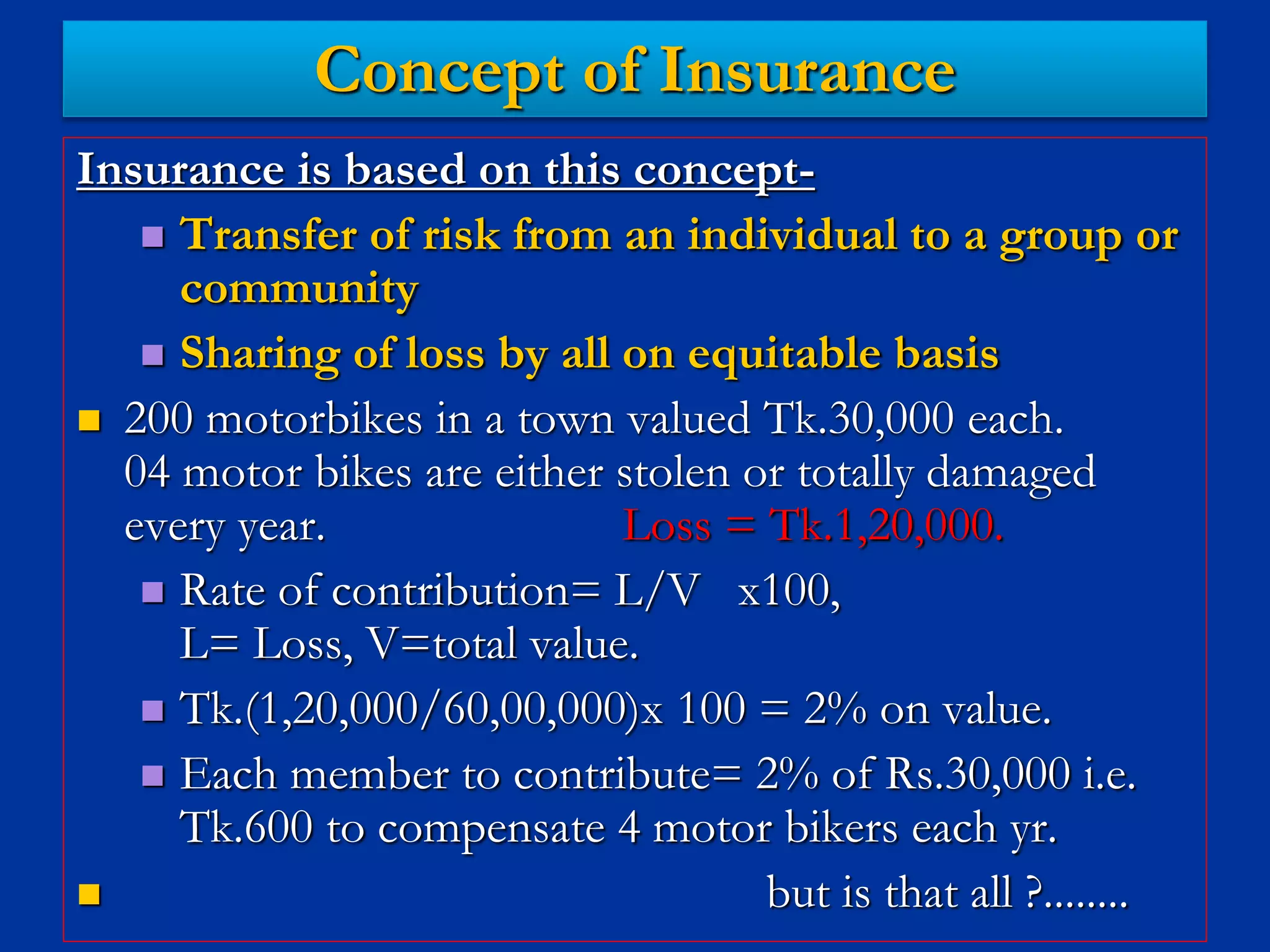

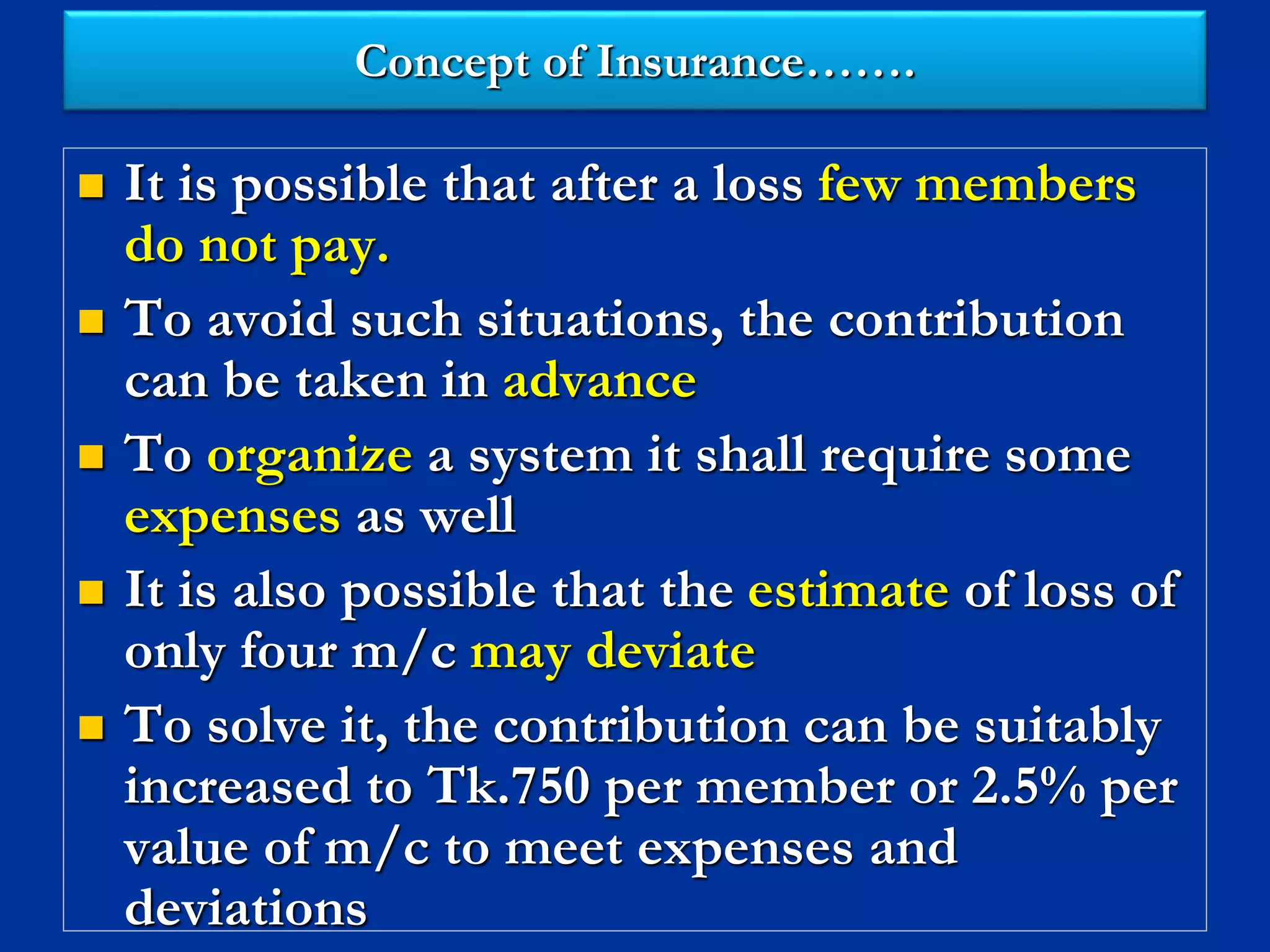

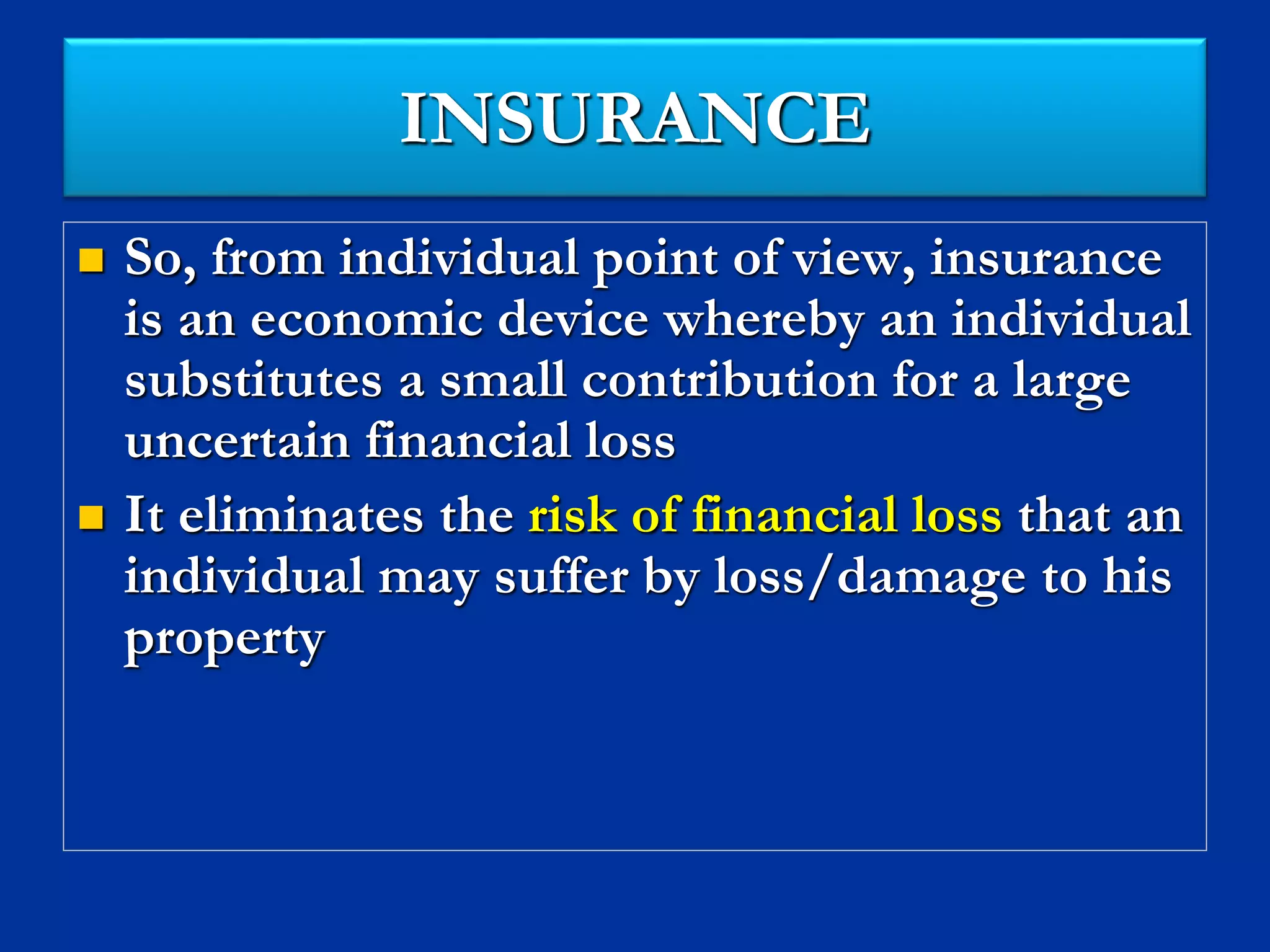

