The document summarizes the key topics that were to be covered in a mortgage 101 seminar presented by Crawford & Associates, including:

- How to find the right lender and mortgage, different types of mortgages and terms, and requirements for conforming vs. alternative lenders.

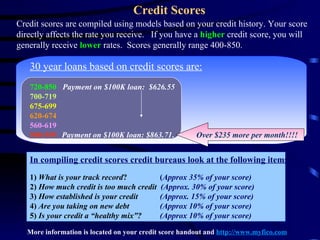

- Factors that affect credit worthiness and credit scores, which directly impact approved loan amounts and interest rates.

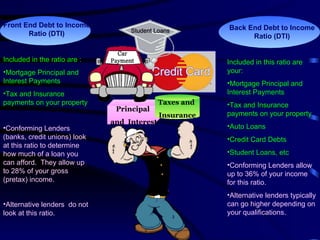

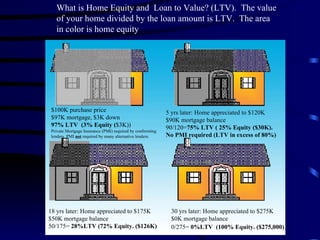

- Key considerations like income, debt ratios, appraisals, loan-to-value ratios, taxes, insurance, responsibilities of borrowers, and payment options.

![The Crawford & Associates Dwight Crawford, C.M.C. LLO 704-542-7937 [email_address]](https://image.slidesharecdn.com/crawfordandassociatesseminar-12499677339396-phpapp03/85/Crawford-And-Associates-Mortgage-101Seminar-14-320.jpg)