Download to read offline

![meet and maintain requirements for EU recognition of Northern Ireland’s low incident of

BSE. It is clear from the above, therefore, that numbers begin to dominate as translations

of mission, aims and objectives into seemingly precise targets.

The style of presentation combines both narrative and descriptive prose allied with

time-bounded, specific targets[1]. For example, the Investing for Health Strategy Paper

set a number of high level targets for health improvement, showing awareness that

health is influenced by a wide range of social, economic, and environmental factors and

policies. The targets might include improving life expectancy for all while reducing the

gap between the most deprived and the Northern Ireland average; promoting mental

health and emotional well-being; reducing injuries and deaths from accidents;

promoting healthy diet and physical activity; and reducing the levels of respiratory

and heart disease exacerbated by air pollution.

The strategy to be implemented in each health area is intended to address the health

and well-being issues in the area (Northern Ireland Executive, 2001, p. 33); how issues

such as healthy life style in schools can be harnessed to improve health (Northern

Ireland Executive, 2001, p. 34); and time-bounded, specific courses of action that will

assist in achieving the objectives needed to be reached under the priority, for example

the health impact assessment introduced in April 2002. This varied presentation

approach allows for greater opportunity for demonstrating the anticipated effects of

cross-cutting policy implementation.

The above analysis shows the outcome of a process of nested translation, whereby

mission is translated into aims, objectives, and quantitative targets against which

achievements are compared. We are inclined to assume that the linkages entailed in

this nested translation are intended to convey a rational, carefully planned political

agenda for the people of NI.

Scotland

The plans for the Scottish Executive are contained in, “Working together for Scotland –

A Programme for Government” (Scottish Executive, 2001a) with the vision “making a

difference for the people of Scotland”[2]. The document is intended to account of what

the politicians have delivered against targets, showing commitment to improving the

lives of the Scottish people through delivery of social justice, creation of opportunities,

careful targeting of resources, meeting needs, and delivering better services. These

plans are intended to be achieved through the cooperation of the Executive with other

social partners in a “working together” mode.

Education and health: The education mission, “working together to give our

children the best start in life” (Scottish Executive, 2001a, section 2.4), was to be

accomplished by: ensuring that all children have access to early learning and quality

care; promoting social justice; modernizing schools; raising standards and achieving

excellence; strengthening leadership in schools and rewarding professionalism in

teaching. Under the aim of ensuring that all children have access to early learning and

quality care, one objective is: “Having delivered a nursery place for every four-year-old,

we will ensure a nursery place for every three-year-old whose parent wants it by 2002”

(Scottish Executive, 2001a, section 3.4). This objective is then linked to an allied status

report: “Achieved for four-year-olds (and) on track for three-year-olds: over 40,500 (68

percent) in pre-school education in July 2000” (Scottish Executive, 2001a, section 3.4,

and Table 1). For early support and improving schools, the following achievements

AAAJ

20,1

18](https://image.slidesharecdn.com/jurnallll-130706094510-phpapp01/85/Jurnallll-8-320.jpg)

![(DELs). Year on year percentage changes in allocations are also shown. Each

department’s budget is then concluded by explanatory narrative; for example:

[. . .] total expenditure by the Department of Health, Social Services and Public Safety will rise

by 9.7 percent to £2,527.7 million in 2002-2003. However, it is recognised that this includes a

transfer of £19 million of social security expenditure from AME [Annually Managed

Expenditure] to DEL which provides no new spending power to the department. The plans

will enable the department to maintain existing services and to make a meaningful response

to the rising costs of modern medicine. The plans, which take account of the Chancellor’s

pre-budget statement, will also enable some key service enhancements. Overall, the resources

will be allocated across a broad range of services to have maximum impact on the health and

well being of the community (Northern Ireland Executive, 2001, p. 44).