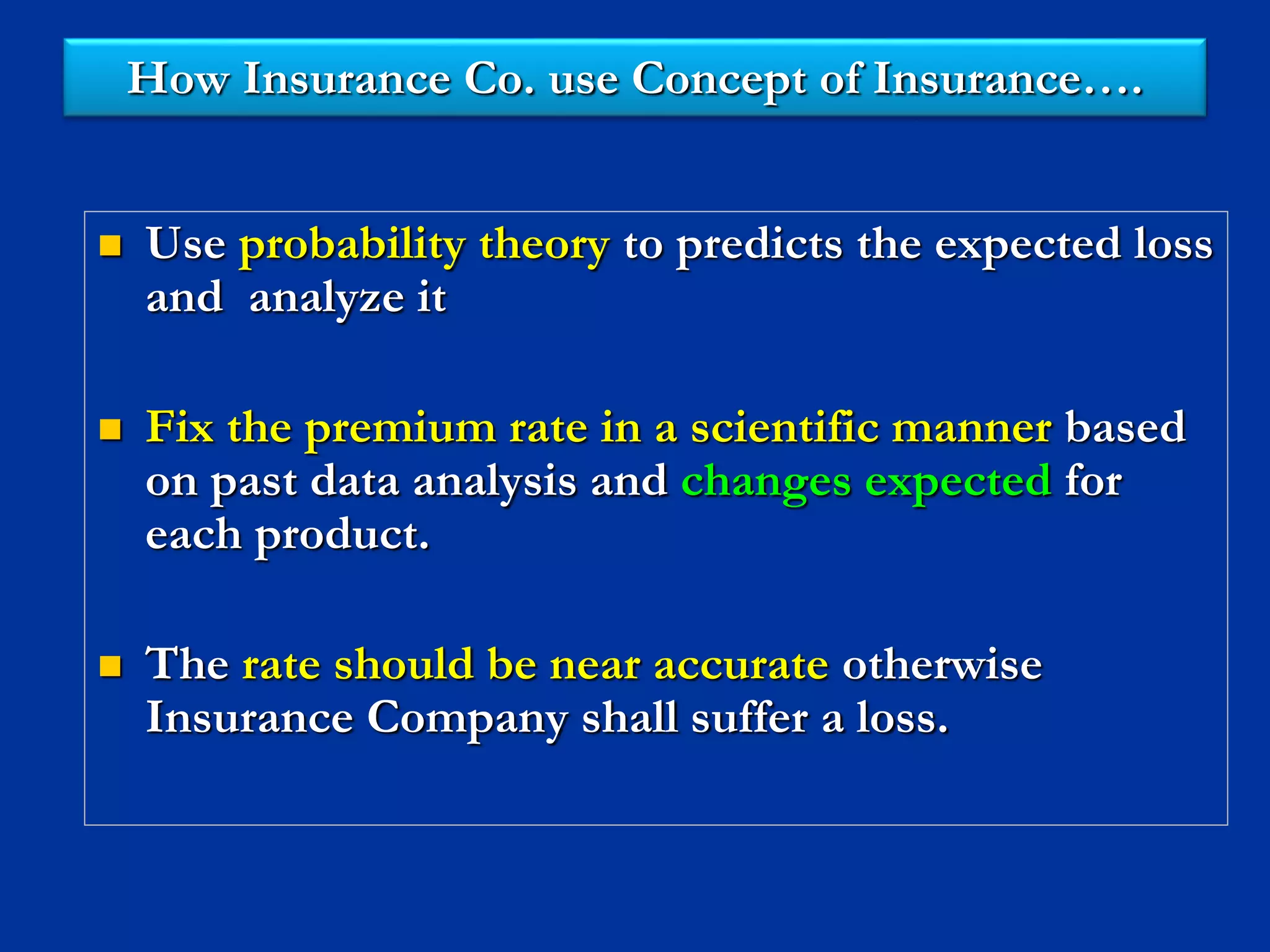

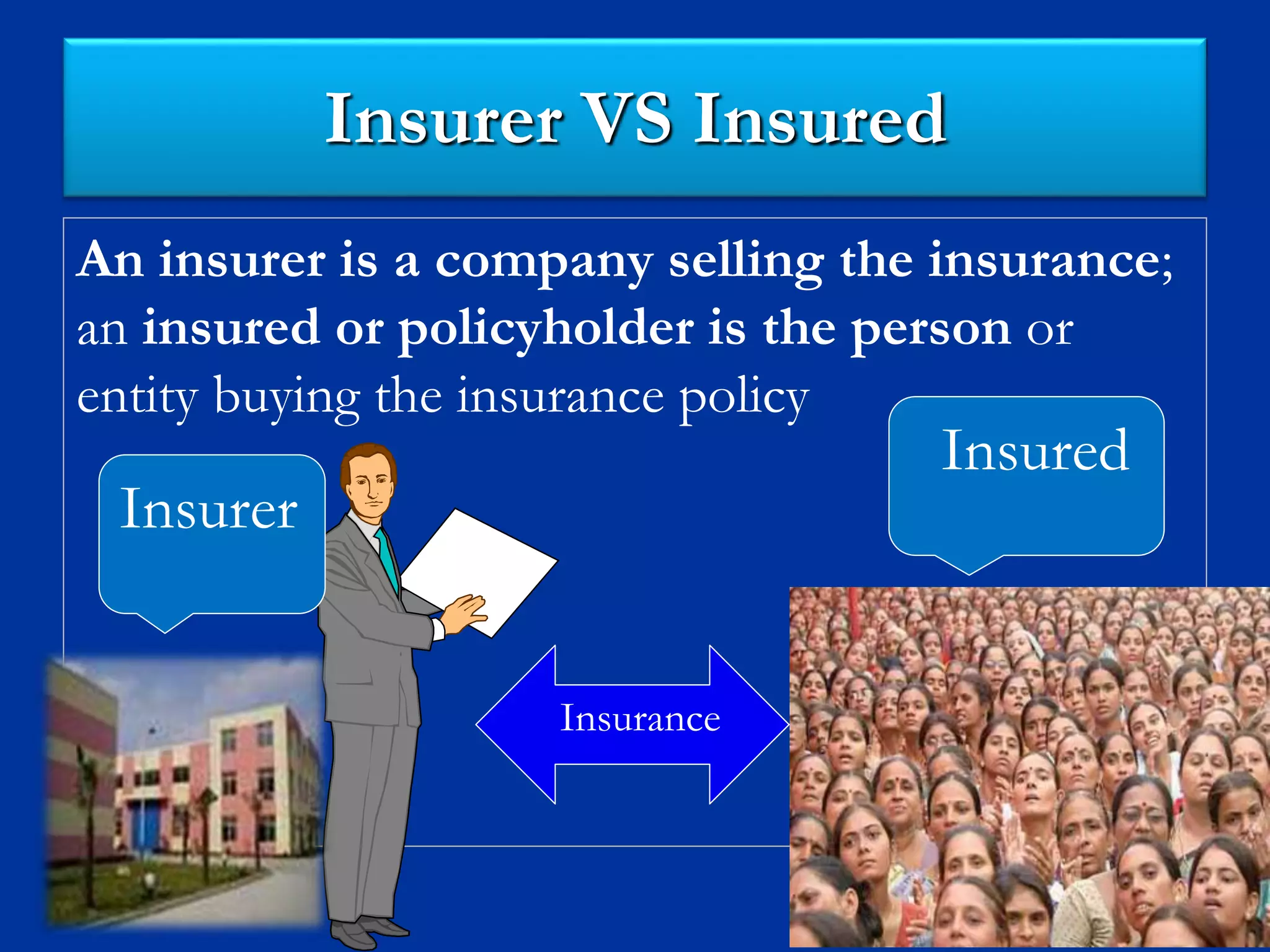

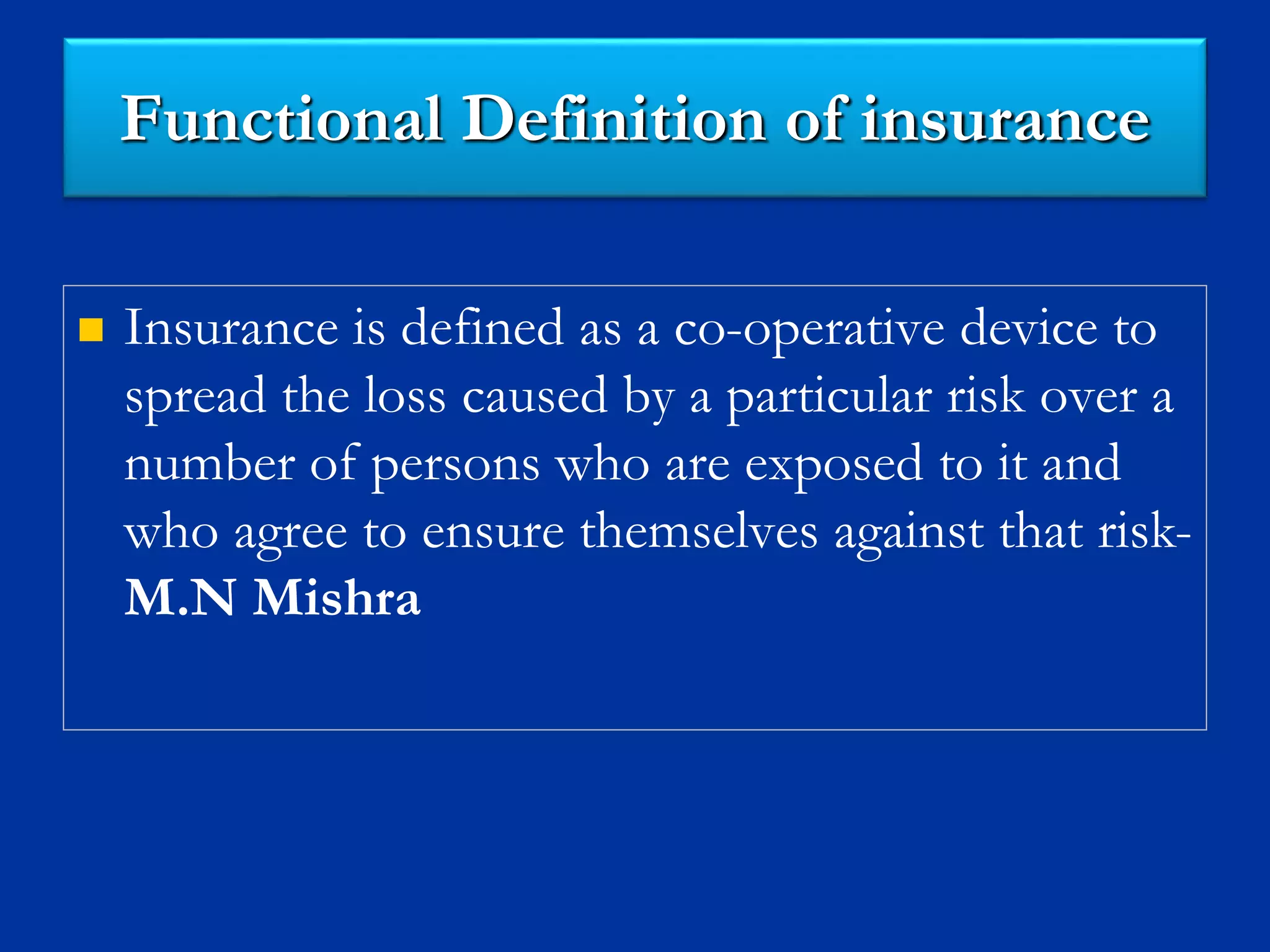

