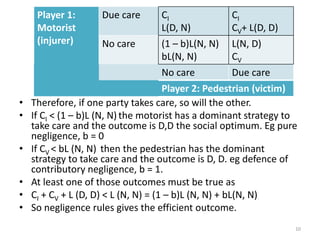

The document discusses the implications of the Productivity Commission's proposed no-fault insurance scheme for catastrophic injuries, advocating for a national insurance scheme that provides care and support without fault liability. It critiques the proposal, arguing that it overlooks the deterrent effect of tort law on behavior and could increase accident costs and incidents by removing incentives for victims to act cautiously. The analysis suggests that while no-fault insurance may simplify compensation, it diminishes the individual responsibility for safety, leading to potentially negative outcomes in road traffic accidents.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)