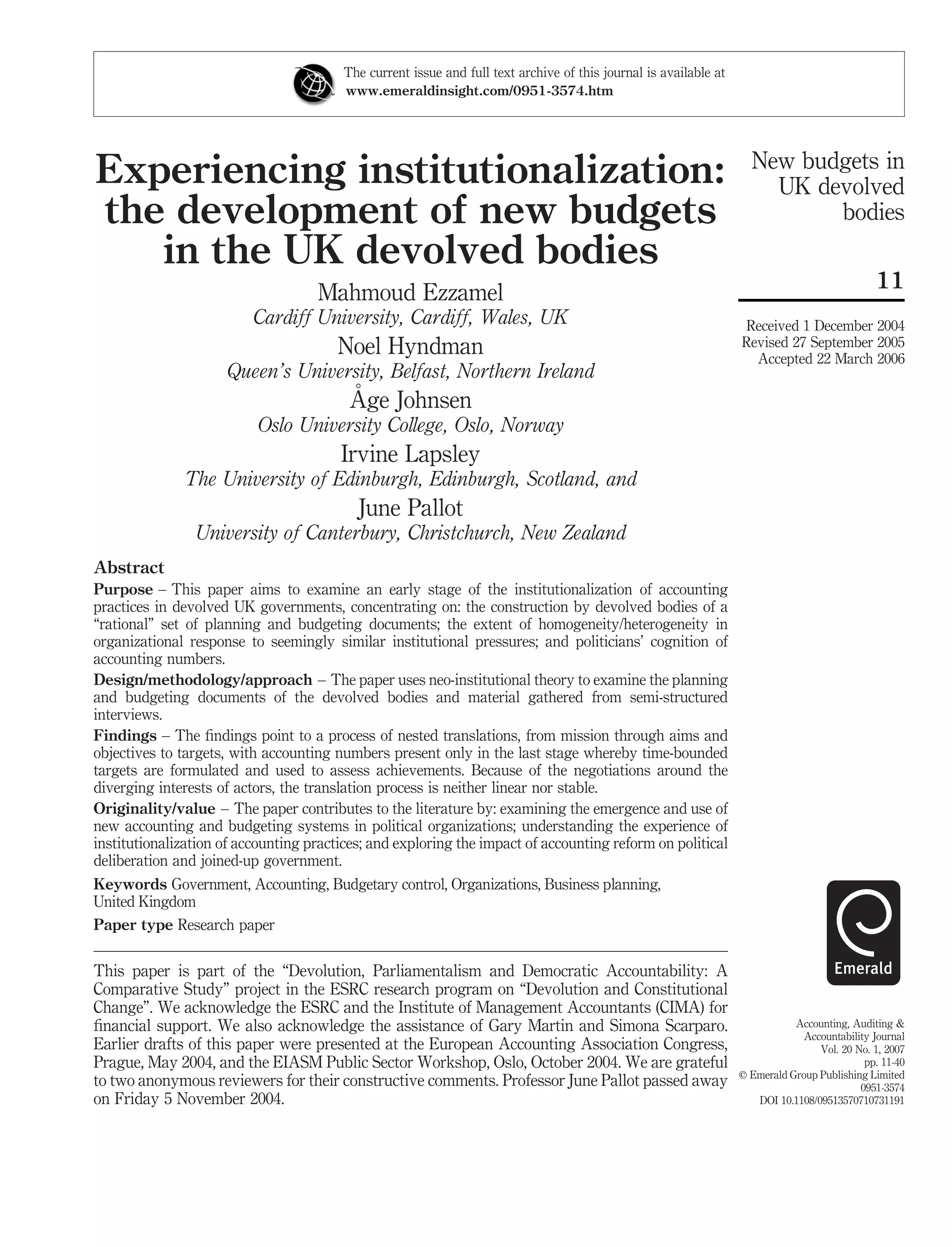

Scotland: In Scotland, the amounts spent on education and health in the previous year

are disclosed and matched in the budget with some of the activities the money helped

fund (e.g. reduction in Primary 1-2 class sizes to 30 or below in education or 955,000

operations in health). This is followed by the amounts earmarked for the coming year,

again matched with the activities they are planned to fund, e.g. providing pre-school

education places for 100 percent of three-year-olds. The introductory section presents

the planned spend in each function on education and health, along with some of the

Figure 1.

