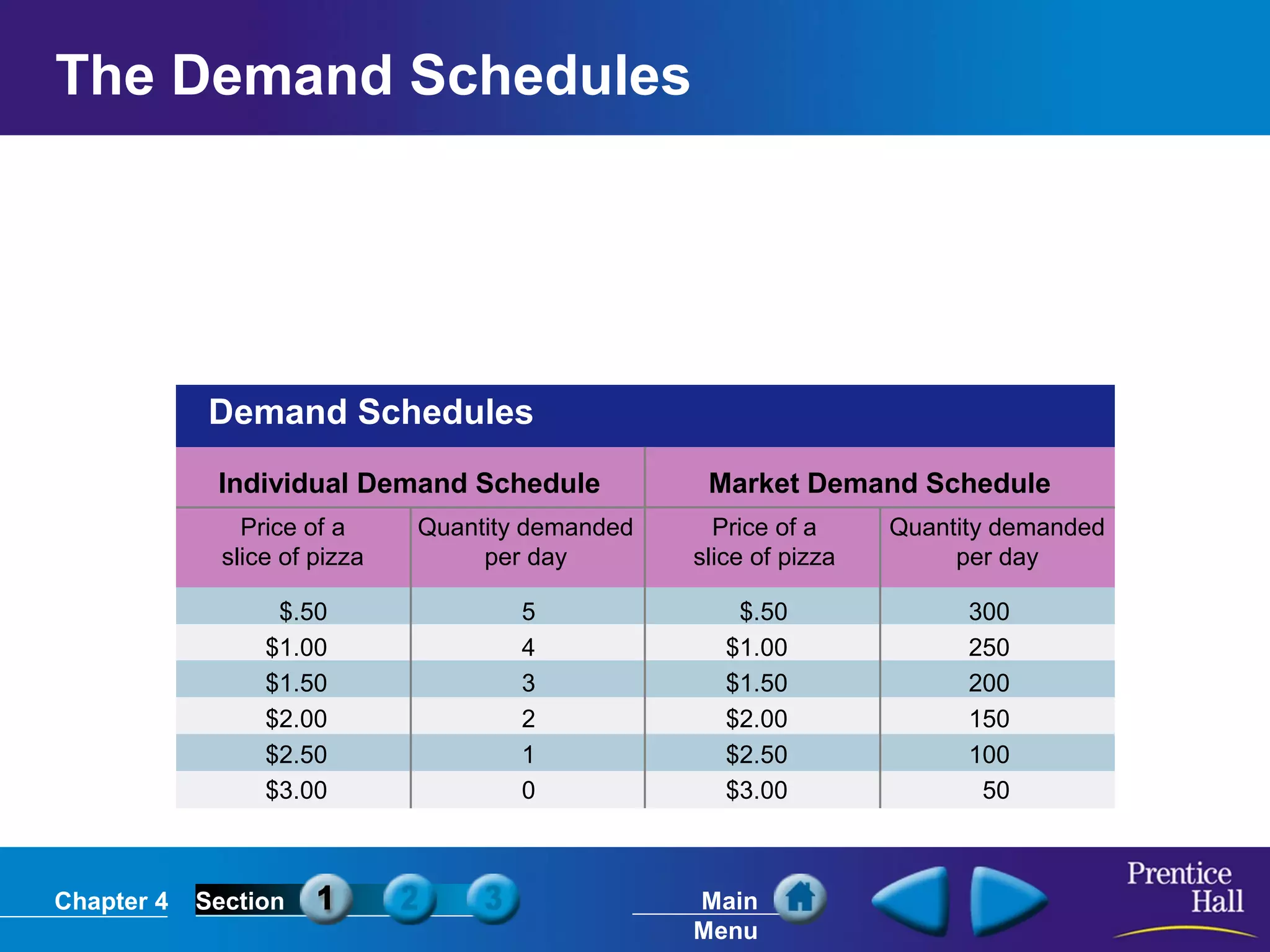

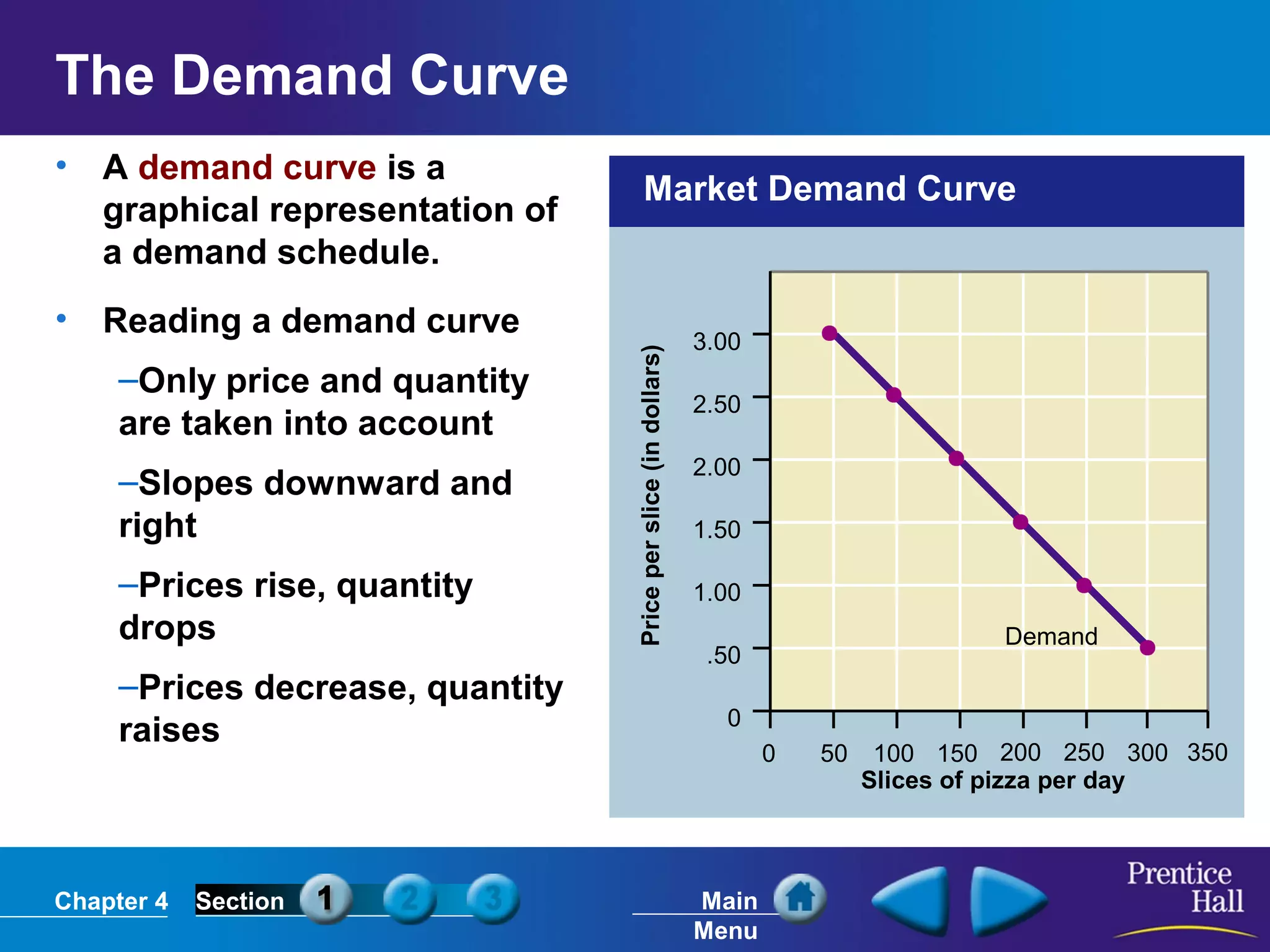

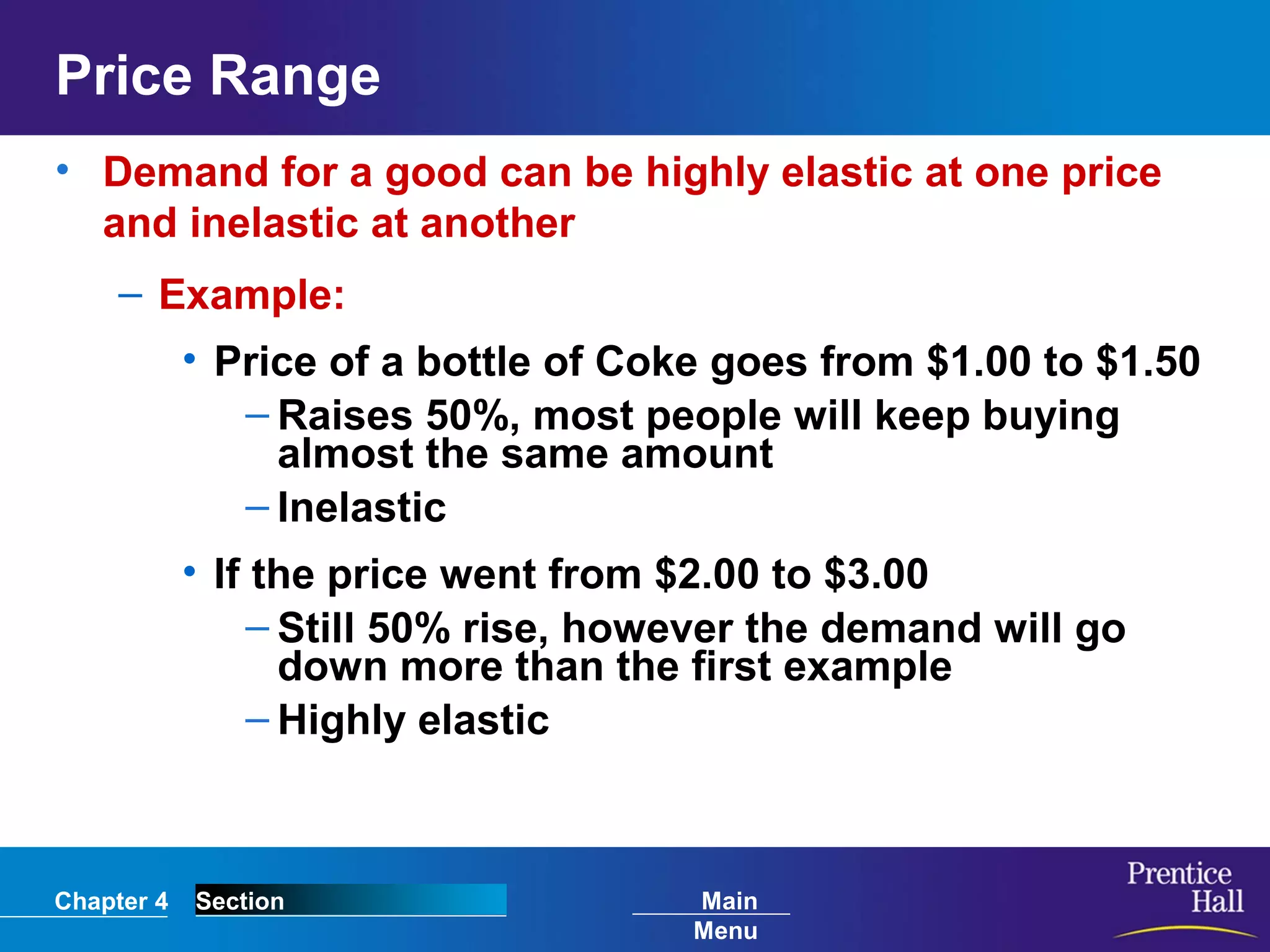

