More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to LGIP FY13 Q1 pt2

Similar to LGIP FY13 Q1 pt2 (20)

More from dougducey

LGIP FY13 Q1 pt2

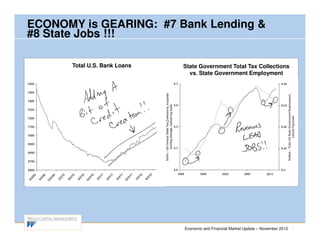

- 1. ECONOMY is GEARING: #7 Bank Lending & #8 State Jobs !!! Total U.S. Bank Loans State Government Total Tax Collections vs. State Government Employment Economic and Financial Market Update – November 2012

- 2. ECONOMY is GEARING: #9 Net Exports!!! U. S. Real Exports vs. Real Imports U. S. REAL Broad Trade-Weighted Dollar Index Economic and Financial Market Update – November 2012

- 3. ECONOMY is GEARING: #10 Sensitivity to Crises!! CBOE VIX VOLATILITY Index Bloomberg European Financial Conditions Index Economic and Financial Market Update – November 2012

- 4. U.S. Economy is Self-Medicating!!! 30-Year National Average Annual Growth in the M2 Trade-Weighted U.S. Mortgage Interest Rate Money Supply Dollar Index Commodity Prices Total Annualized U.S. Annual Consumer Price Crude Oil vs. Non-Energy Commodities Auto Sales Inflation Rate Economic and Financial Market Update – November 2012

- 5. SAME Demographic New-NORMAL Hits Entire G-10!?? G-10* Global REAL GDP *Includes Canada, Sweden, Switzerland, U.K., Japan, U.S., Italy, France, Germany & Australia Economic and Financial Market Update – November 2012

- 6. Fortunately, the U.S. Enacted the Emerging Market MARSHALL PLAN!!! Percent of Nominal Global GDP (in U.S. Dollars) Comprised by Economies EXCLUDING the G-10 Economies Economic and Financial Market Update – November 2012

- 7. GLOBAL GROWTH IS STILL O.K.?!? Global REAL GDP G-10 Economies vs. Rest of Global Economy Economic and Financial Market Update – November 2012

- 8. What? Real Global Growth Has Accelerated??? Real Global World Product Annualized Real Gross World Product 2011 U.S. Dollars, natural log scale Growth by Decade* Note: The 00s decade is the annualized growth for 11 years from 2000 to 2011 Economic and Financial Market Update – November 2012

- 9. Finding Top-LINE GROWTH?!? S&P 400 Real Sales Per Share** vs. U.S. S&P 400 Nominal Sales Per Share vs. Real GDP U.S. Nominal GDP Annualized Growth by Decade* Annualized Growth by Decade* ** S&P 400 Sales Per Share Adjusted by GDP Price Deflator Index * The 2000s decade is actually from 1999Q4 to 2012Q2 * The 2000s decade is actually from 1999Q4 to 2012Q2 Economic and Financial Market Update – November 2012

- 10. Earnings Story Is Not Just Margins!!? Annual Growth in S&P 400 Sales per Share Large Cap (S&P 500) vs. Small Cap (Russell 2000) Per Share Annual Sales Growth Economic and Financial Market Update – November 2012

- 11. What About Europe??? Solution is Growth … Not Austerity Finally, an “Economic Union” Moving Euro zone from “Imminent Calamity” to “Chronic Problem” Fallout is Slower/No Growth from Euro zone “Financial” Contagion Unlikely In 1990, Global Recovery Proceeded Without Japan Investor Sensitivity is Decaying Economic and Financial Market Update – November 2012

- 12. What About CHINA??? China Leading Economic Index vs. China Leading Economic Index vs. Short-Term Policy Interest Rate** Real Annual M2 Money Growth* ** China CHIBOR 3 month interest rate (six month moving average) NOTE: Annual Real Money Growth (dotted line) Until 7/2002 and China SHIBOR 3 month interest rate thereafter. LEADING by Six Months NOTE: Interest Rate LEADS by One Year Economic and Financial Market Update – November 2012

- 13. Inflation Story?? Unstoppable Forces Meet Immovable Objects!?! Inflation Forces Deflation Forces Massive Newly-Developing Demand Force 30-Year Disinflationary Culture Excess Liquidity Everywhere Tech-Induced Productivity Surge Monetary /Fiscal Overkill New-found Global Competition Pent-Up Demands Impaired Balance Sheets Improving Balance Sheets Resource/Potential GDP Slack Government Solutions Economic and Financial Market Update – November 2012