Map of aim, objectives and

spending plans relating to

education: Northern

Ireland Executive

New budgets in

UK devolved

bodies

23](https://image.slidesharecdn.com/jurnallll-130706094510-phpapp01/85/Jurnallll-13-320.jpg)

![Such an explanation is also consistent with a neo-institutional theory understanding,

whereby budget numbers are seen as manifestations of calculative rationality aimed at

gaining external legitimacy (Meyer, 1986). However, alternative explanations of the

lack of narrative in the Welsh budgets emerged, with another informant offering

time-pressure as an explanation:

One of the difficulties we would have is: we are developing the narrative now, we are

beginning to use those strategic statements within the government at the moment. The real

test for that, in any budgetary process, comes down to the wire and there is a lot of intense

negotiation about the figures over months, and then weeks, and then days, as you get to the

end. And all the minds are focused on the data, informed by the narrative earlier. Whether we

would have the time in any real budgetary process to reconnect the data to the narrative, that

would be a challenge and certainly we don’t do that at the moment (NPW).

This justification only serves to emphasize the importance of numbers in the Welsh

budgetary process; when time pressure becomes acute, what seems to get sacrificed is

the narrative as the supplement that is seemingly of marginal importance. As the

minds become “focused on the data” the narrative is pushed to the side in the quest for

concluding negotiations and producing an agreed budget “on time”. It is interesting,

however, why this supposed time pressure did not arise in the cases of Northern

Ireland and Scotland. Given the novelty of the budgetary cycle across all three

devolved institutions, it may be that those in charge of preparing budgets exhibited

fundamentally different mindsets concerning preference for numbers versus narrative;

such an explanation would be contrary to the traditional expectation of

neo-institutional theory of isomorphic conformity. In this case we would be

witnessing some heterogeneity in institutional response to similar pressures. This is an

issue that could be explored more in future research.

The somewhat utilitarian and stark presentational style of the Welsh budget is

counteracted by the publication of “Partnership Agreement” produced by the coalition

Executive made up of Labour (the party that in the first Assembly elections held the

highest number of seats but without sufficient majority to rule on its own) and the

Liberal Democrats (who joined in the political coalition to govern Wales). This

document, is the result of political compromise in that the policies in the Labour

election manifesto were revised to incorporate some of the policies to which the Liberal

Democrats were committed, and was used in the Executive’s budget planning round,

thus permitting more meaningful interpretation of the budget figures. The document:

[. . .] is a narrative. . . it is one of the key reference points in the budget turn around process

because it is commitment by Ministers, we have to ensure that resources have been allocated

to deliver the promises they made in the Partnership Agreement (NPW).

This document charts initiatives the Welsh Executive is responsible for under

departmental remits, and whether or not they have been actioned and funded. It is split

up along departmental lines and looks specifically at initiatives/targets promised, what

was promised in terms of plans anticipated, whether the initiative has been actioned

and whether or not funding was provided. An example from the education and lifelong

learning section is: “We will fully fund training grants for new primary school teachers

by increasing the total training budget to £8 million in 2001-2002 and £12 million in

2002-03” (Welsh Executive, 2001d, p. 1) – this initiative is shown as being actioned and

it is stated that provision is made for it in the baselines from 2001-2002. Hence, in order

AAAJ

20,1

26](https://image.slidesharecdn.com/jurnallll-130706094510-phpapp01/85/Jurnallll-16-320.jpg)

![politicians are already overwhelmed with information, how could they cope with more?

One non-politician from Scotland commented: “the capacity of Parliament and the

committees to use the information is really very limited. They are demanding more, but

we don’t really see them making much use of it.” The second dimension relates to the

difficulty of reconciling members’ demands for information and departments’ ability to

provide relevant information. One informant illustrated this difficulty, while also

hinting at the emphasis on process:

The difficulty is if the balance is wrong. I feel for the department on this to a degree and

protocols are being developed on this all the time. But they have responded to the demands of

committees and they’re not sure some times what they should be providing or shouldn’t be

providing and then they’re castigated for not providing documents they would have thought

they wouldn’t have had to provide. So there is a focus on process on the part of members that

riles departments and they aren’t resourced to deal with it (NPNI).

