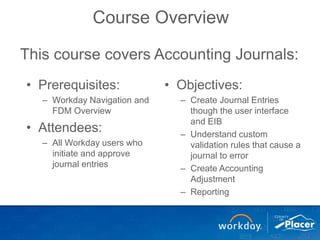

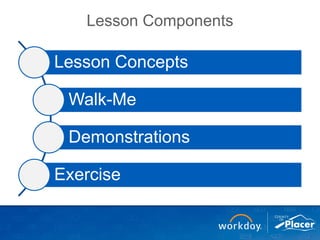

This document outlines an end user training course on journal entries in Workday. The course covers creating and finding journals, journal concepts like custom validations and balancing funds, demonstrations on creating basic journals and uploading journals via EIB files, and processing accounting adjustments. Exercises are included for trainees to practice these skills with instructor assistance.