Download to read offline

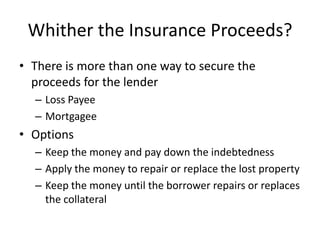

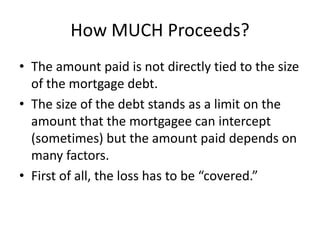

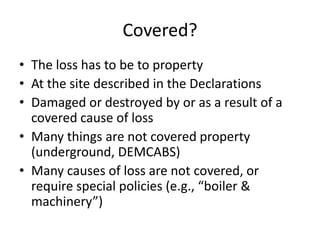

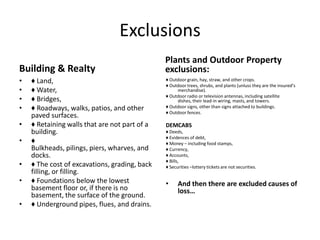

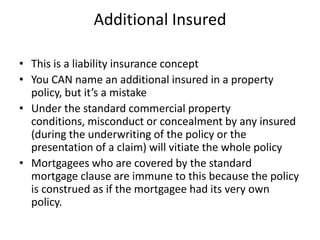

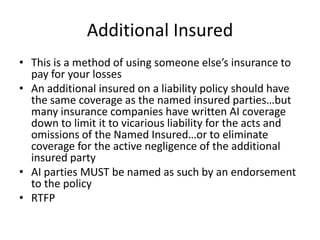

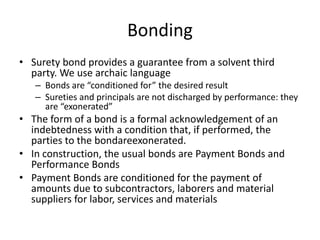

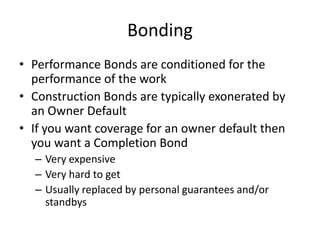

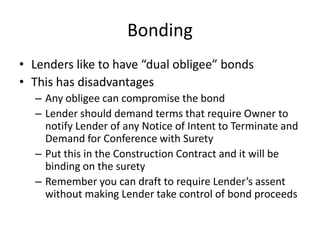

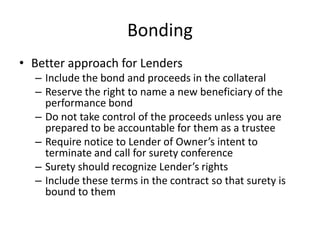

This document provides an overview of common mistakes that lenders make regarding insurance. It discusses the importance of understanding insurance contracts and coverage details. Key points include: defining covered losses and determining how insurance proceeds will be used; ensuring sufficient coverage amounts and resolving valuation issues; avoiding assumptions that insurance proceeds replace lost collateral; and properly naming additional insureds and beneficiaries on bonds. Reading the full policy and understanding exclusions, limitations, and obligations is emphasized.