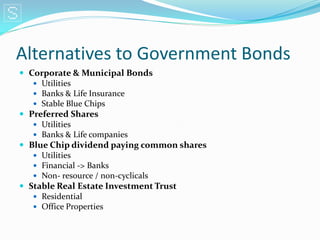

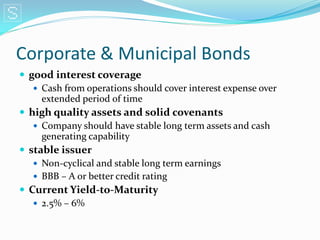

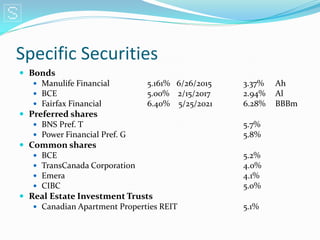

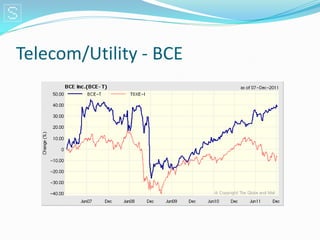

This document discusses alternatives to government bonds for fixed income investments, including corporate and municipal bonds, preferred shares, dividend paying common stocks, and real estate investment trusts. Specific securities are mentioned as examples for each asset class. Non-cyclical sectors like utilities are preferred over more volatile cyclical sectors for reducing portfolio risk. Historical data on interest rates, inflation rates, and bond yields in Canada from 1990-2012 are also presented.