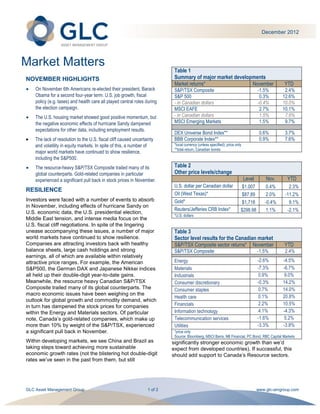

- The document summarizes market developments in November 2012 and year-to-date. It discusses the US presidential election, housing market momentum, and uncertainty around resolving the US fiscal cliff.

- Major world markets showed resilience despite issues like Hurricane Sandy and the fiscal cliff negotiations. Companies attracted investors with strong earnings and balance sheets.

- The resource-heavy Canadian S&P/TSX Composite trailed other markets. Gold-related stocks in particular pulled back, weighing on the Materials and Energy sectors.

- Bond markets offered less volatility than equities but low yields meant little return beyond historically low levels. Uncertainty around resolving the fiscal cliff increased volatility into the end of the year.