Download to read offline

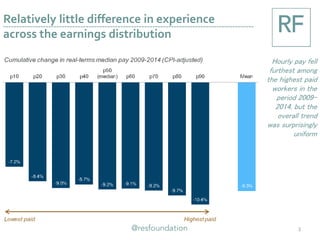

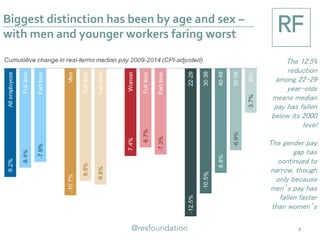

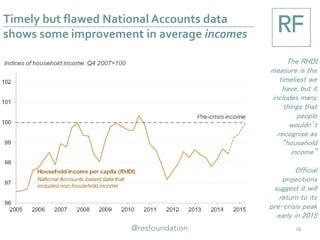

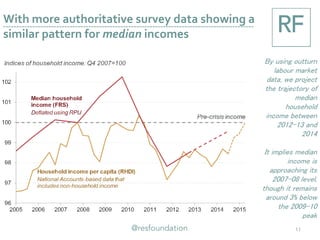

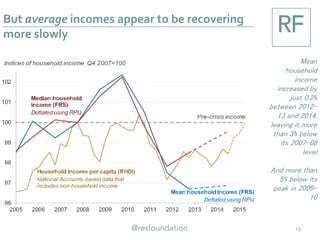

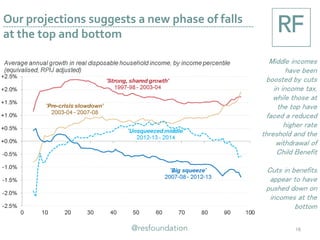

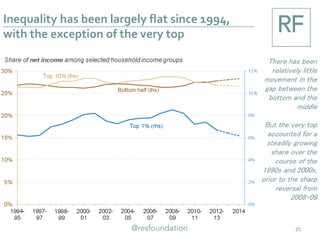

- Pay falls have been relatively uniform across earnings distributions but have hit young men hardest. With inflation falling, average pay is showing signs of improvement but full recovery to pre-crisis levels will take years. - Household incomes experienced varying impacts, with the top seeing the largest reductions initially. Recently, the middle has seen some recovery while incomes at the bottom and top have continued to fall. Median income may return to 2007 levels this year but many will still face reductions. - The analysis estimates trends in household income between 2012-13 and 2014 using outturn labor market data to project pay and population changes, finding ongoing challenges for incomes at the bottom and top.