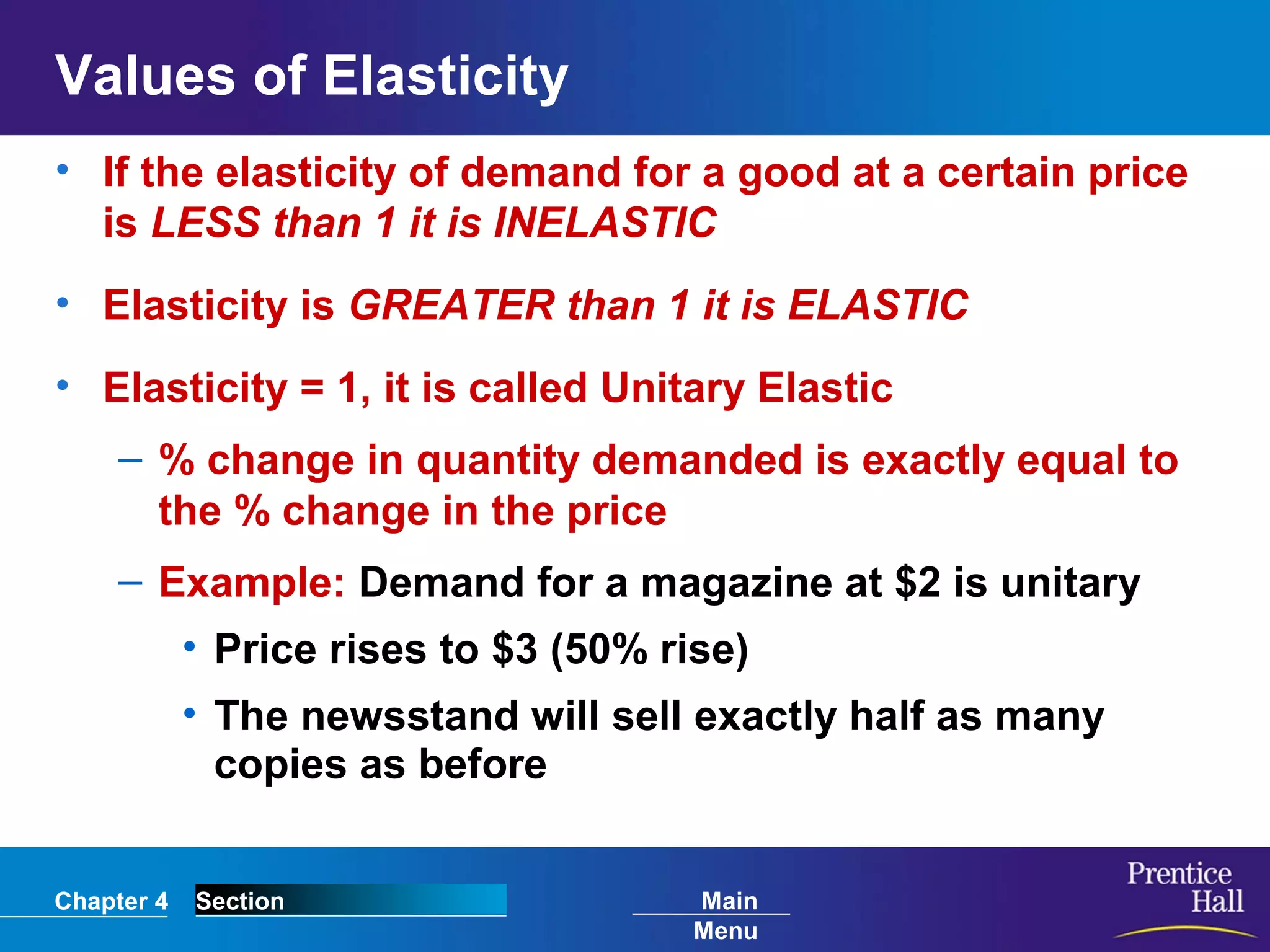

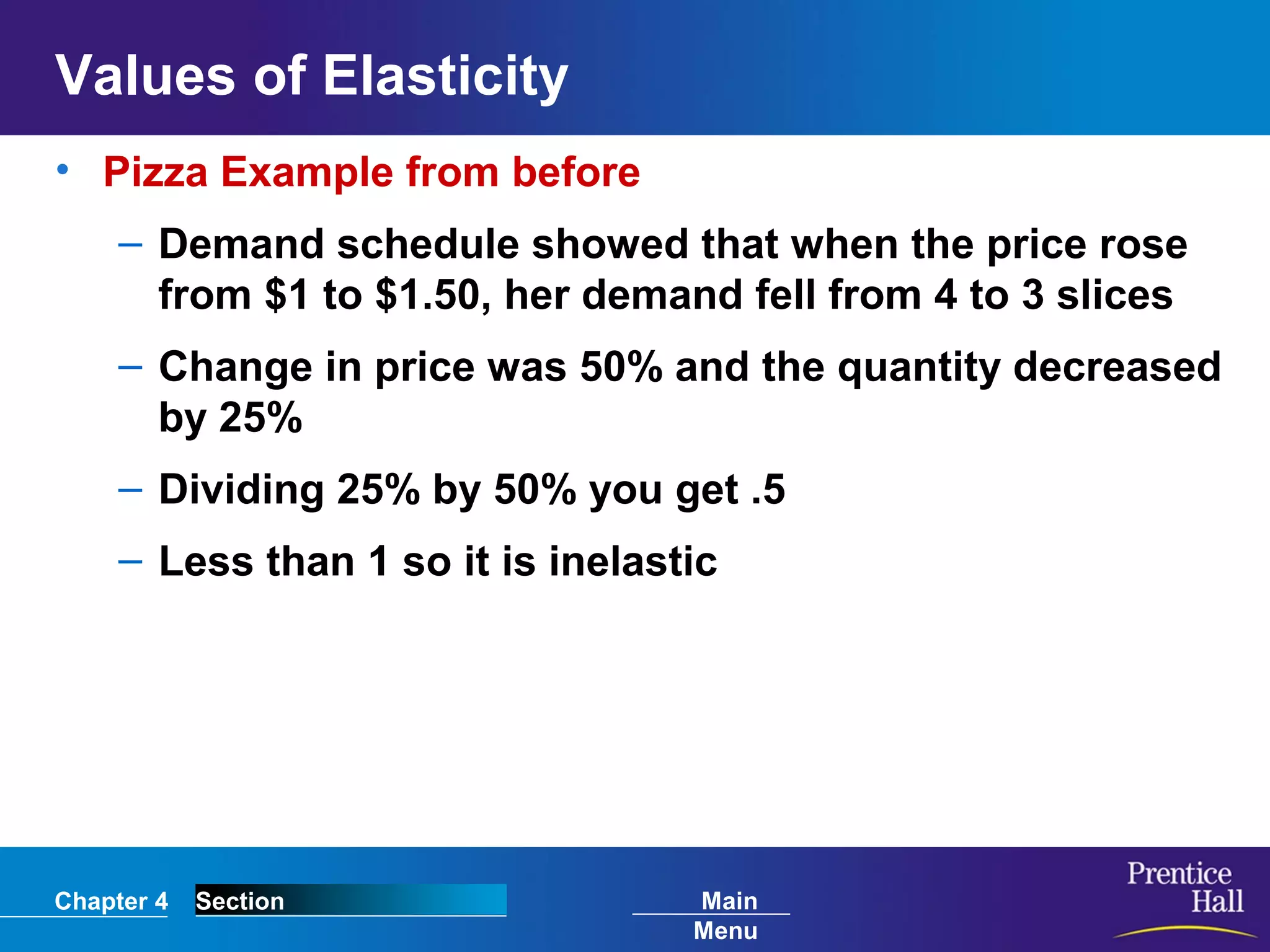

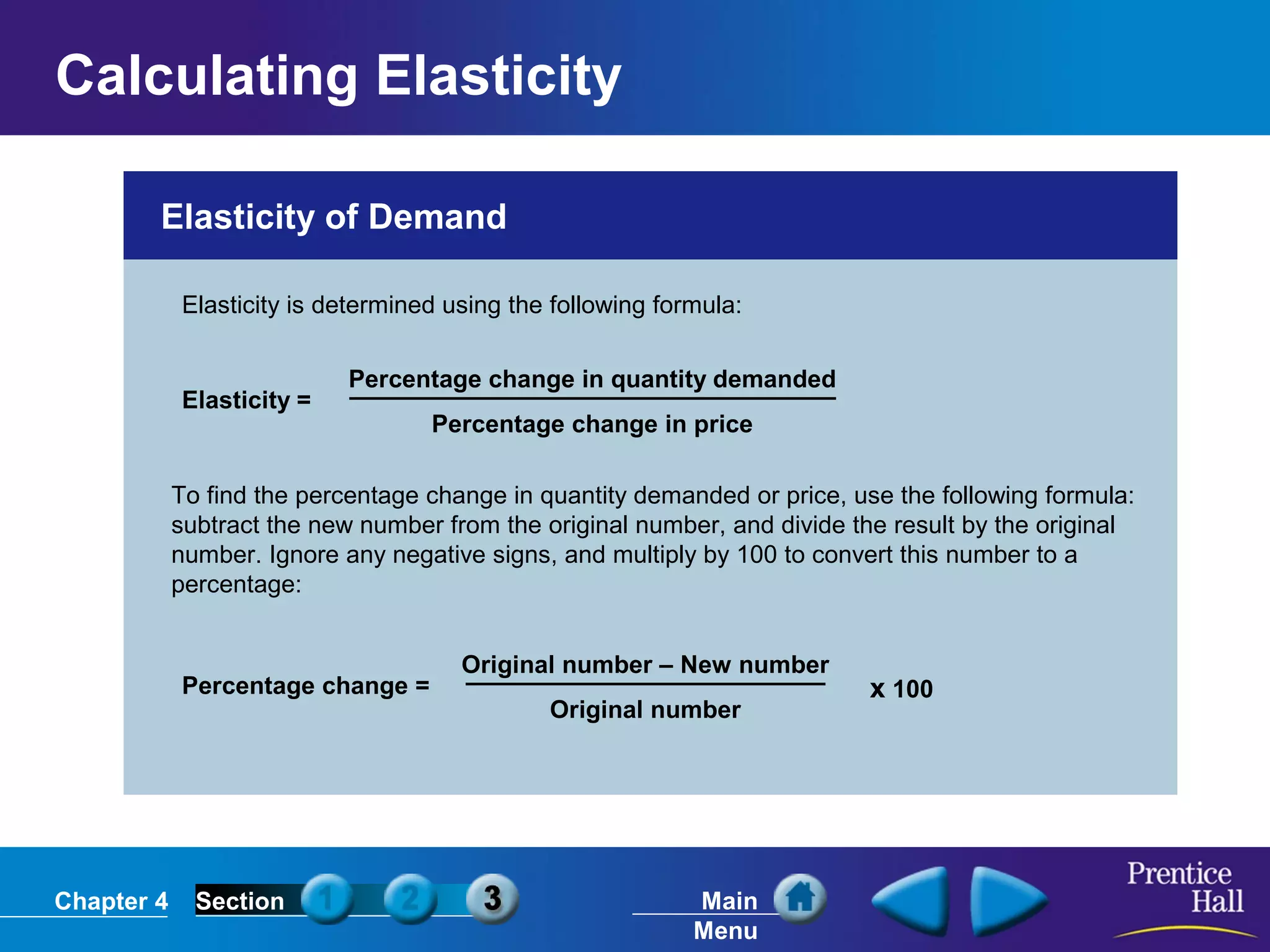

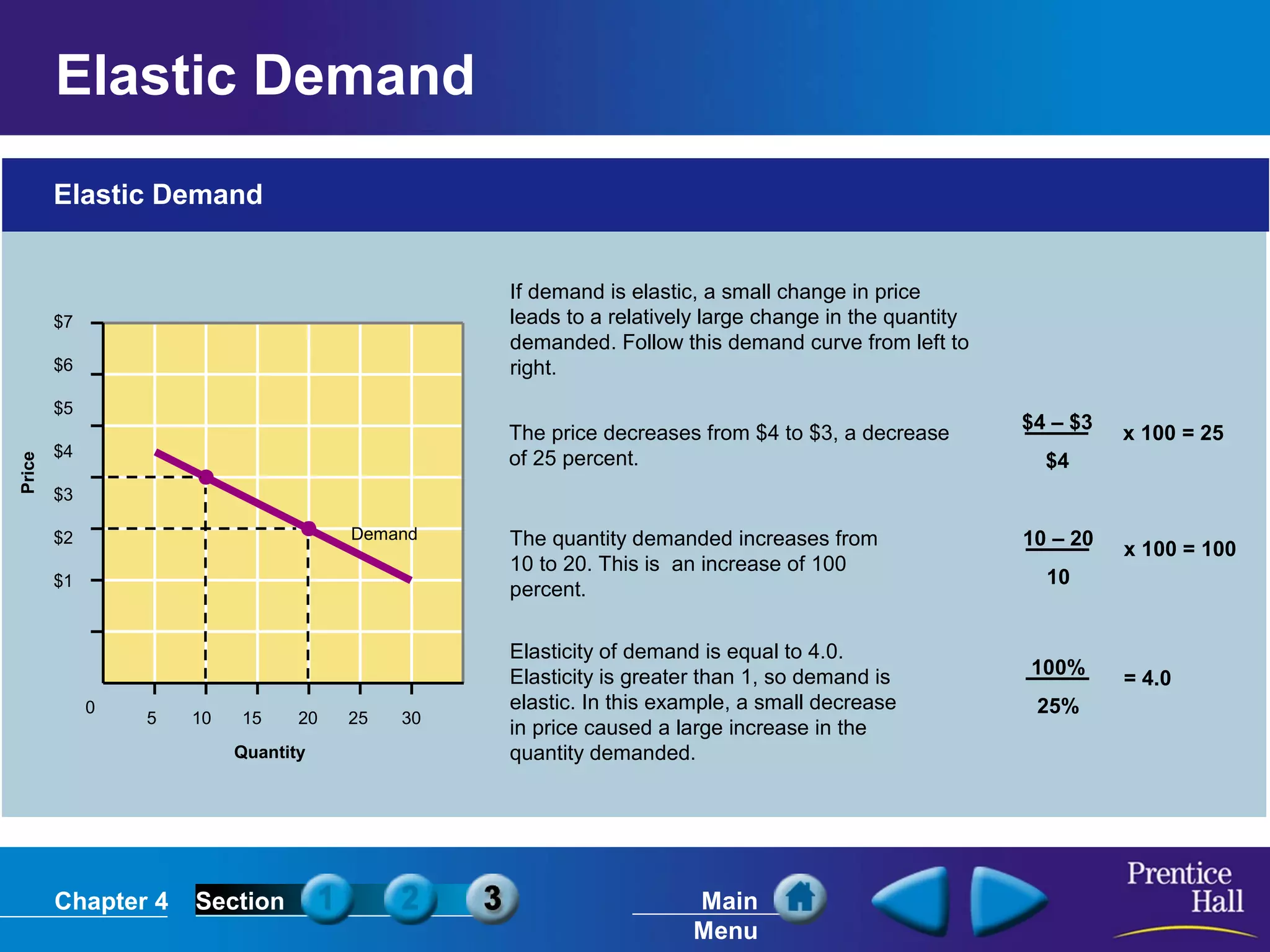

