This document discusses concepts related to demand, including:

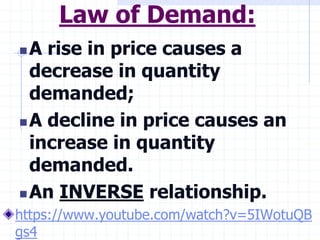

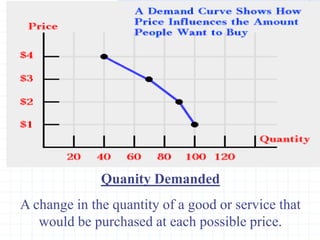

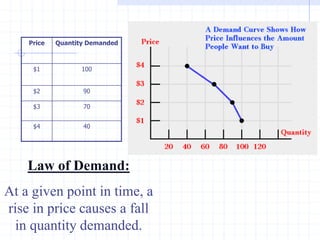

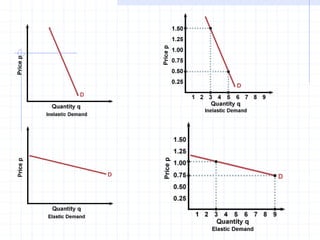

1. Demand is determined by desire and ability to pay. The law of demand states that as price rises, quantity demanded falls, and vice versa. Demand is graphed with quantity on the horizontal axis and price on the vertical axis.

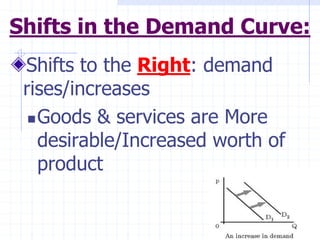

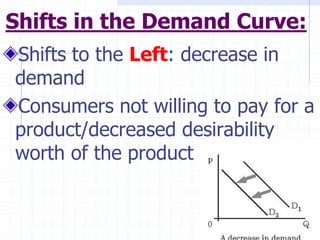

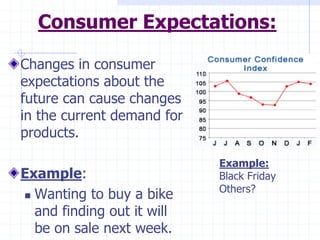

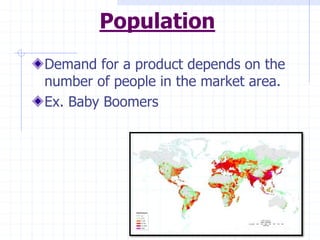

2. Factors that can shift the demand curve include tastes, income, prices of substitutes and complements, expectations, and population. A shift to the right indicates increased demand while a shift to the left indicates decreased demand.

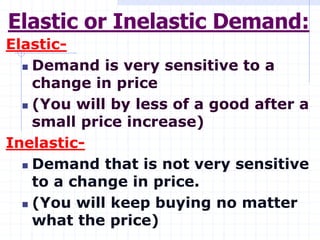

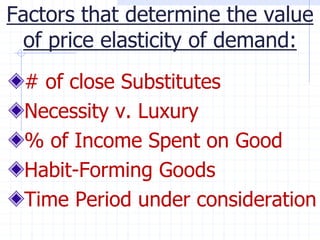

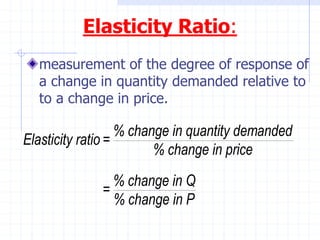

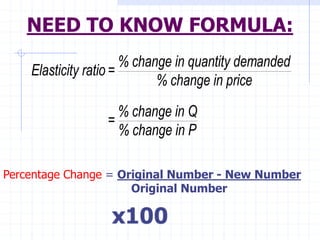

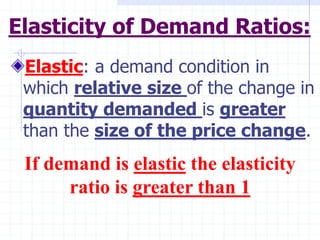

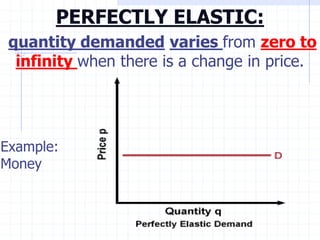

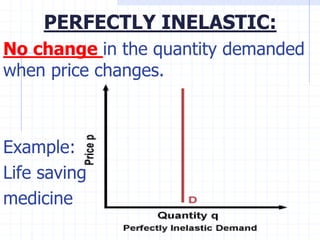

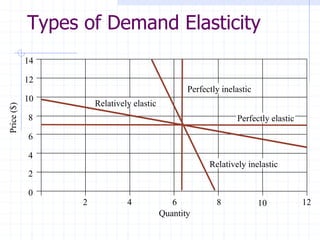

3. Elasticity measures the responsiveness of quantity demanded to price changes. Demand is elastic if a small price change leads to a large quantity change, inelastic if