- 14. Time to Start Normalizing Monetary Policy!!?! Nominal GDP Growth vs. Money Supply Growth* Fed Funds Rate vs. Business Bank Loans *3-Year Trailing annualized growth rates. GDP is GNP until 1946. Money Supply is M1 through 1958 and M2 thereafter. Economic and Financial Market Update – November 2012

- 15. Fed Needs to Get Beyond its Crisis Mindset???! Effective Federal Funds U.S. Excess Bank Reserves Interest Rate Trillions U.S. Dollars Economic and Financial Market Update – November 2012

- 16. Oil? Supply Catching Demand??? Baker Hughes U.S. Crude Oil Rig Count Economic and Financial Market Update – November 2012

- 17. What Oil Crisis??? U.S. Oil Production (Mil. Barrels per day) U.S. Net Imports Crude Oil (Mil. Barrels per day) 2011 7.84 2011 8.48 Economic and Financial Market Update – November 2012

- 18. So … You Like Gold, Huh??!? Price of S&P 500 Stock Index in Ounces of Gold* Price of Gold Relative to U.S. Treasury Bond* Price of Gold Relative to U.S. House Price* *Relative Price of S&P 500 divided by Price of Gold. *Price of gold divided by Long-term U.S. Treasury *Price of gold divided by U.S. House Price Number of Ounces of gold it takes to purchase the Bond Prices. Bond Price set at $100 in December Index. House Price Index is based on the S&P 500 Stock Price Index. 1962 and then rose or fell each month based on Median New Home Sales Price Index until Ibbotson’s estimate of price-only return. March 1987 and the Case-Shiller National U.S. House Price Index thereafter. Price of Gold Relative to Overall Number of Hours of Work Required to Price of Gold Relative to Consumer Price Index Commodity Prices* Purchase an Ounce of Gold* Basket of Consumer Goods and Services *Price of Gold divided by S&P GSCI Spot *Price of Gold Price divided by the Average Commodity Price Index. Hourly Earnings Index. Economic and Financial Market Update – November 2012

- 19. Will Bonds Be Bloodied??? Real 10-Year Treasury Bond Yield* *10-Year Treasury Bond Yield Less Annual Core Consumer Price Inflation Rate 9 8 7 6 5 4 3 2 1 0 -1 -2 -3 -4 -5 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 Economic and Financial Market Update – November 2012

- 20. FEAR Has Been Bond Market’s Best Friend!!? Real Treasury Bond Yield and CONFIDENCE Economic and Financial Market Update – November 2012

- 21. AGING Demographics & the Bond Market?!? U.S. 10-Year Treasury Bond Yield vs. U.S. Labor Force Growth Economic and Financial Market Update – November 2012

- 22. U.S. Deficit… More Cyclical Than Structural?!?! U.S. Federal Deficit/GDP Ratio vs. Detrended Real GDP* *Detrended by 1965 to 1984 average annualized growth of 3.25% and by 1985 to 2012 average annualized growth of 2.6%. Economic and Financial Market Update – November 2012

- 23. Huh…. Best Post-Recession Stock Market Rally Ever???! Post-War Stock Market Rallies Post-War Stock Market Rallies Cumulative Price-Only Percent Returns Cumulative Percent Price Only Return From Recession from Recession Low Low During First 870 Days NOTE: BOLD Line is the Current Recovery Stock Market Rally Economic and Financial Market Update – November 2012

- 24. Conference Boards Consumer Confidence Index (Solid) Confidence and Real Treasury Bond Yield “DOA” Sectors LEAD Stock MARKET!?! Real 10-Year Treasury Bond Yield Year (10-year yield less core consumer price inflation rate) year (Dotted) Economic and Financial Market Update – November 2012

- 25. IF INFLATION STAYS LOW…LOTS OF VALUATION ROOM!?! U.S. Stock Market Environmental PE Valuation* *Sum of PE ratio (based on trailing 12-month eps), 10-yr Treasury bond yield and Annual CPI Inflation Rate Economic and Financial Market Update – November 2012

- 26. POST-WAR STOCK MARKET STORY!??! U.S. Stock Market vs. Long-Term Trendline Level Total U.S. Corporate Profits S&P 500 Stock Price Index (Solid) Actual Level (Solid) vs. Trendline (Dotted) Trendline Level (Dotted) Economic and Financial Market Update – November 2012