In order to cope with the amount of information available, some participants expressed

the view that a discernment relating to the relevance of the information to their roles

was crucial. Effective mechanisms that ensured filtering and focusing on important

issues were identified as being needed. Interviewees were keen to stress, however, that

the subject of information provision was one of learning and education. At the heart of

this process, the relationship between politicians and departmental officials was

identified as being important:

We’re getting information, but at times it’s not the right information, it’s not detailed enough,

or perhaps it’s too detailed. And it is a learning process at the moment, as to what information

do we need as an Assembly, within the committee structure, to do our job effectively (NPNI).

Budget cognition. Only a small number of politicians were either interested in or could

read and digest the budget; these tended to have either accounting/finance background

or extensive previous experience in the public sector. The vast majority of politicians

interviewed said that the budget was something of a mystery, and this situation was

not helped in the case of Wales because of the lack of budget narrative. Politicians who

considered themselves lacking in financial expertise tended to take a defensive posture

by attributing the ability to understand budgets to the domain of the “genius”, or those

with “a mathematical mind”, while presenting themselves as being better able to deal

with visual representations:

There are members of the Parliament who are interested in financial issues – may be

10 percent. In fairness, most members are bored rigid by financial budgeting issues (PS).

To be quite frank I think for most of us it [the budget] is probably above our heads because I

am not a statistician and I am not a mathematical genius. And I think in many respects I am a

visual person, charts, simple visual instruments. I can cope with those far better than looking

at spreadsheets (PW).

Similarly, another politician from the Welsh Assembly said: “I am pretty in-numerate,

so I find the scrutiny of columns of statistics impossible.” Such cognition problems

have consequences, which could culminate in less than effective scrutiny and

monitoring of budgets. One politician, noting this difficulty, questioned whether or not

the Executive desired to be open:

New budgets in

UK devolved

bodies

29](https://image.slidesharecdn.com/jurnallll-130706094510-phpapp01/85/Jurnallll-19-320.jpg)

![The financial grasp and the minutiae of the budget largely passes over the head of the elected

members. It’s not to say we’re all stupid, it’s just to say that the accounting procedures and

the presentational aspects of it, the fine working of it, is not easily understood by the

politicians. Now, is that deliberate or is every statement of that nature based like that? I

haven’t made up my mind on that. One thinks that some may be blinded by science, but

rather than admit to ignorance, they say wonderful, we’ll vote for that (PNI).

Such repeated emphasis by politicians upon their perceived lack of interest in, or

ability to comprehend, financial information is striking. Inability to understand

financial information may in itself encourage politicians to treat financial information

as less relevant to their deliberations. Those who desired to mobilize financial

information in their debate, and at the same time lacked the ability to understand such

information, tended to seek help either from their researchers or more likely from other

knowledgeable members of their party:

I don’t really mind who I go to, I will weigh up in my own mind how much credibility I would

give to other people’s comments. But I am sure that other members also go out and try to find

other views (PW).

Much of the performance information in each devolved body is contained in the budget

and the budget reports. While there appeared to be some disagreement among

participants regarding their perception of the levels of performance information that

are produced, the vast majority were of the opinion that there was limited systematic

dissemination of what was available. In addition, the flow and amount of performance

information were considered far from satisfactory:

[. . .] we only receive information on performance in briefings, when we actually search it

out. . . Now, hitherto, I would have to say that it’s been a bit short. Quite what the reluctance

is; is it that it’s not available because the programme is relatively new or is it because they

think that the programme is addressing the problem but they’re not quite sure, and they don’t

want to expose the fact that they’re pouring large sums of money into it without it having

proved itself? (PNI).

When it comes to finance and political debates, there is never enough information in detail on

how public money is allocated . . . It is very difficult, really, to get to the guts of many

questions even with approval from the Treasury (PS).

[. . .] a lot of it [accounting information] is probably designed to keep us in the dark. There are

all sorts of bold part figures, that is the right expression, circulating about, but you don’t

really know what has been spent on what (PS).

With respect to performance information, there has been a focus on looking at inputs

and activity levels, rather than this loop being completed by reviewing the associated

issues concerned with outcomes and customer services, but that this was changing

because public bodies are:

Fabulous at firing arrows at walls, drawing targets around them and then saying it was a

brilliant shot. The situation has now moved on to, there’s the target, now fire the arrow at it

(NPNI).

