Download to read offline

![iii

NAWRU Non-Accelerating Wage Rate of Unemployment

PMI Purchasing Managers' Index

REER Real Effective Exchange Rate

SGP Stability and Growth Pact

VAT Value-Added Tax

CPB Centraal Planbureau, the Netherlands Bureau for Economic Policy Analysis

ECB European Central Bank

EIB European Investment Bank

EFSF European Financial Stability Facility

EMU Economic and Monetary Union

ESM European Stability Mechanism

FOMC Federal Open Market Committee, US

Fed Federal Reserve, US

IMF International Monetary Fund

OBR Office for Budget Responsibility, UK

OECD Organisation for Economic Cooperation and Development

WTO World Trade Organisation

Other abbreviations

AQR Asset Quality Review

BLS Bank Lending Survey

CFCI Composite Financing Cost Indicator

DSGE Dynamic stochastic general equilibrium [model]

FDI Foreign Direct Investment

FLS Funding for Lending Scheme, UK

FY Financial year

JPA Job Protection Plan, Hungary

LFS Labour Force Survey

LTRO Longer-Term Refinancing Operation

MRO Main Refinancing Operations

NFC Non-Financial Corporations

OMT Outright Monetary Transactions

SME Small and medium-sized enterprises

SMP Securities Market Programme, ECB

QUEST Quarterly Estimation and Simulation Tool, DG ECFIN's DSGE model

Graphs/Tables/Units

a.a. Annual average

bbl Barrel

bn Billion

bps Basis points

lhs Left hand scale

pp. / pps. Percentage point / points

pts Points

Q Quarter

q-o-q% Quarter-on-quarter percentage change

rhs Right hand scale

SAAR Seasonally-Adjusted Annual Rate

tn Trillion

y-o-y% Year-on-year percentage change](https://image.slidesharecdn.com/europeancommissionsautumnforecast2014-141120054853-conversion-gate02/75/European-commission-s-autumn-forecast-2014-5-2048.jpg)

![EA and EU outlook

33

area over the forecast horizon, though more

moderately than during the crisis period and to

stabilise in the EU.

…amid narrowing cross-country differences.

Labour market conditions and performances

continue to differ substantially across EU countries

but these divergences seem to have begun

narrowing this year. Unemployment rates in a

number of Member States worst affected by the

crises, such as Ireland, Portugal, Spain and Greece

were considerably below their cyclical peaks in

August. Unemployment in Ireland and Portugal

was down 3.1 pps., while in Spain and Greece,

unemployment was down 1.2 pps. and 1.1 pps.

respectively. The reduction has been more limited

in countries with the lower cyclical peaks such as

Austria -0.3 pp. or Germany -0.5 pp.. Thus,

unemployment in the euro area as a whole has

fallen mainly because of declines in the most

stressed countries. Looking ahead, labour market

differences are expected to continue narrowing

over the forecast horizon, although they will

nonetheless remain large. Unemployment rates are

expected to range from 4.8% in Germany to about

22% in Greece and Spain in 2016.

7. INFLATION DEVELOPMENTS

The trend towards lower inflation across EU

Member States has continued in autumn, guided by

lower commodity prices and remaining economic

slack. The outlook of a gradual pick-up in HICP

inflation rests on a gradual narrowing of the output

gap and a gradually easing of the dampening

influence of external factors.

A confluence of factors is keeping inflation

very low...

The EU economy’s disinflationary slide has

continued in 2014. HICP inflation continued to fall

in the first three quarters to 0.5% in the EU and

0.4% in the euro area. The persistence of low

inflation in Europe can be explained by a mix of

global factors and the weak economic

environment. The decline in global commodity

prices, especially energy and food prices had a

significant impact in driving headline inflation

lower. The impact of lower commodity prices was

magnified by the appreciation of the euro against

the US dollar earlier this year. The depreciation

since May did not neutralise the stronger fall in

commodity prices over the summer. The remaining

slack in the economy and weak domestic demand

have kept underlying price pressures low, a fact

also reflected in the prices of services and non-energy

industrial goods.