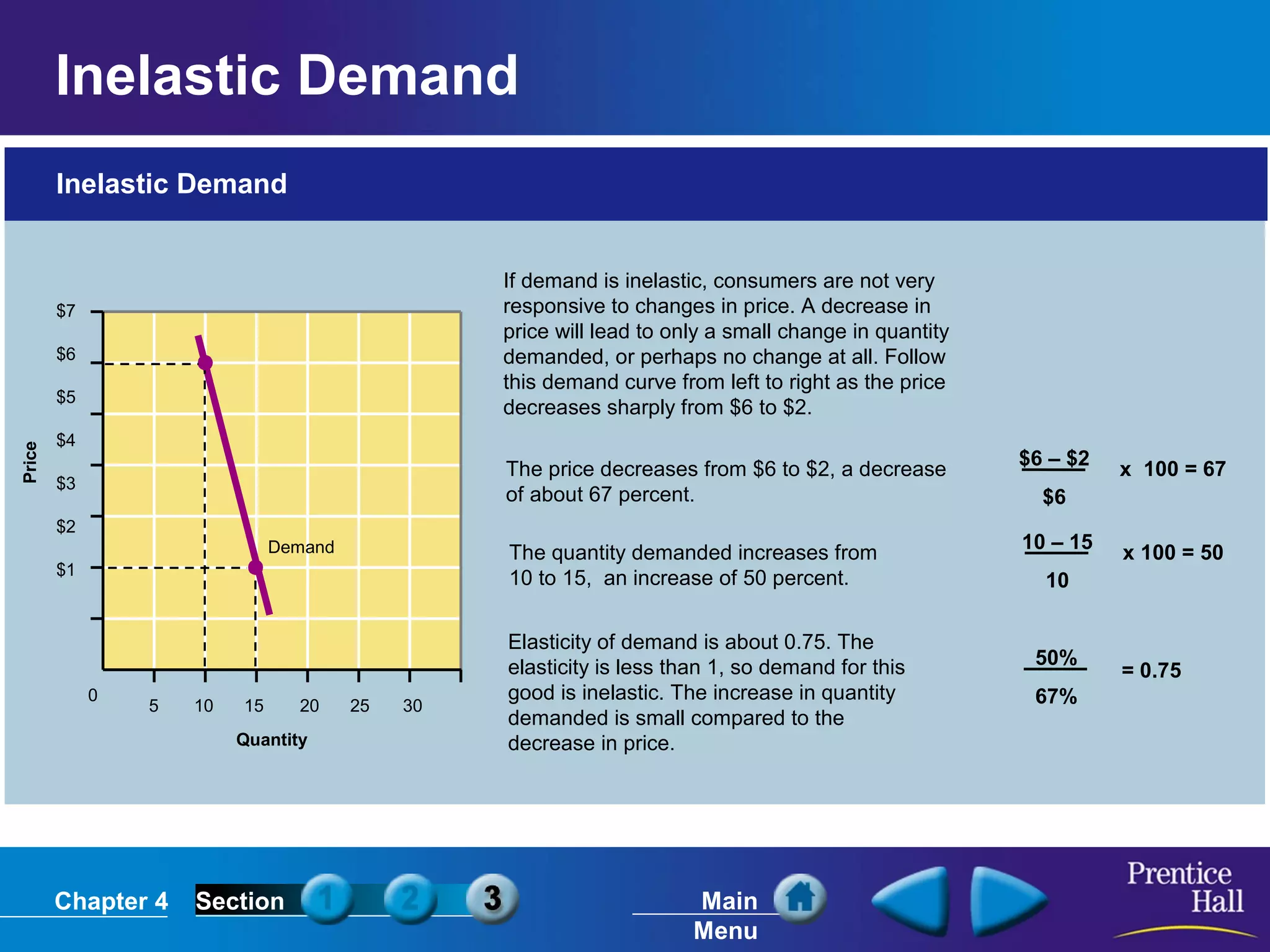

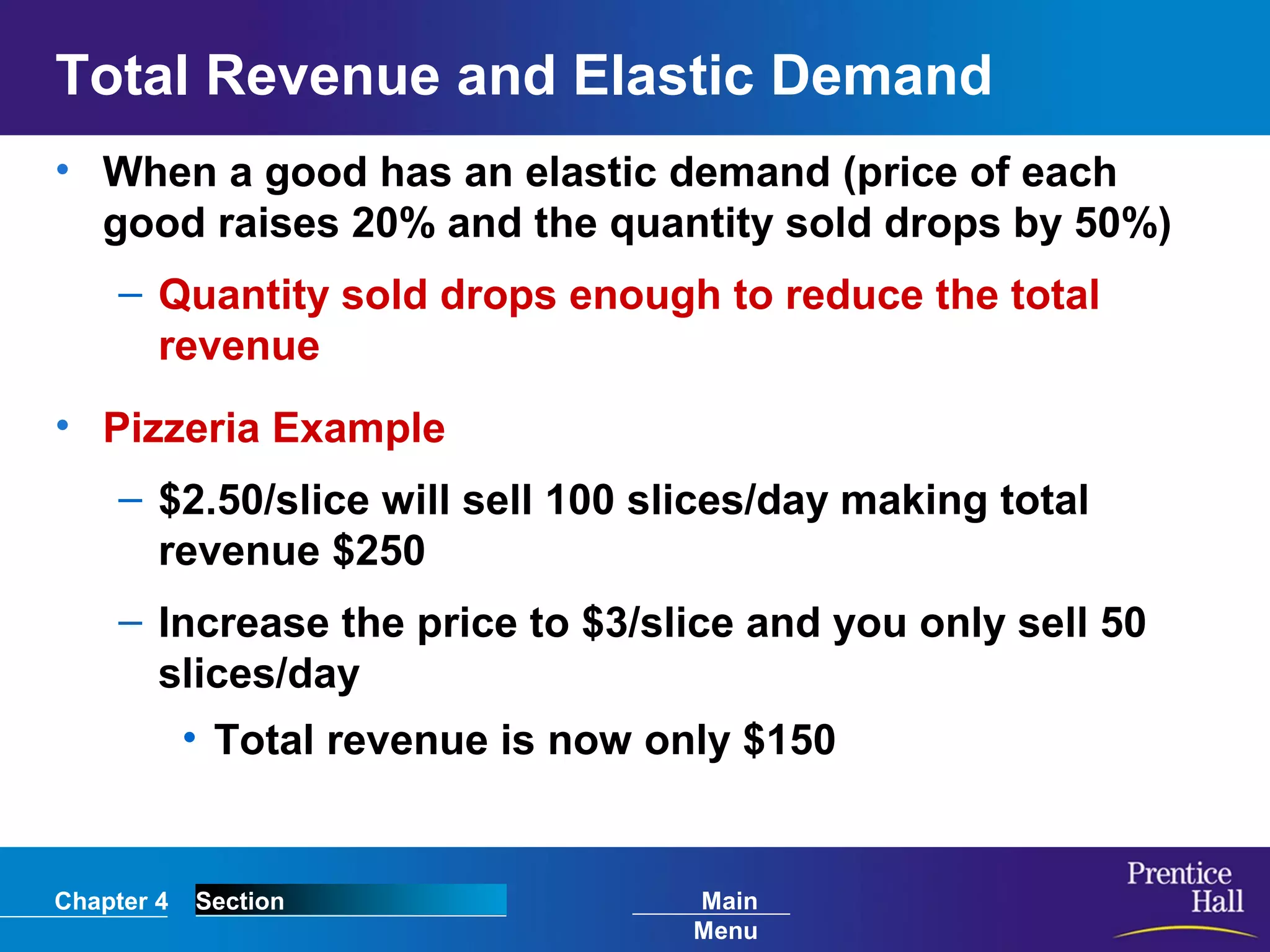

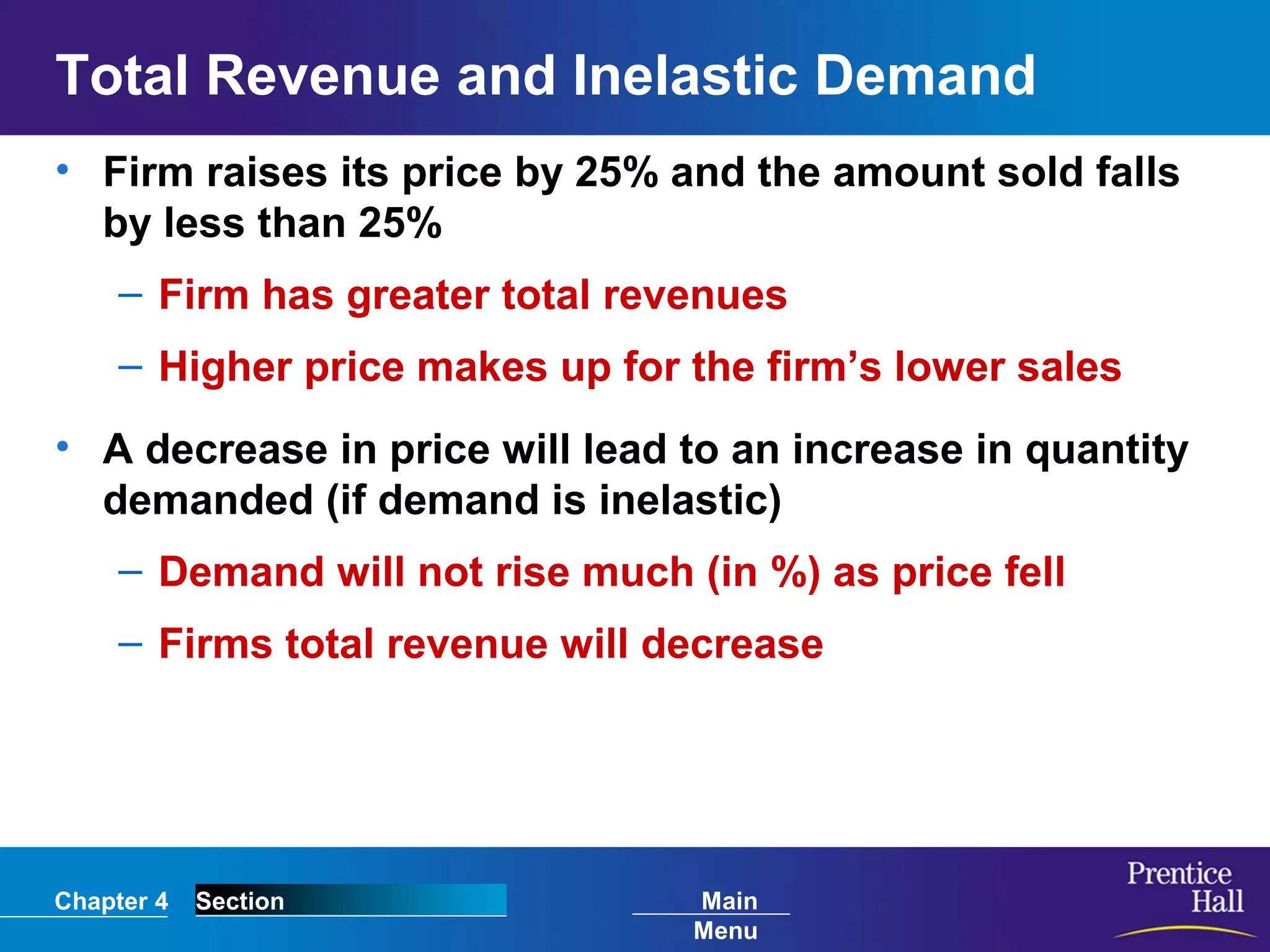