Given politicians’ limited cognition of numbers, scrutiny (and accountability) is likely

to be diluted as it appears that little use is made of accounting information in political

deliberations. Politicians were perceived by non-politicians as being more concerned

AAAJ

20,1

30](https://image.slidesharecdn.com/jurnallll-130706094510-phpapp01/85/Jurnallll-20-320.jpg)

![Translating and operationalizing objectives further involved the formulation of

time-bounded and specific targets where specific numbers begin to mediate as the

expression of political commitments in what is emerging as a “management by

numbers” culture (Ezzamel et al., 1990). Given the prevalence of such a management by

numbers culture within the institutional field, the emphasis on numbers could be taken

as a means of the devolved bodies demonstrating their compliance with that culture

(isomorphic pressure). This focus on numbers was evident in each body; in some

instances, reference was made to past achievements and how these fitted in with the

overall plan (in Scotland and Northern Ireland, though more so in Scotland), whilst

others focused solely on future intentions and plans (Wales). This situation in Wales

may be due to the Scottish and Northern Ireland documents being relatively more

comprehensive, as Wales developed separate planning documents for separate policy

issues. Targets, particularly those stated in numerical terms, seemingly became more

precise translations of the broad, less differentiating, mission, aims and objectives as

more precisely delineated measures of accountability to which the Executive could be

held. In this sense, the targets stated in the budget documents of each devolved body

provided a visible link back to objectives, aims and ultimately mission. It is these

precise targets that are likely to act as the yardstick against which actual achievements

and political aspirations could be contrasted and compared. This chain of seemingly

logical, precise translation, which we gleaned from our analysis of the planning and

budgeting documents, from missions ultimately into numbers, both creates and

reinforces a myth of rational governance, where trust is placed into governance by

quantification. The budget in each devolved institution therefore can be seen to

function as a “ritual” of reason, seeking to legitimize the manner by which the devolved

bodies conduct themselves (Czarniawska-Jorges and Jacobsson, 1989).

Homogeneities and heterogeneities

The three devolved bodies shared some commonalities in their planning and budgeting

documents. First, a top-to-bottom management architecture (Meekings, 1995) was

evident in all bodies with one caveat; in Scotland, the formulation of the mission

statements was a more elongated process, and the Scottish programme for government

had much broader aims than in the other two institutions[3]. In Scotland, there

appeared to be a greater preponderance placed on defining, in Drucker’s (1980, p. 104)

terminology, “a lofty organizational objective”. Second, a systematic review

architecture (Meekings, 1995) was common across the devolved bodies, with the

periodic reporting of achievements being commonplace. Third, an integrated planning

and budgeting process (Meekings, 1995) was in place, though to a lesser extent in

Wales compared to Scotland and Northern Ireland. In considering the link and

coupling between planning documents and the budgetary documents, tight

arrangements were evidenced in both Scotland and Northern Ireland. In Wales, this

process was much less explicit and the reader needs to expend much more effort if the

interrelationships between all areas of planning and funding are to be made. This may

be a consequence of the existence of substantial alternative planning documents as

alluded to above. Thus, while we are witnessing strong tendencies towards isomorphic

compliance, there are still some elements of heterogeneity between the three devolved

bodies (Townley, 2002).

AAAJ

20,1

34](https://image.slidesharecdn.com/jurnallll-130706094510-phpapp01/85/Jurnallll-24-320.jpg)

This document summarizes a research paper that examines the development of new budgeting and planning processes in the UK's devolved governments of Northern Ireland, Scotland, and Wales following devolution in the late 1990s. The researchers analyze planning and budget documents from the three bodies using neo-institutional theory to understand how new accounting practices emerge and become institutionalized. Their findings show a process of translating broad visions and missions into specific, time-bound targets in budgets, though this process is non-linear and negotiated. They also find both similarities and differences in the budgeting processes across the three bodies, indicating elements of isomorphism as well as heterogeneity. Politicians in all three bodies struggled to understand budget contents without assistance from financial experts.

![20090502 porj-s-07-00024[1]](https://cdn.slidesharecdn.com/ss_thumbnails/20090502-porj-s-07-000241-110416112012-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)