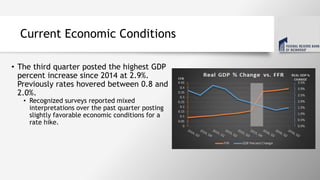

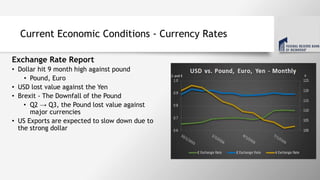

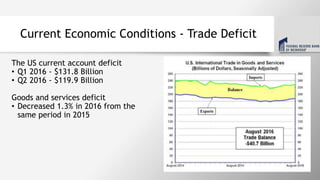

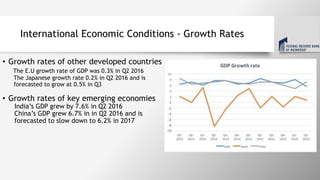

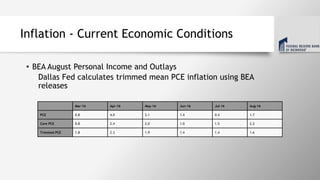

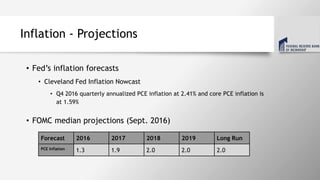

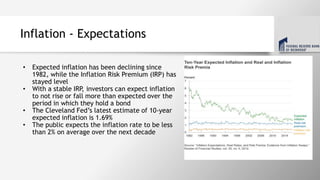

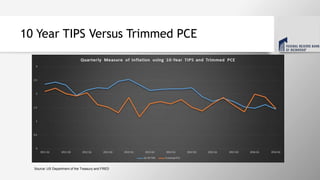

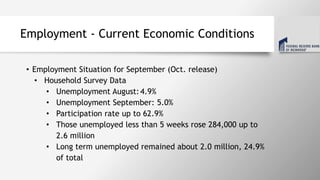

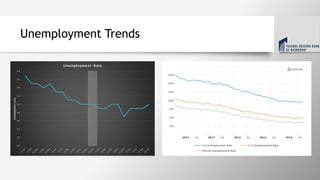

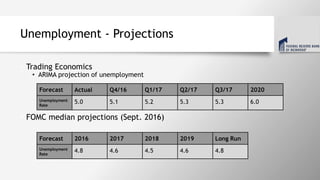

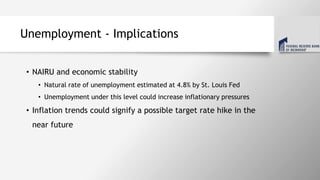

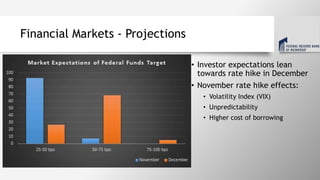

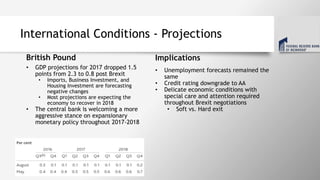

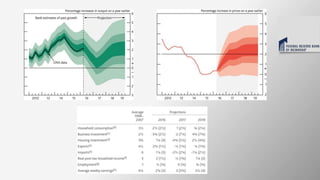

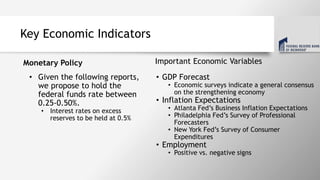

This document summarizes current economic conditions and projections from various reports. It finds that GDP growth increased in Q3 while surveys reported mixed interpretations. Several manufacturing surveys strengthened while others weakened or remained sluggish. Inflation increased slightly while unemployment decreased and expectations are that it will continue to decrease. Projections anticipate a possible December rate hike depending on revised GDP, inflation expectations, and ongoing Brexit negotiations. Key economic indicators to monitor are outlined.