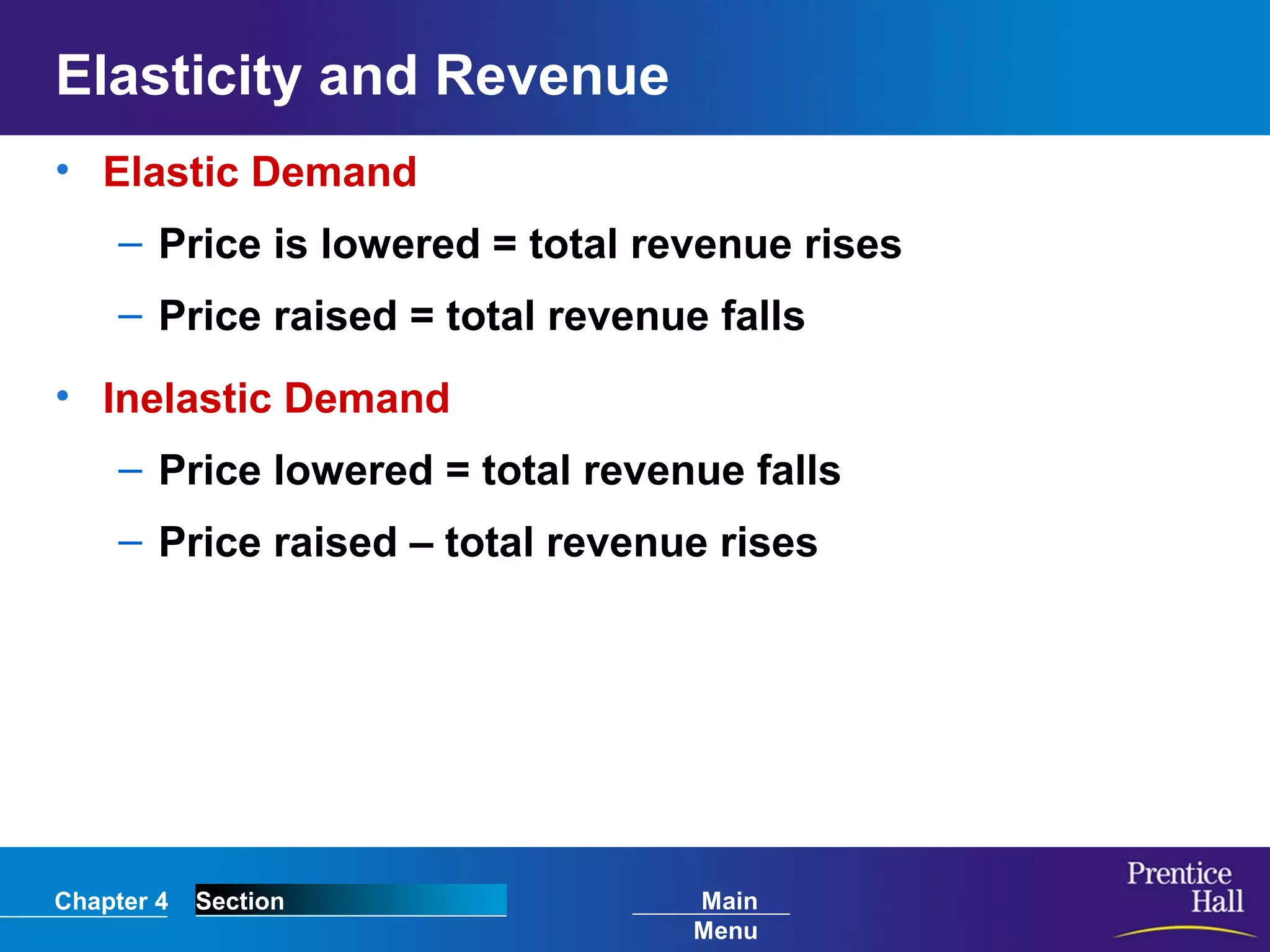

The document discusses concepts related to demand, including the law of demand, demand schedules, demand curves, elasticity of demand, and how elasticity affects total revenue. Specifically, it explains that according to the law of demand, as price increases, quantity demanded decreases, and vice versa. It provides examples of demand schedules and how they are used to construct demand curves. It also discusses factors that can cause a shift in the demand curve, such as changes in income, population, or prices of related goods. Finally, it explains the concept of elasticity of demand and how elastic versus inelastic demand impacts a firm's total revenue when price is changed.