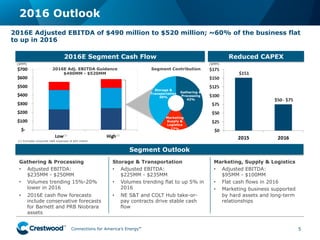

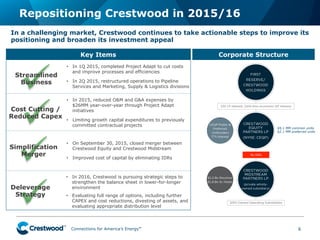

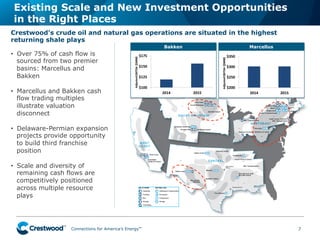

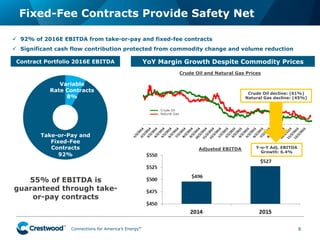

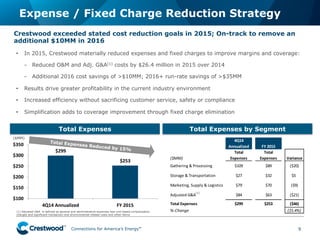

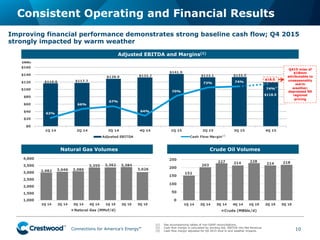

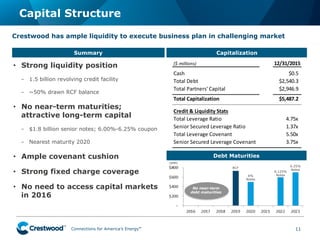

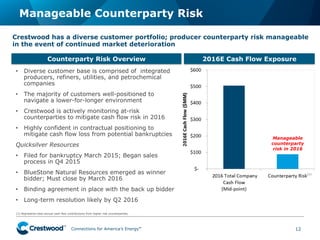

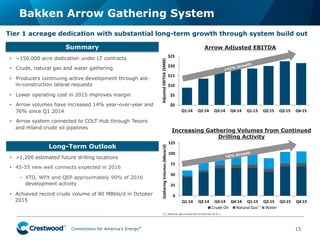

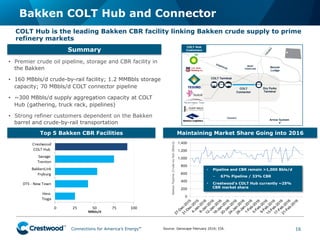

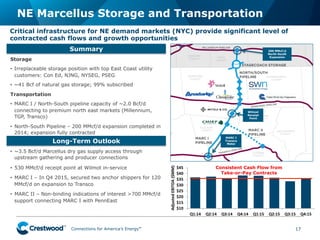

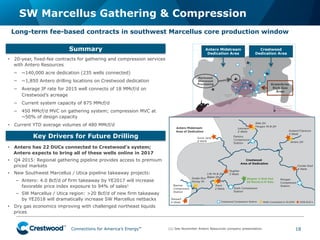

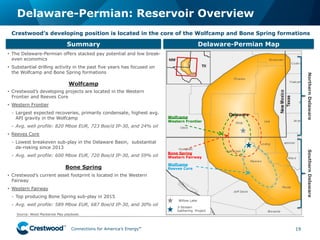

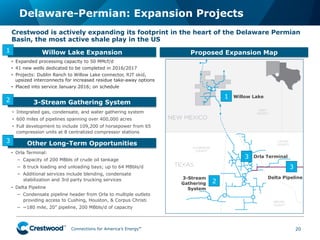

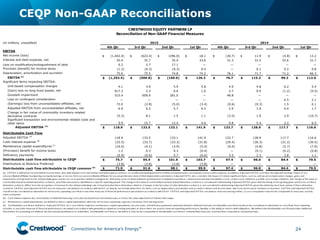

The document provides an overview of Crestwood Midstream Partners LP and Crestwood Equity Partners LP. It discusses key investor highlights including 2016 outlook and adjusted EBITDA guidance of $490-520 million. It also summarizes the company's capital structure, debt maturity profile, and operational updates in core areas like the Bakken shale play.