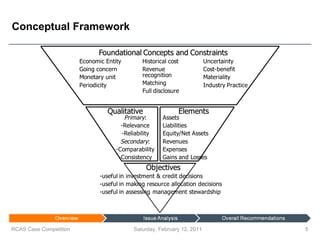

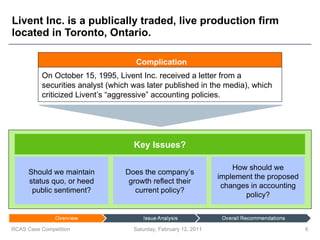

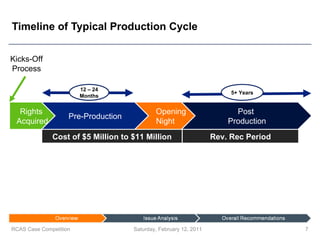

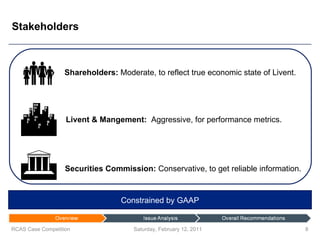

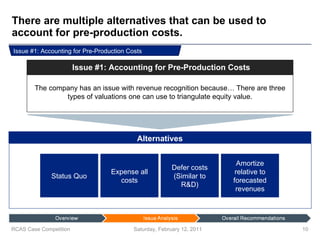

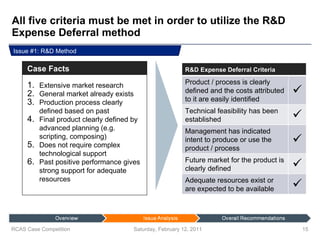

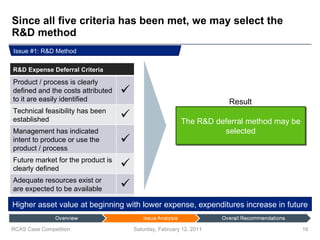

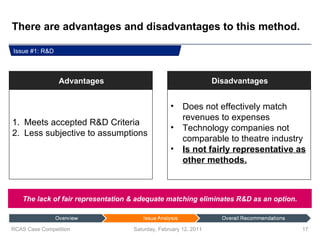

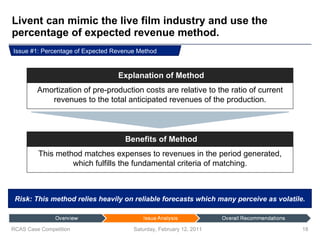

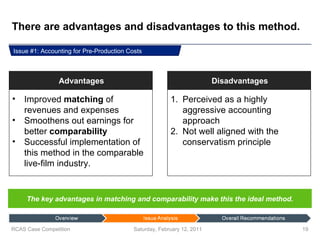

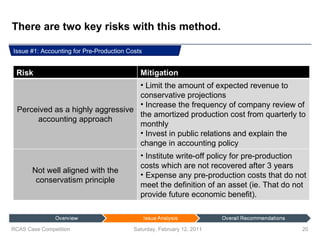

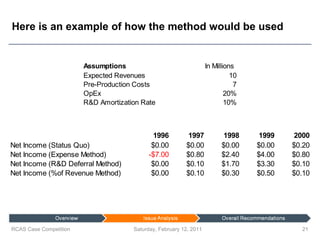

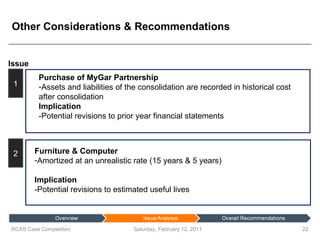

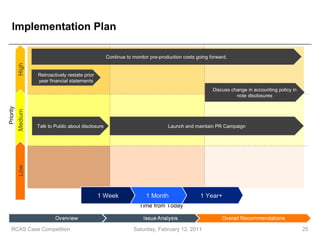

The document summarizes a meeting where an audit committee discussed how a production company, Livent Inc., should account for pre-production costs according to Canadian GAAP. The committee analyzed expensing all costs, deferring costs similar to R&D, and amortizing costs relative to forecasted revenues. They determined amortizing costs relative to revenues best matches expenses to revenues earned. They recommend this method and discuss implementing it through disclosure, conservative forecasts, and write-offs for unrecovered costs.