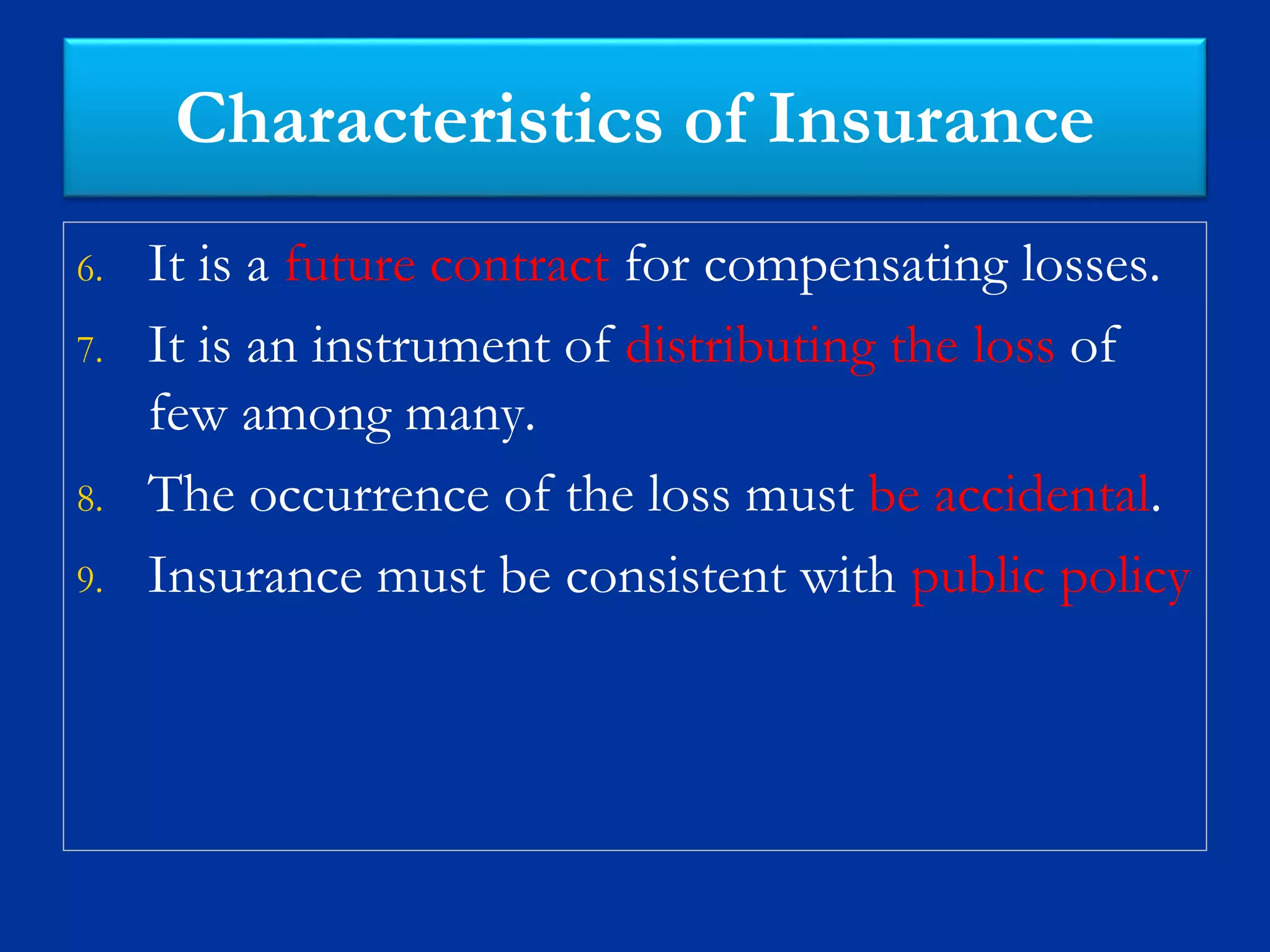

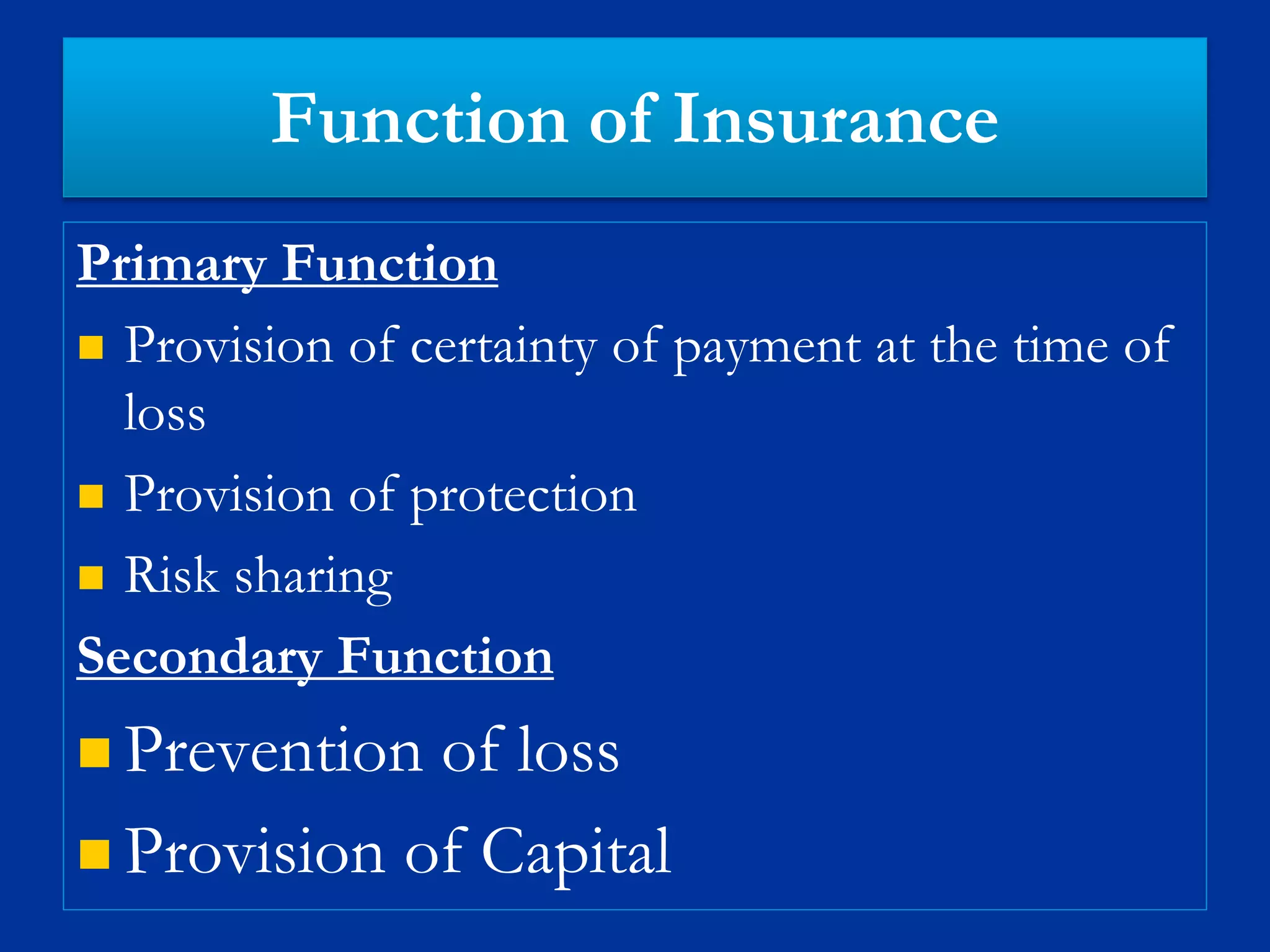

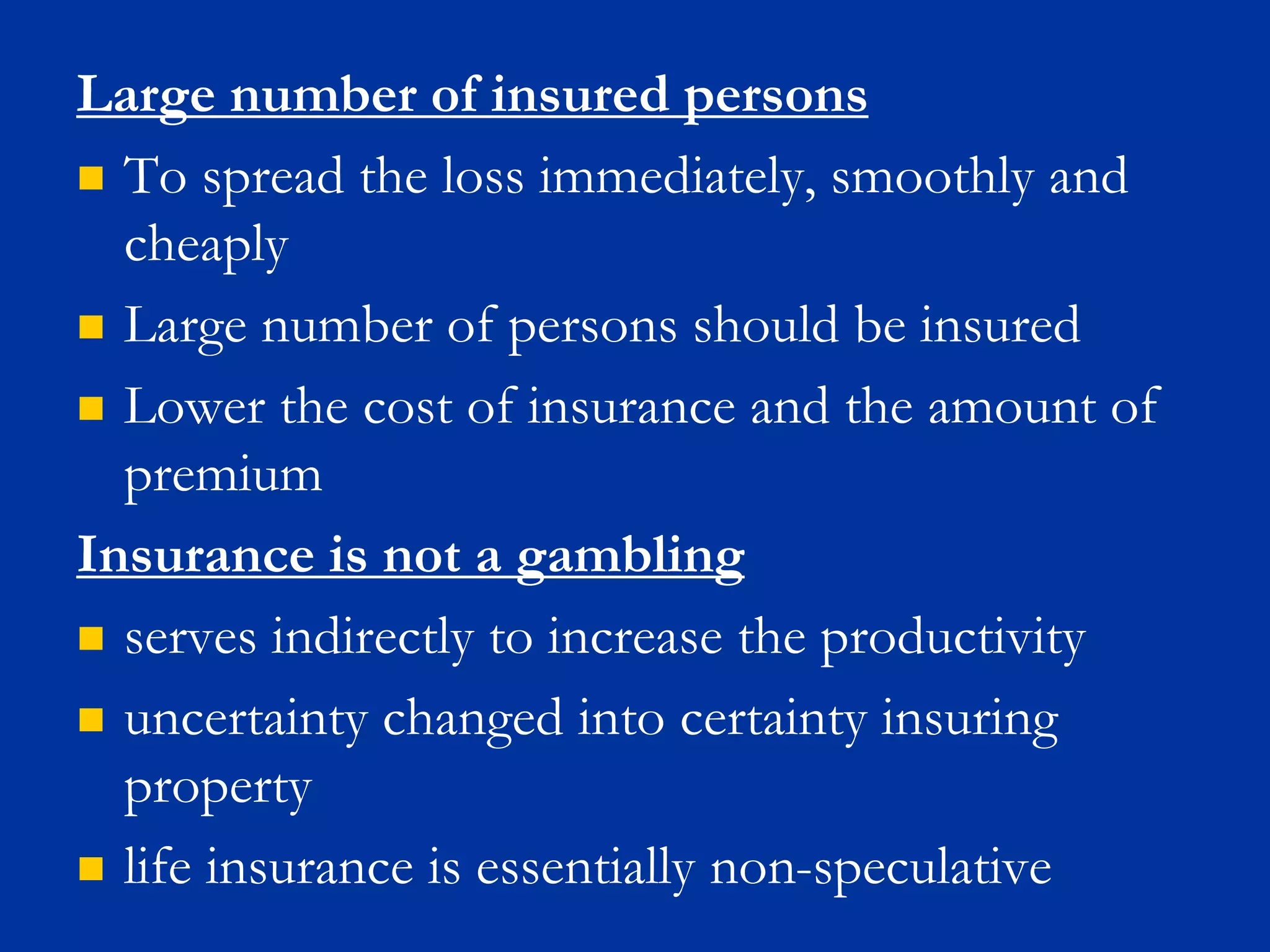

This document discusses key concepts and principles of insurance. It explains that insurance works by transferring risk from individuals to a group, where losses are shared equitably among members. Premium contributions are calculated based on past loss experience to determine expected losses. Insurance companies collect premiums in advance from a large number of policyholders to compensate the few who suffer losses, using statistical data and probability theory to set accurate premium rates. The document defines insurance and outlines its nature as a risk-sharing cooperative device where payments are made contingent on specified events.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)