Uneak White's Personal Brand Exploration Presentation

LL 457

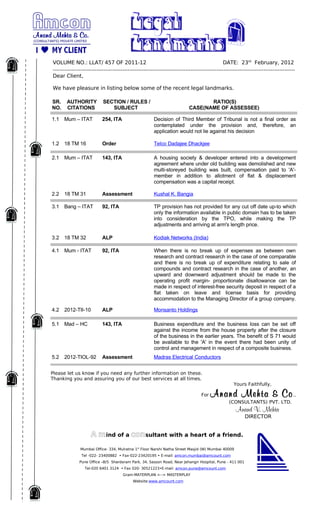

1. VOLUME NO.: LLAT/ 457 OF 2011-12 DATE: 23rd February, 2012

Dear Client,

We have pleasure in listing below some of the recent legal landmarks.

SR. AUTHORITY SECTION / RULES / RATIO(S)

NO. CITATIONS SUBJECT CASE(NAME OF ASSESSEE)

1.1 Mum – ITAT 254, ITA Decision of Third Member of Tribunal is not a final order as

contemplated under the provision and, therefore, an

application would not lie against his decision

1.2 18 TM 16 Order Telco Dadajee Dhackjee

2.1 Mum – ITAT 143, ITA A housing society & developer entered into a development

agreement where under old building was demolished and new

multi-storeyed building was built, compensation paid to 'A'-

member in addition to allotment of flat & displacement

compensation was a capital receipt.

2.2 18 TM 31 Assessment Kushal K. Bangia

3.1 Bang – ITAT 92, ITA TP provision has not provided for any cut off date up-to which

only the information available in public domain has to be taken

into consideration by the TPO, while making the TP

adjustments and arriving at arm's length price.

3.2 18 TM 32 ALP Kodiak Networks (India)

4.1 Mum - ITAT 92, ITA When there is no break up of expenses as between own

research and contract research in the case of one comparable

and there is no break up of expenditure relating to sale of

compounds and contract research in the case of another, an

upward and downward adjustment should be made to the

operating profit margin- proportionate disallowance can be

made in respect of interest-free security deposit in respect of a

flat taken on leave and license basis for providing

accommodation to the Managing Director of a group company.

4.2 2012-TII-10 ALP Monsanto Holdings

5.1 Mad – HC 143, ITA Business expenditure and the business loss can be set off

against the income from the house property after the closure

of the business in the earlier years. The benefit of S 71 would

be available to the 'A' in the event there had been unity of

control and management in respect of a composite business.

5.2 2012-TIOL-92 Assessment Madras Electrical Conductors

Please let us know if you need any further information on these.

Thanking you and assuring you of our best services at all times.

Yours Faithfully,

For Anand Mehta & Co .,

(CONSULTANTS) PVT. LTD.

Anand V. Mehta

DIRECTOR

A mind of a consultant with a heart of a friend.

Mumbai Office- 334, Mulratna 1st Floor Narshi Natha Street Masjid (W) Mumbai 40009

Tel -022- 23400882 • Fax-022-23420195 • E-mail: amcon.mumbai@amcount.com

Pune Office –B/5 Shardaram Park, 34, Sasson Road, Near Jehangir Hospital, Pune - 411 001

Tel-020 6401 3124 • Fax 020- 30521223•E-mail: amcon.pune@amcount.com

Gram-MATERPLAN <--> MASTERPLAY

Website:www.amcount.com