- 27. CULTURAL “GLOOM TO GLEE” CYCLE!!? U.S. Stock Market Percent Above/Below Long-Term Trendline Economic and Financial Market Update – November 2012

- 28. Could A Return To “NORMAL CONFIDENCE” Double the Stock Market??? Detrended U.S. Stock Market vs. U.S. Consumer Confidence Economic and Financial Market Update – November 2012

- 29. Mania to Mania!!? New-Era → Mania of OPTIMISM New-Normal → Mania of PESSIMISM Economic and Financial Market Update – November 2012

- 30. A “Confidence-Driven” Secular Bull à la 1950s- 60s!??! U.S. Stock Market vs. Long-Term Bond Yields* *Sources: Robert Schiller’s database, Bloomberg. Natural Log Scale (Dotted) Natural Log Scale (Solid) Long-Term Bond Yield* U.S. Stock Market* Term Economic and Financial Market Update – November 2012

- 31. Stay With Cyclical Stocks?!? Unemployment Claims vs. Stable/Cyclical Relative Stock Price Performance* *Geo-weighted index of stable S&P 500 sectors (consumer staples, health care, and utilities) relative to index of S&P 500 cyclical sectors (consumer discretionary, industrials, and materials). Relative stock price performance of S&P 500 stable vs. cyclical sectors* Unemployment Insurance Claims Moving Average of Initial Natural Log Scale (Solid) Natural Log Scale (Dotted) 4-Week Week Economic and Financial Market Update – November 2012

- 32. Wait for the Flow!!!? Net New Monthly Mutual Fund Cash Flows Stock Funds Less Bond Funds* vs. Relative Price Performance of Stocks Over Bonds *3-Month Moving Average of Monthly Flows Economic and Financial Market Update – November 2012

- 33. BUY & “HOLD YOUR NOSE” !!?? Rolling 10-Year Standard Deviations of Dow Jones Industrial Average – 1900 to 2012 Daily Percent Stock Market Changes Shown on a Natural Log Scale Economic and Financial Market Update – November 2012

- 34. A Lost Decade?? Hardly!!! Emerging World Economies’ Real Corporate Profit Per Job* Nominal U.S. Dollar GDP *Total U.S. corporate profits adjusted for Percent of U.S. Nominal GDP GDP deflator inflation index and divided by 2000 vs. 2010 nonfarm private payrolls. Shown on a natural log scale. Real U.S. Wage Rate* *U.S. average hourly earnings index divided by consumer price index. Shown on a natural log scale. Inflation-Adjusted Total Global GDP Real U.S. Dollars Economic and Financial Market Update – November 2012

- 35. 2012-2013 Possibilities??? U.S. Economy has a “GEAR YEAR” Real GDP Rises by 3%ish U.R. Exhibits “Slow but Steady” Decline H.H. & Biz Confidence Improve Housing Market “Pops” a Little Biz Spend Some of $2 Trillion Cash Hoard Euro Crisis Mutates from “Imminent Calamity” to “Chronic Problem” Emerging World Soft Landing… Accelerates in 2nd Half U.S. Politics Moves to a “Happier Middle” Talk of a “New All-Time” Stock Market High T-Bond Market Gets Drilled Economic and Financial Market Update – November 2012

- 36. Questions? Wells Capital Management (WellsCap) is a registered investment adviser and a wholly owned subsidiary of Wells Fargo Bank, N.A. WellsCap provides investment management services for a variety of institutions. The views expressed are those of the author at the time of writing and are subject to change. This material has been distributed for educational/informational purposes only, and should not be considered as investment advice or a recommendation for any particular security, strategy, or investment product. The material is based upon information we consider reliable, but its accuracy and completeness cannot be guaranteed. Past performance is not a guarantee of future returns. As with any investment vehicle, there is a potential for profit as well as the possibility of loss. For additional information on Wells Capital Management and its advisory services, please view our web site at www.wellscap.com, or refer to our Form ADV Part II, which is available upon request by calling 415.396.8000. WELLS CAPITAL MANAGEMENT® is a registered service mark of Wells Capital Management, Inc. Economic and Financial Market Update – November 2012

- 37. QUESTIONS? OFFICE OF THE ARIZONA STATE TREASURER