Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

Company Valuation webinar series - Tuesday, 4 June 2024FelixPerez547899

This session provided an update as to the latest valuation data in the UK and then delved into a discussion on the upcoming election and the impacts on valuation. We finished, as always with a Q&A

Improving profitability for small businessBen Wann

In this comprehensive presentation, we will explore strategies and practical tips for enhancing profitability in small businesses. Tailored to meet the unique challenges faced by small enterprises, this session covers various aspects that directly impact the bottom line. Attendees will learn how to optimize operational efficiency, manage expenses, and increase revenue through innovative marketing and customer engagement techniques.

RMD24 | Debunking the non-endemic revenue myth Marvin Vacquier Droop | First ...BBPMedia1

Marvin neemt je in deze presentatie mee in de voordelen van non-endemic advertising op retail media netwerken. Hij brengt ook de uitdagingen in beeld die de markt op dit moment heeft op het gebied van retail media voor niet-leveranciers.

Retail media wordt gezien als het nieuwe advertising-medium en ook mediabureaus richten massaal retail media-afdelingen op. Merken die niet in de betreffende winkel liggen staan ook nog niet in de rij om op de retail media netwerken te adverteren. Marvin belicht de uitdagingen die er zijn om echt aansluiting te vinden op die markt van non-endemic advertising.

Discover the innovative and creative projects that highlight my journey throu...dylandmeas

Discover the innovative and creative projects that highlight my journey through Full Sail University. Below, you’ll find a collection of my work showcasing my skills and expertise in digital marketing, event planning, and media production.

Kseniya Leshchenko: Shared development support service model as the way to ma...Lviv Startup Club

Kseniya Leshchenko: Shared development support service model as the way to make small projects with small budgets profitable for the company (UA)

Kyiv PMDay 2024 Summer

Website – www.pmday.org

Youtube – https://www.youtube.com/startuplviv

FB – https://www.facebook.com/pmdayconference

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

At Techbox Square, in Singapore, we're not just creative web designers and developers, we're the driving force behind your brand identity. Contact us today.

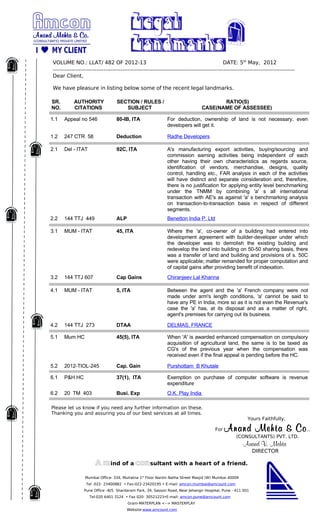

1. VOLUME NO.: LLAT/ 482 OF 2012-13 DATE: 5th May, 2012

Dear Client,

We have pleasure in listing below some of the recent legal landmarks.

SR. AUTHORITY SECTION / RULES / RATIO(S)

NO. CITATIONS SUBJECT CASE(NAME OF ASSESSEE)

1.1 Appeal no 546 80-IB, ITA For deduction, ownership of land is not necessary, even

developers will get it.

1.2 247 CTR 58 Deduction Radhe Developers

2.1 Del - ITAT 92C, ITA A's manufacturing export activities, buying/sourcing and

commission earning activities being independent of each

other having their own characteristics as regards source,

identification of vendors, merchandise, designs, quality

control, handling etc., FAR analysis in each of the activities

will have distinct and separate consideration and, therefore,

there is no justification for applying entity level benchmarking

under the TNMM by combining 'a' s all international

transaction with AE's as against 'a' s benchmarking analysis

on transaction-to-transaction basis in respect of different

segments.

2.2 144 TTJ 449 ALP Benetton India P. Ltd

3.1 MUM - ITAT 45, ITA Where the 'a', co-owner of a building had entered into

development agreement with builder-developer under which

the developer was to demolish the existing building and

redevelop the land into building on 50-50 sharing basis, there

was a transfer of land and building and provisions of s. 50C

were applicable; matter remanded for proper computation and

of capital gains after providing benefit of indexation.

3.2 144 TTJ 607 Cap Gains Chiranjeev Lal Khanna

4.1 MUM - ITAT 5, ITA Between the agent and the 'a' French company were not

made under arm's length conditions, 'a' cannot be said to

have any PE in India, more so as it is not even the Revenue's

case the 'a' has, at its disposal and as a matter of right,

agent's premises for carrying out its business.

4.2 144 TTJ 273 DTAA DELMAS, FRANCE

5.1 Mum HC 45(5), ITA When 'A' is awarded enhanced compensation on compulsory

acquisition of agricultural land, the same is to be taxed as

CG's of the previous year when the compensation was

received even if the final appeal is pending before the HC.

5.2 2012-TIOL-245 Cap. Gain Purshottam B Khutale

6.1 P&H HC 37(1), ITA Exemption on purchase of computer software is revenue

expenditure

6.2 20 TM 403 Busi. Exp O.K. Play India

Please let us know if you need any further information on these.

Thanking you and assuring you of our best services at all times.

Yours Faithfully,

For Anand Mehta & Co .,

(CONSULTANTS) PVT. LTD.

Anand V. Mehta

DIRECTOR

A mind of a consultant with a heart of a friend.

Mumbai Office- 334, Mulratna 1st Floor Narshi Natha Street Masjid (W) Mumbai 40009

Tel -022- 23400882 • Fax-022-23420195 • E-mail: amcon.mumbai@amcount.com

Pune Office –B/5 Shardaram Park, 34, Sasson Road, Near Jehangir Hospital, Pune - 411 001

Tel-020 6401 3124 • Fax 020- 30521223•E-mail: amcon.pune@amcount.com

Gram-MATERPLAN <--> MASTERPLAY

Website:www.amcount.com