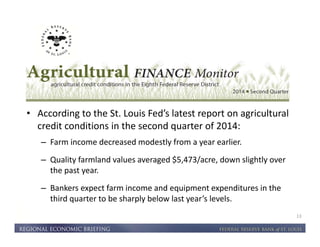

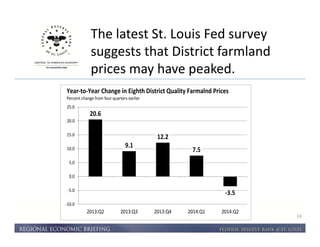

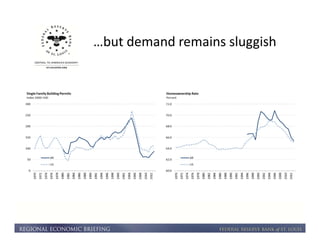

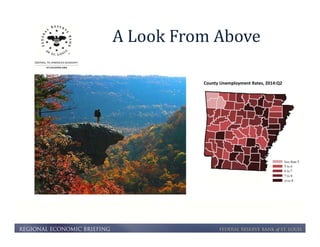

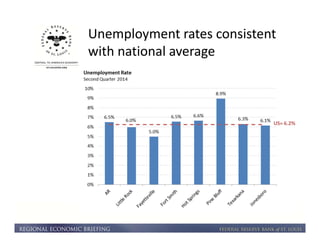

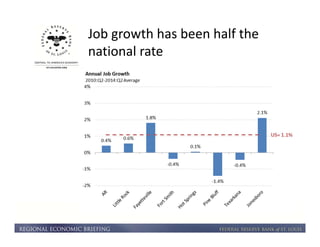

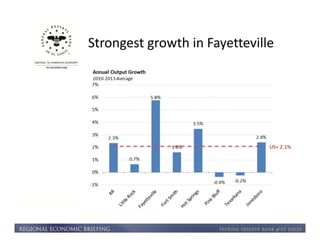

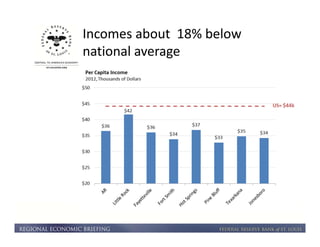

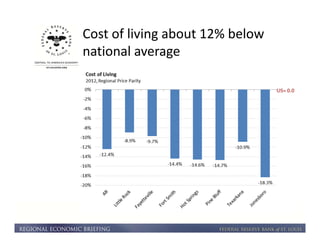

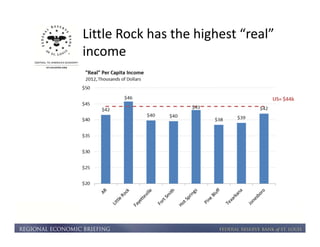

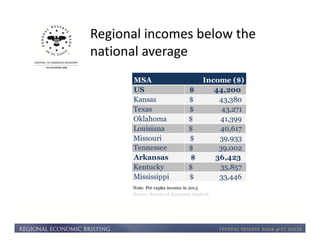

This document summarizes an economic conference held by the Federal Reserve Bank of St. Louis on October 15, 2014. It discusses current economic conditions in the US and Arkansas. The US economy is seeing steady job growth and falling inflation and unemployment. However, a stronger dollar and weaker global growth could impact exports. In Arkansas, farm income decreased while farmland values fell slightly. The latest survey suggests Arkansas farmland prices may have peaked. Regional economic growth has exceeded the national average, though job growth in Arkansas has been half the national rate and incomes remain below average.