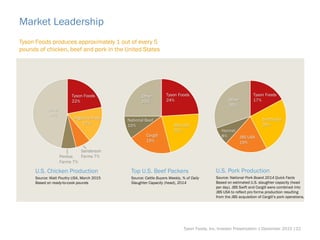

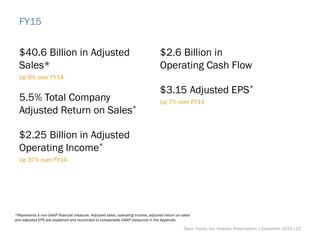

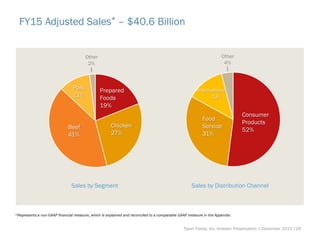

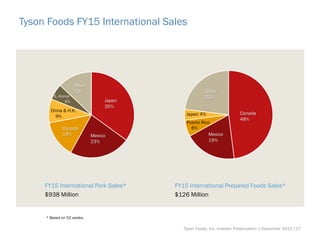

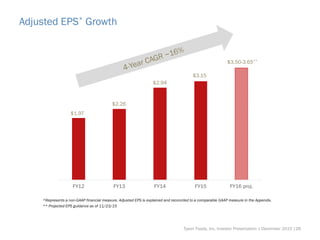

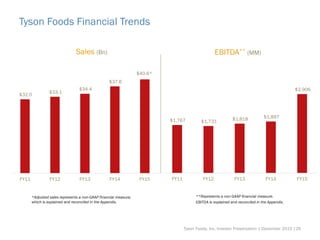

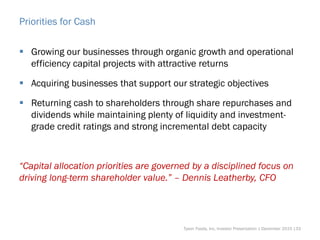

The document provides forward-looking statements and cautions readers that actual results may differ materially from expectations. It highlights that Tyson Foods is one of the largest food companies in the world with advantaged brands in growing categories. The presentation outlines Tyson's market leadership in protein production, financial trends including sales growth and adjusted EPS growth, and priorities for cash including growing organically, acquisitions, and returning cash to shareholders.