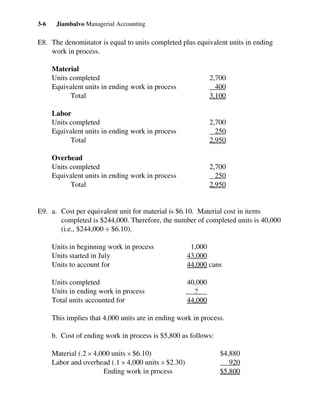

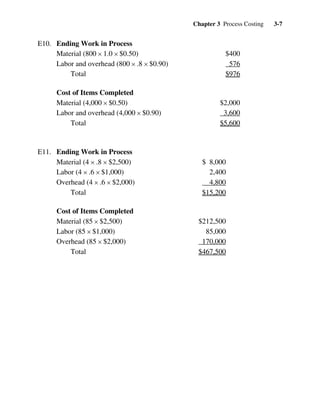

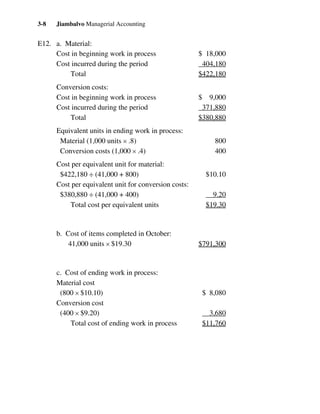

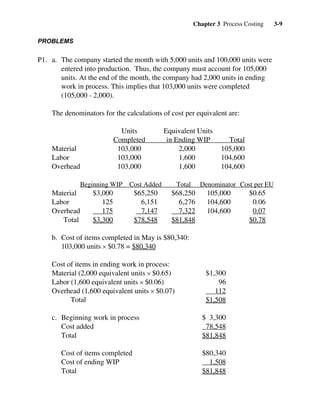

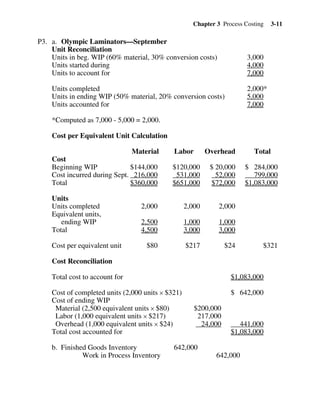

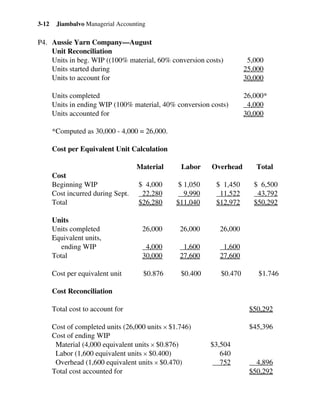

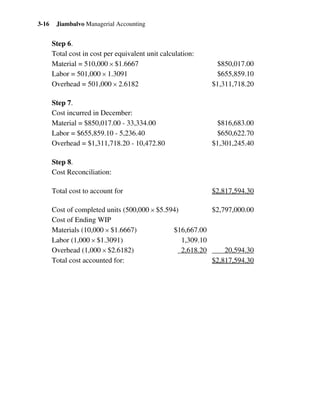

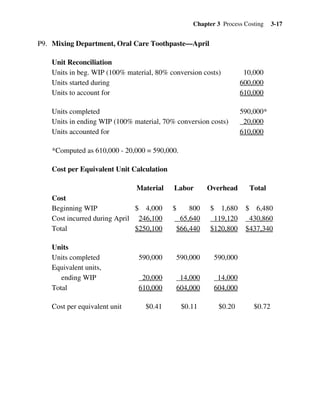

Downloaded 219 times

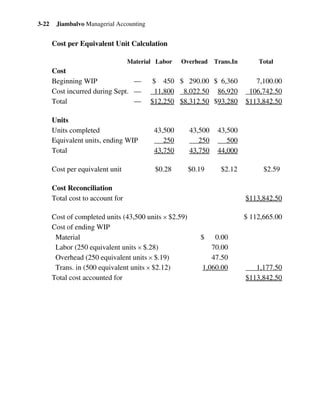

This document discusses process costing concepts including: 1. Equivalent units is used to calculate average unit costs and represents partially completed units as a percentage of whole units. 2. Conversion costs include direct labor and overhead costs incurred throughout the production process. 3. Cost per equivalent unit is calculated by dividing the total costs (beginning WIP + costs incurred) by the total units (completed + equivalent units in ending WIP). 4. Reconciliation ensures calculations are correct and no units are lost by accounting for the total number of units.