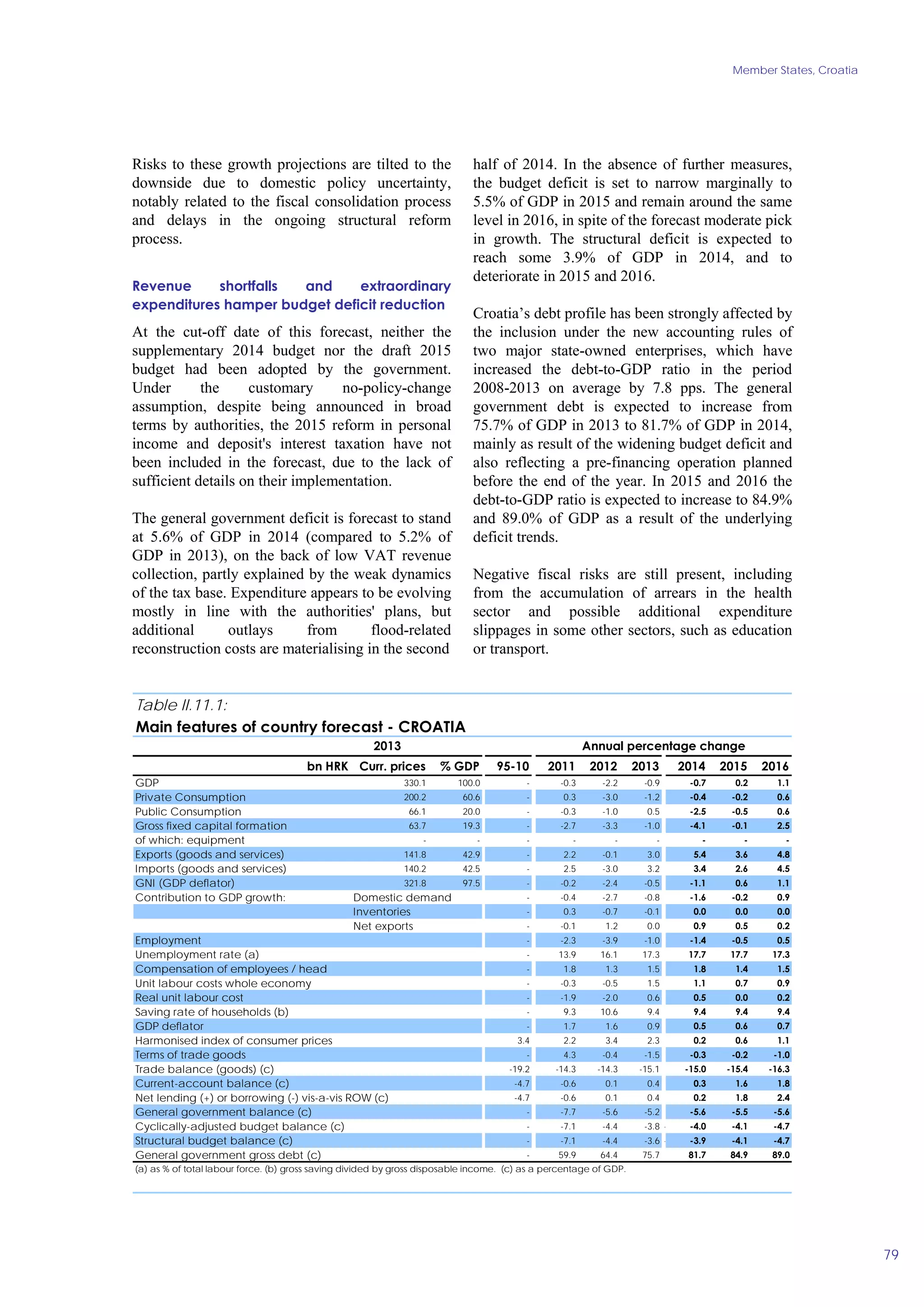

Core inflation (all items excluding energy and

unprocessed food) was on a gradual decline from

2012 up to the third quarter of 2014, but with only

marginal changes in 2014 in both the EU (Graph

I.32) and the euro area. The low level of core

inflation basically reflects historically low services

inflation due to weak demand and contained wage

pressures but also steadily declining non-energy

industrial goods inflation, which can be attributed

to low input prices and declining import prices. In

the third quarter of 2014, core inflation stood at

1.0% in the EU and 0.8% in the euro area, with

services inflation at 1.4% and 1.2% and inflation

of non-energy industrial goods close to zero in

both regions.

5

4

3

2

1

0

-1

%

forecast

Graph I.32: Inflation breakdown, EU

07 08 09 10 11 12 13 14 15 16

Energy and unprocessed food [pps.]

Other components (core inflation) [pps.]

HICP, all items

Disaggregated HICP data show that the decline in

food prices has increased in 2014 with food price

inflation standing at -0.9% in the EU and -0.8% in

the euro area in the third quarter. However, there is

no clear evidence that the decline is mainly caused

as a result of the Russian import ban on imports of

food products from the EU. The Member States hit

most directly by the ban are those with the highest

weights of the products concerned in their HICP

basket. A potential decrease in food prices is

therefore likely to vary across countries and

depends on the extent to which food exports can be

diverted, although diverting them to other Member

States would only matter for the regional

distribution of the impact on HICP inflation.](https://image.slidesharecdn.com/europeancommissionsautumnforecast2014-141120054853-conversion-gate02/75/European-commission-s-autumn-forecast-2014-45-2048.jpg)

The European Economic Forecast for autumn 2014 indicates a slow and fragile recovery for the EU economy, with modest GDP growth projections of 1.3% for the EU and 0.8% for the euro area. The report highlights ongoing challenges including high unemployment, low inflation, and a legacy of the global financial crisis impacting growth. It emphasizes the need for effective economic policies and structural reforms to stimulate investment and improve the economy's growth potential moving forward.