Download to read offline

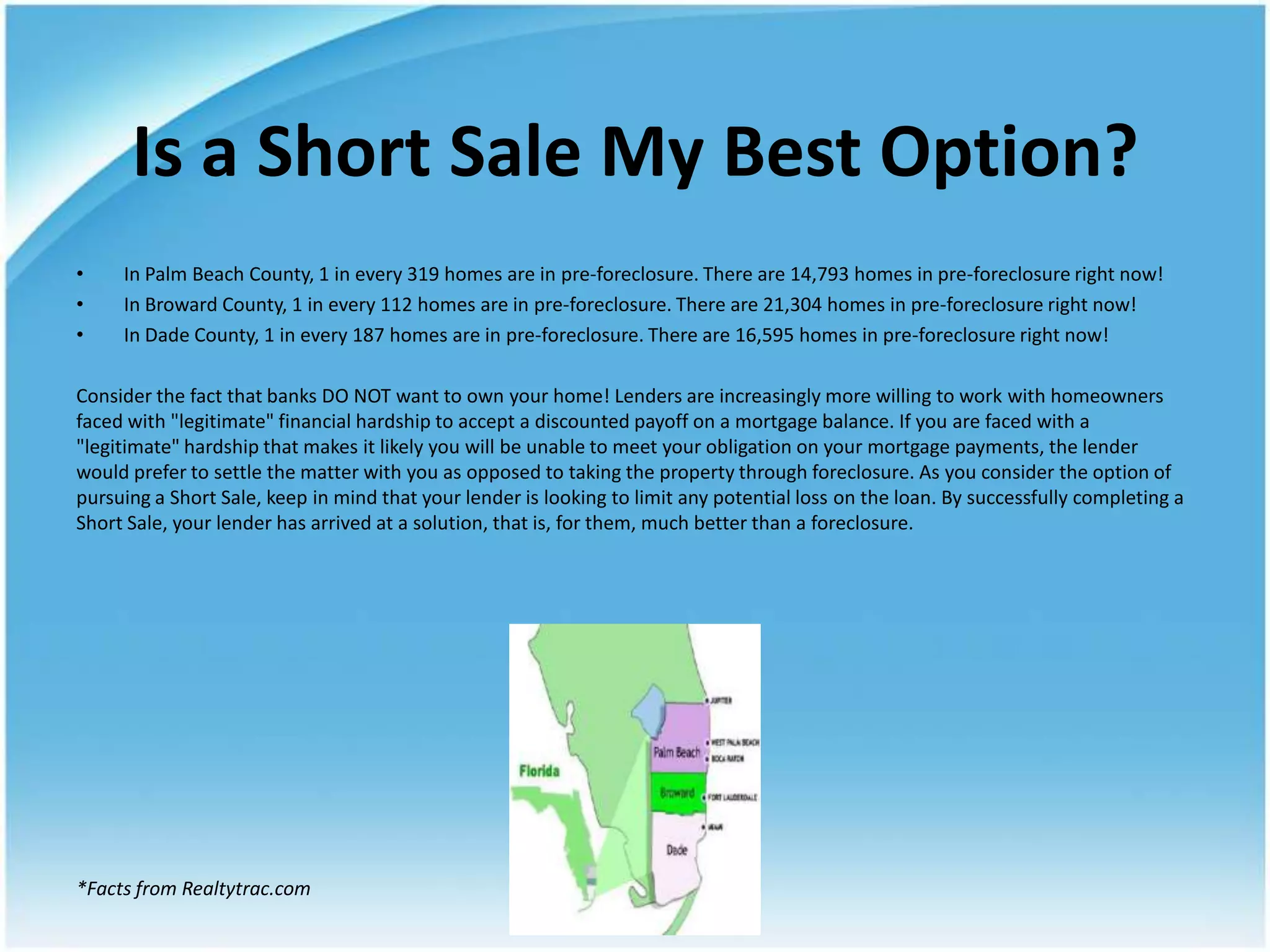

The document provides an overview of foreclosure alternatives, especially focusing on short sales as a viable option for distressed homeowners in Florida. It explains the foreclosure process, the differences between short sales and foreclosures, and includes essential tax implications related to both scenarios. Additionally, it emphasizes the importance of consulting legal and real estate professionals for personalized guidance on financial hardships.