Download to read offline

![EDF Trading Derivatives Desk

Definitions and Basic Assumptions

Lt is a Levy process if L0 = 0 and has independent and stationary increments, and it’s

continuous in probability

∀t ≥ 0, ∀ε > 0, lims→t (|Lt − Ls| > 0) = 0

The Fourier transform of Lt follows Levy-Khintchine formula :

[ezLt] = etψ(z)

∀z ∈ , ψ(z) = imz −

σ2

2

z2 + (eizu − 1 − iuz)ν(du)

• The measure ν(dx) is called the Levy mesur of Lt

• Levy process consists of three independent parts

O. Senhadji El Rhazi 6 August 06, 2005](https://image.slidesharecdn.com/levyprocessesintheenergymarkets-170629135106/85/Levy-processes-in-the-energy-markets-7-320.jpg)

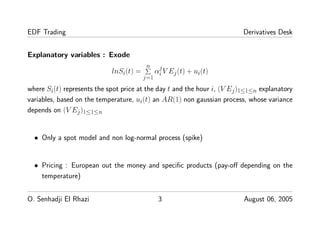

![EDF Trading Derivatives Desk

Asset Price Model 2

Assume F(t, T) the forward price at time t with delivery at time T, which we model as

stochastic process

F(t, T) = Λ(t, T)eXT

t

Using the condition of arbitrage-free price of forward, the market price of risk ω, we

postulate the model (under ) :

Λ(t, T) = F(0, T)exp( t

0 [ϕ(ω + σe−a(T−s)) − ϕ(ω)]ds)

XT

t = t

0 σe−a(T−s)dLs

O. Senhadji El Rhazi 9 August 06, 2005](https://image.slidesharecdn.com/levyprocessesintheenergymarkets-170629135106/85/Levy-processes-in-the-energy-markets-10-320.jpg)

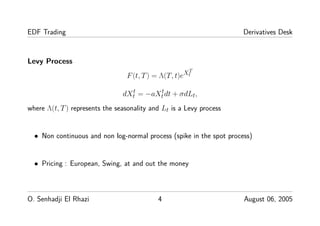

![EDF Trading Derivatives Desk

Asset Price Model 3

F(t, T) = Λ(T, t)eXT

t

• Mean-reversion :

dXt

t = −aXt

tdt + σdLt

• Seasonal variations :

Λ(t, T) = F(0, T)exp( t

0 [ϕ(ω + σe−a(T−s)) − ϕ(ω)]ds)

• Leptokurtic log-spot :

Lt and not Wt

O. Senhadji El Rhazi 10 August 06, 2005](https://image.slidesharecdn.com/levyprocessesintheenergymarkets-170629135106/85/Levy-processes-in-the-energy-markets-11-320.jpg)

![EDF Trading Derivatives Desk

Asset Price Model 4

We denote Yt = ln( St

F(0,t)), this process is a solution of the SDE given by

dYt = a(mt − Yt)dt + σdLt

mt = −

1

a

[ϕ(ω + σe−at) − ϕ(ω)] − t

0 [ϕ(ω + σe−as) − ϕ(ω)]ds

We consider discretisation of an interval [0, T], with step h = T

n. We denote Yih = Yi

which follows the following schema :

Yi − φ1Yi−1 − φi

0 = εi

with,

εi = ih

(i−1)h σe−a(ih−s)dLs, φ1 = e−ah

O. Senhadji El Rhazi 11 August 06, 2005](https://image.slidesharecdn.com/levyprocessesintheenergymarkets-170629135106/85/Levy-processes-in-the-energy-markets-12-320.jpg)

![EDF Trading Derivatives Desk

and,

φi

0 = − ih

0 [ϕ(ω + σe−as) − ϕ(ω)]ds + φ1

(i−1)h

0 [ϕ(ω + σe−as) − ϕ(ω)]ds

εi are i.i.d if ah ≪ 1, we can make this approximation :

εi ∼ σLh

• With conjugate gradient or maximum likelihood methods, we can estimate the pa-

rameters of the model Lt.

O. Senhadji El Rhazi 12 August 06, 2005](https://image.slidesharecdn.com/levyprocessesintheenergymarkets-170629135106/85/Levy-processes-in-the-energy-markets-13-320.jpg)

![EDF Trading Derivatives Desk

Subordination

The class of HG distribution can be obtained by subordination of the Brownian time, if

we define

Lt = µt + βτt + Wτt

where Wt is a standard Brownian motion and τt (business time) is generated by a GIG(λ, δ, γ),

which has the following distribution

fGIG

(x) = (

γ

δ

)λ 1

2Kλ(δγ)

xλ−1

exp(−

1

2

(

δ2

x

+ γ2

x))

✒ Period of agitation τt+dt − τt > dt, ar[Wτt+dt

|τt+dt] > ar[Wτt

|τt] + ar[Wτdt

]

✒ Period of calm τt+dt − τt ≤ dt, ar[Wτt+dt

|τt+dt] ≤ ar[Wτt

|τt] + ar[Wτdt

]

The process Lt can be seen as a stochastic volatility model.

O. Senhadji El Rhazi 18 August 06, 2005](https://image.slidesharecdn.com/levyprocessesintheenergymarkets-170629135106/85/Levy-processes-in-the-energy-markets-19-320.jpg)

![EDF Trading Derivatives Desk

Bibliographie

[BEHN99] F.E.Benth, L.Ekeland, R.Hauge, B.F.Nielsen , On arbitrage-free pricing of forward contracts in

energy markets, Preprint, pp. 1-7, (2001).

[CM99] P.Carr and D.B.Madan, Option Valuation Using the Fast Fourier Transform, J.Comp Finance, pp.

61-73, (1999).

[CS00] L.Clewlow and C.Strickland, Energy Derivatives. Pricing and Risk Management, Lacima Publications,

(2000).

[ML02] V.Mignon et S.Lardic, Econométrie des séries temporelles macroéconomiques et financières, Eco-

nomica, pp. 45, 274, 25-52, (2002).

[Rai00] S.Raible, Levy Processes in Finance : Theory, Numerics, and Empirical Facts, PhD thesis, Institut

für Mathematische Stochastik, Universität Freiburg im Breisgau, (2000).

[Sch03] W.Schoutens, Levy Processes in Finance : Pricing Financial Derivatives, Wiley Publications, (2003).

O. Senhadji El Rhazi 21 August 06, 2005](https://image.slidesharecdn.com/levyprocessesintheenergymarkets-170629135106/85/Levy-processes-in-the-energy-markets-22-320.jpg)

1) The document discusses several models for pricing derivatives in energy markets, including a 2-factor model, an Exode model, and models based on Levy processes. 2) It proposes an asset price model that incorporates mean-reversion, seasonal variations in forward curves, and the leptokurtic behavior of log-spot prices using a Levy process. 3) The model discretizes the Levy process using a Euler scheme and estimates the model parameters using maximum likelihood methods.

![11.[104 111]analytical solution for telegraph equation by modified of sumudu ...](https://cdn.slidesharecdn.com/ss_thumbnails/11-104-111analyticalsolutionfortelegraphequationbymodifiedofsumudutransformelzakitransform-120513000219-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)